Question: 1) Using COSO (2013), identify principles of effective control and associated risks that could threaten preschool objectives. Create a chart using the following headings. For

1) Using COSO (2013), identify principles of effective control and associated risks that could threaten preschool objectives. Create a chart using the following headings. For the principles identified (in the Principles column and explained on page 203 in the Romney text), identify the situation in existence at the ARK (under Application to the ARK Preschool) that represents adherence to the COSO principle (listed under Principles). Then list the Risks that this situation raises (list under Risks) :

| Principles | Application to the Ark Preschool | Risks |

| 3. Is there clear oversight? Clear reporting lines of authority? |

|

|

| 10. Have control activities been selected to minimize risks |

|

|

| 11. Have control activities over technology been developed? |

|

|

| 13. Does the preschool use information to assess internal control? |

|

|

2) The Ark is a small business with budget constraints. What control improvements would you recommend to reduce the risk of misstatement or fraud? Page212 in the Romney text begins a discussion of the control sources that you can think about in relation to the ARK. These controls need not line up to the previous question. Use the following table structure for your answer:

|

Control Source |

Suggested Control Procedures |

| Authorization controls |

|

| Segregation of functions |

|

| Accounting Records |

|

| Access Controls |

|

| Independent Verification |

|

|

|

|

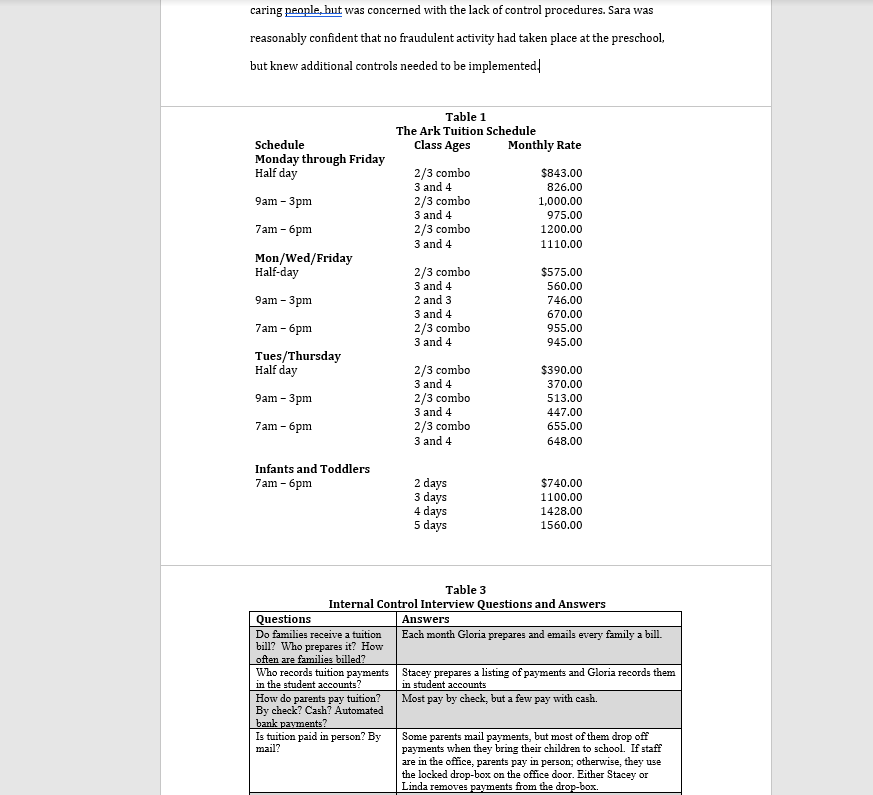

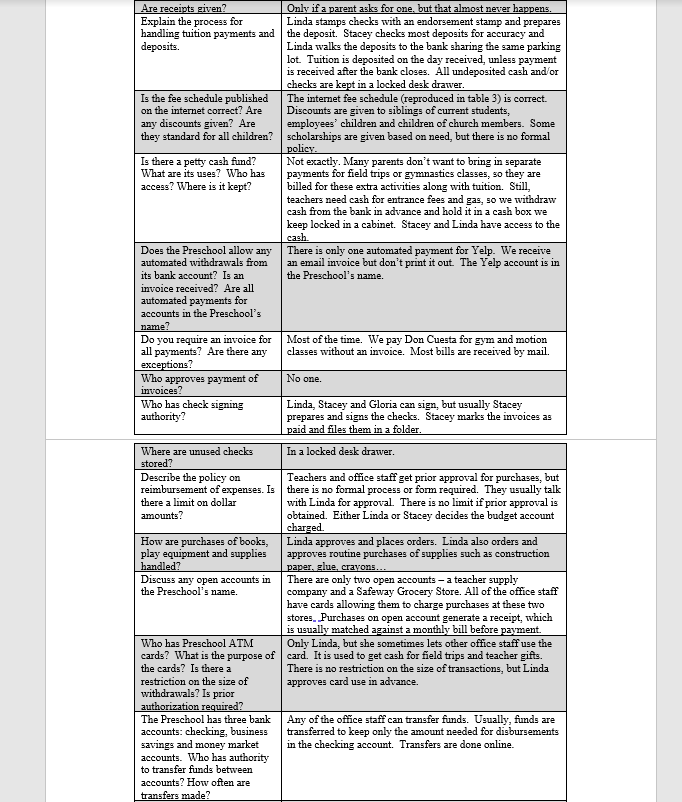

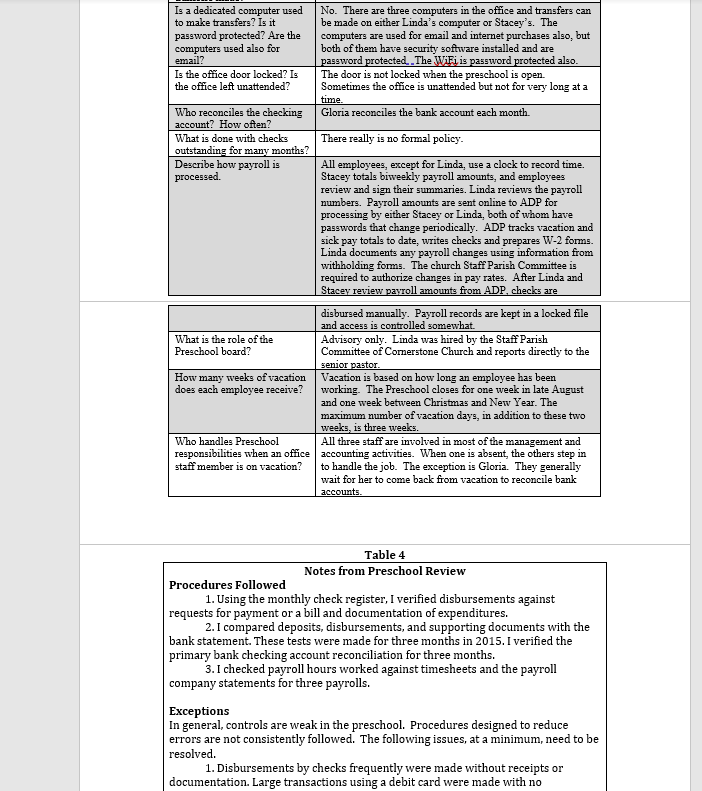

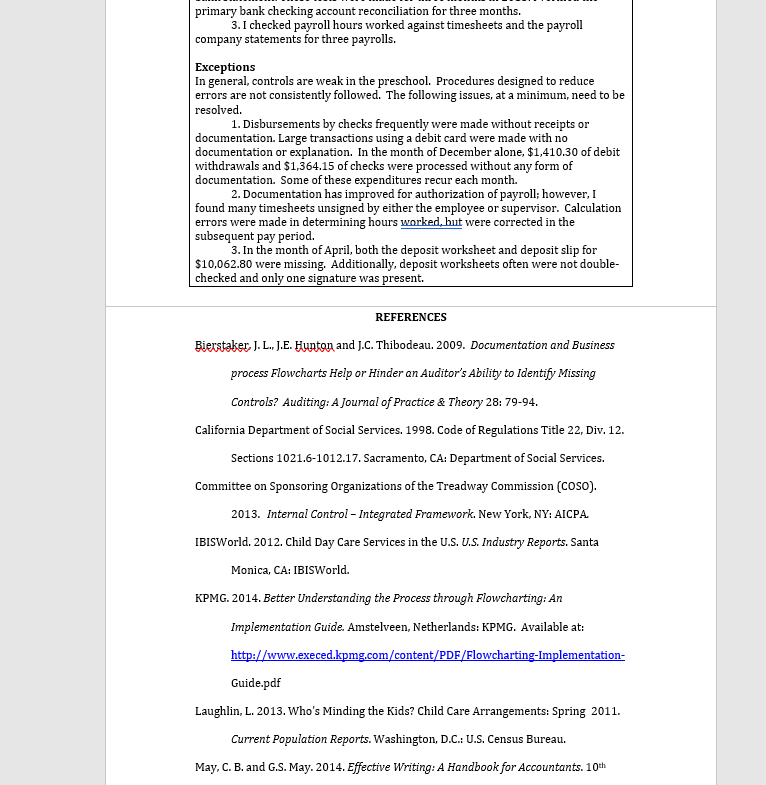

CASE: WHO'S IN CONTROL OF THE ARK? Sara Green released her seat belt and reached into the back seat of her car for the list of audit and control questions she had prepared for the director of the Ark Preschool. She paused, listening to the sounds of children's laughter, before closing the car door and walking into the building. Sara's two children had attended the Ark Preschool and she stood for a moment in the hallway as memories washed over her. Sara remembered Thanksgiving dinners with her children dressed in grocery bag costumes of Native Americans and Pilgrims, Mother's Day teas with cookies made by children and teachers, and the annual fall festivals. Startled from her reverie by slamming doors, Sara made