Answered step by step

Verified Expert Solution

Question

1 Approved Answer

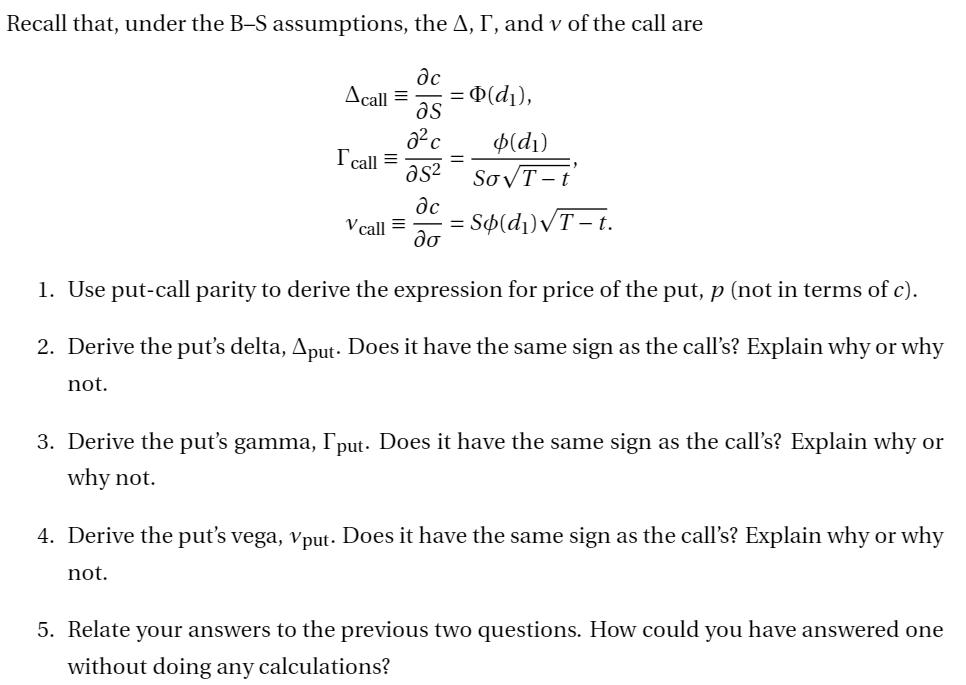

Recall that, under the B-S assumptions, the A, I, and v of the call are Acall = = (d), as $(d1) I call =

Recall that, under the B-S assumptions, the A, I, and v of the call are Acall = = (d), as $(d1) I call = as SoT-t' V call = = So(d)T-t. do 1. Use put-call parity to derive the expression for price of the put, p (not in terms of c). 2. Derive the put's delta, Aput. Does it have the same sign as the call's? Explain why or why not. 3. Derive the put's gamma, put. Does it have the same sign as the call's? Explain why or why not. 4. Derive the put's vega, Vput. Does it have the same sign as the call's? Explain why or why not. 5. Relate your answers to the previous two questions. How could you have answered one without doing any calculations?

Step by Step Solution

★★★★★

3.48 Rating (168 Votes )

There are 3 Steps involved in it

Step: 1

1 Using putcall parity we have P S C X1 rT Rearranging the equation we can solve for the price of th...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Elementary Statistics

Authors: Neil A. Weiss

8th Edition

321691237, 978-0321691231