Answered step by step

Verified Expert Solution

Question

1 Approved Answer

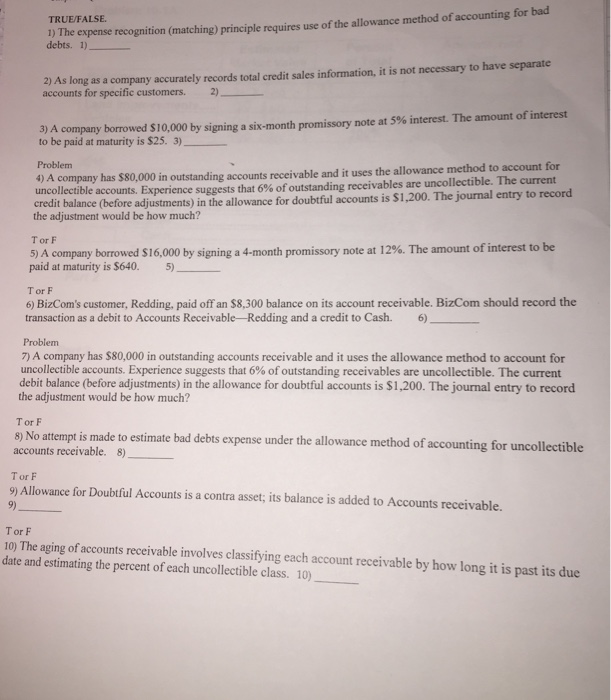

1) The expense recognition (matching) principle requires use of the allowance method of accounting for bad debts. 1) TRUE/FALSE. 2) As long as a company

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Cost Accounting

Authors: Edward J. Vanderbeck

12th Edition

0324100949, 978-0324100945