Answered step by step

Verified Expert Solution

Question

1 Approved Answer

1. Suppose there are two basis assets on the market - a stock and a risk-free zero-coupon bond with face value $100 and time-to-maturity of

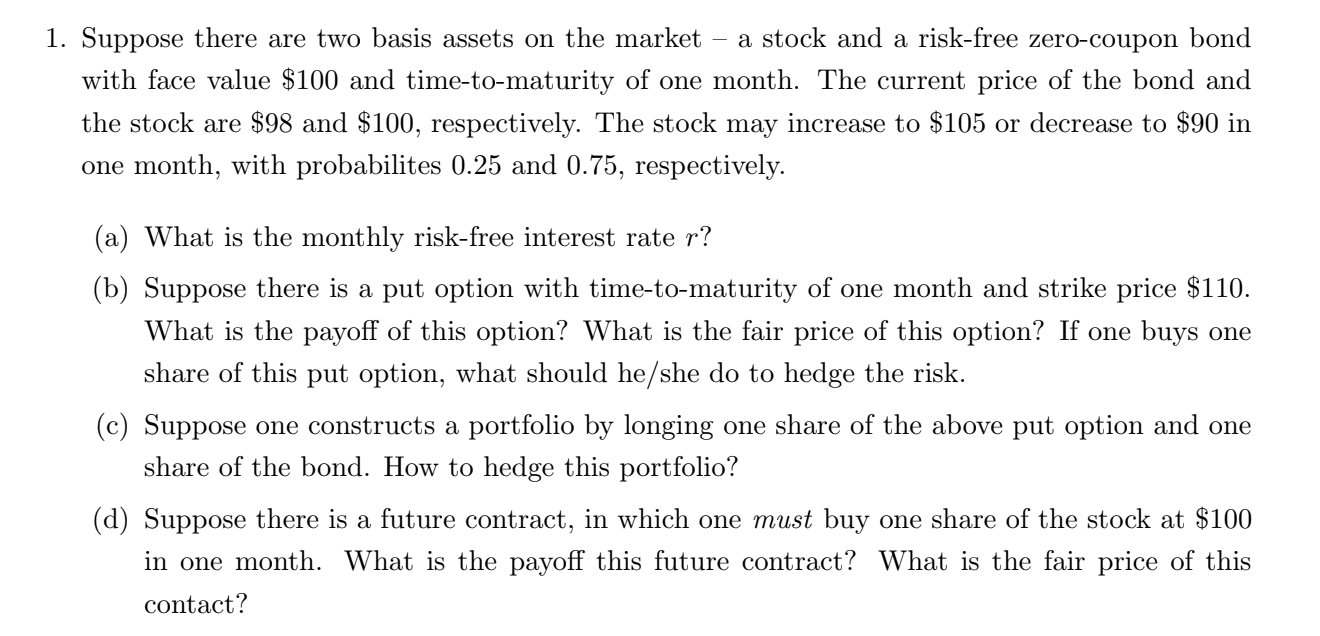

1. Suppose there are two basis assets on the market - a stock and a risk-free zero-coupon bond with face value $100 and time-to-maturity of one month. The current price of the bond and the stock are $98 and $100, respectively. The stock may increase to $105 or decrease to $90 in one month, with probabilites 0.25 and 0.75 , respectively. (a) What is the monthly risk-free interest rate r ? (b) Suppose there is a put option with time-to-maturity of one month and strike price $110. What is the payoff of this option? What is the fair price of this option? If one buys one share of this put option, what should he/she do to hedge the risk. (c) Suppose one constructs a portfolio by longing one share of the above put option and one share of the bond. How to hedge this portfolio? (d) Suppose there is a future contract, in which one must buy one share of the stock at $100 in one month. What is the payoff this future contract? What is the fair price of this contact

1. Suppose there are two basis assets on the market - a stock and a risk-free zero-coupon bond with face value $100 and time-to-maturity of one month. The current price of the bond and the stock are $98 and $100, respectively. The stock may increase to $105 or decrease to $90 in one month, with probabilites 0.25 and 0.75 , respectively. (a) What is the monthly risk-free interest rate r ? (b) Suppose there is a put option with time-to-maturity of one month and strike price $110. What is the payoff of this option? What is the fair price of this option? If one buys one share of this put option, what should he/she do to hedge the risk. (c) Suppose one constructs a portfolio by longing one share of the above put option and one share of the bond. How to hedge this portfolio? (d) Suppose there is a future contract, in which one must buy one share of the stock at $100 in one month. What is the payoff this future contract? What is the fair price of this contact Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Sustainable Development

Authors: Magdalena Ziolo

1st Edition

0367819767, 978-0367819767