her way to the preschool office. Sara entered a tiny office crammed with three desks, computers, boxes, and supplies, and was surprised to see three middle-aged women waiting anxiously for her. After clearing papers from the only empty seat, Sara greeted the preschool director, the education administrator, and the office assistant. The director and administrator run the preschool on a daily basis handling tuition receipts, bill payments, crying children, worried parents and tired teachers. The part-time office assistant, a former engineer, primarily records transactions into a Quicken system and reconciles bank statements. Sara had asked to meet with the administrator to ask a few questions about organizational goals and accounting processes at the preschool, but all three wanted to take part in the conversation. Sara settled into her chair and pulled out her list of questions. After briefly explaining the importance of internal control, she asked the staff about preschool operating, reporting and compliance objectives. They responded that operating objectives of the Ark Preschool include financial solvency, sufficient cash when needed, reduction of waste, effective scheduling of teachers to minimize overtime, and protection of preschool equipment from theft. Their financial reporting objectives include monthly budget updates, timely reconciliation of bank accounts, and reliable annual reports to Cornerstone Church. The most important compliance objective is adherence to wage and labor laws, federal and state income reporting regulations, and state preschool licensing requirements. Sara listened carefully as the administrator answered questions with the director and assistant adding their comments. Ringing telephones and teachers clocking out at the end of the day interrupted the interview, but Sara quickly realized all three administrators were clearly invested in the preschool and we were eager to explain how it worked. She leaned forward and started taking notes. 1 Child Care in the United States By the early 2010's, childcare had grown to be a $47 billion industry in the United States alone (IBISWorld 2012). In 2012, 65% of women with children aged three to five worked outside of the home, requiring assistance with child care (U.S. Census Bureau 2012). A patchwork of parents, family members, nonrelatives in the home, and external providers take care of children under school-age. Most home- based providers care for the children of no more than two families and are located in