Answered step by step

Verified Expert Solution

Question

1 Approved Answer

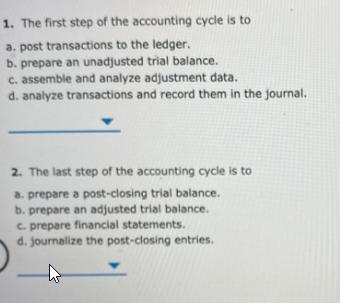

1. The first step of the accounting cycle is to a. post transactions to the ledger. b. prepare an unadjusted trial balance. c. assemble

1. The first step of the accounting cycle is to a. post transactions to the ledger. b. prepare an unadjusted trial balance. c. assemble and analyze adjustment data. d. analyze transactions and record them in the journal. 2. The last step of the accounting cycle is to a. prepare a post-closing trial balance. b. prepare an adjusted trial balance. c. prepare financial statements. d. journalize the post-closing entries.

Step by Step Solution

★★★★★

3.44 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

ANSWER 1 D Analyze transactions and record them in the journal Identifying an economic event or transaction is the first phase of the accounting cycle ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting Introduction To Financial Accounting

Authors: Henry Dauderis, David Annand

1st Edition

1517089719, 978-1517089719