Answered step by step

Verified Expert Solution

Question

1 Approved Answer

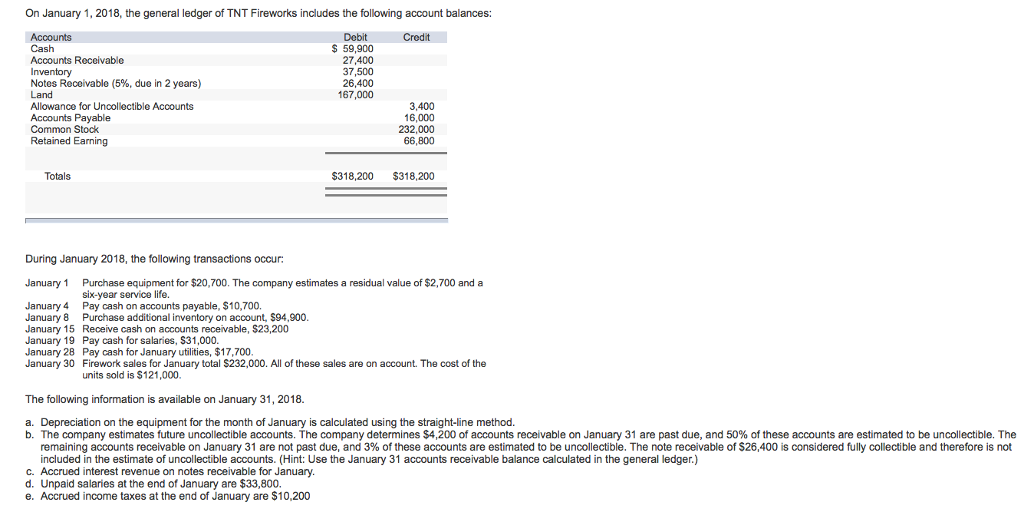

1. Record each of the transactions listed above in the 'General Journal' tab (these are shown as items 1 - 8) assuming a FIFO perpetual

|

1.

| Record each of the transactions listed above in the 'General Journal' tab (these are shown as items 1 - 8) assuming a FIFO perpetual inventory system. The transaction on January 30 requires two entries: one to record sales revenue and one to record cost of goods sold. Review the 'General Ledger' and the 'Trial Balance' tabs to see the effect of the transactions on the account balances. | |

| 2. | Record adjusting entries on January 31. in the 'General Journal' tab (these are shown as items 9-13). | |

| 3. | Review the adjusted 'Trial Balance' as of January 31, 2018, in the 'Trial Balance' tab. | |

| 4. | Prepare a multiple-step income statement for the period ended January 31, 2018, in the 'Income Statement' tab. | |

| 5. | Prepare a classified balance sheet as of January 31, 2018, in the 'Balance Sheet' tab. | |

| 6. | Record the closing entries in the 'General Journal' tab (these are shown as items 14 and 15). | |

| 7. | Using the information from the requirements above, complete the 'Analysis' tab. |

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Small Business Financial Management Kit For Dummies

Authors: Tage C. Tracy, John A. Tracy

1st Edition

047012508X, 978-0470125083