Answered step by step

Verified Expert Solution

Question

1 Approved Answer

1. Record 2021 income taxes. 2. Record 2022 income taxes. 3. Record 2023 income taxes. 4. Record 2024 income taxes. Zekany Corporation would have had

1. Record 2021 income taxes.

2. Record 2022 income taxes.

3. Record 2023 income taxes.

4. Record 2024 income taxes.

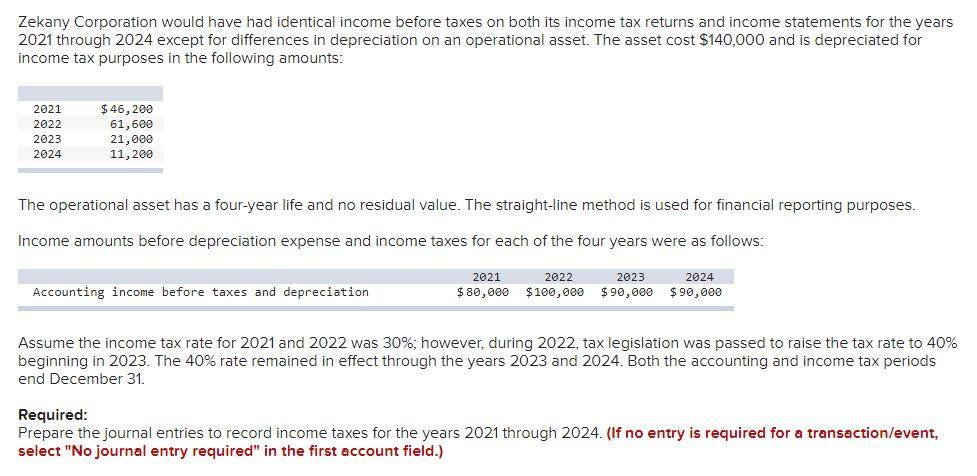

Zekany Corporation would have had identical income before taxes on both its income tax returns and income statements for the years 2021 through 2024 except for differences in depreciation on an operational asset. The asset cost $140,000 and is depreciated for income tax purposes in the following amounts: 2021 2022 2023 $ 46,200 61,600 21,000 11,200 2024 The operational asset has a four-year life and no residual value. The straight-line method is used for financial reporting purposes. Income amounts before depreciation expense and income taxes for each of the four years were as follows: Accounting income before taxes and depreciation 2021 $80,000 2022 $100,000 2023 $ 90,000 2024 $ 90,000 Assume the income tax rate for 2021 and 2022 was 30%; however, during 2022, tax legislation was passed to raise the tax rate to 40% beginning in 2023. The 40% rate remained in effect through the years 2023 and 2024. Both the accounting and income tax periods end December 31. Required: Prepare the journal entries to record income taxes for the years 2021 through 2024. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting And Financial Analysis In The Hospitality Industry

Authors: Jonathan A. Hales

1st Edition

0750678968, 978-0750678964