private homes, Day care centers generally care for 50 to 100 children, and are either for-profit corporations or not-for-profits sponsored by churches, community centers, parent cooperatives or Head Start (Laughlin 2013). State and local regulations ensure facilities are safe, supervision is adequate and children are protected. Safety inspections are common, but the greatest regulatory issue for most childcare facilities is the maintenance of adequate ratios of children to staff members. While regulations vary across the United States, all states place limits on the number of children under the supervision of each caregiver. For example, California's Title 22 (1998) requires that a single caregiver attend to no more than four infants, six toddlers from 18 to 30 months, or twelve children between age two and kindergarten. Staffing is a major issue for most preschools and it is difficult to attract caregivers who are both qualified and willing to work long hours for modest pay. Over 441,000 individuals were employed as preschool teachers in 2014, the average annual pay was $32,040, and most jobs required an associate's degree (Bureau of Labor Statistics 2014). Jobs are expected to grow by 6.7% over the period from 2014 through 2024. | The Ark Preschool The Ark Preschool is a not-for-profit preschool operating as an outreach ministry of the Cornerstone Church. It opened in 1985 when the first director saw a need for quality childcare in the community. Over time, the school adapted to meet the needs of both families who were members of the church and families in the community, and expanded operations to provide full-day childcare from infancy to school age. As an outreach ministry of the church, the preschool's purpose is to provide quality care and early education in a loving environment, and the preschool prides itself on its family feel. In its first ten years, the preschool was indeed a close- knit family with the director employing four of her daughters as teachers. The preschool has employed several directors since 1985, but the mission has remained the same: to celebrate the spirit and encourage the development of each child. A day at the preschool includes story time, alphabet and counting games, outdoor play, nature walks, water play, crafts for small motor skills, music and singing. At any time, between 60 and 75 children are enrolled at the preschool either as full-time or part-time students. Annual tuition has grown to $709,596 in 2015, an average of $59,000 per month. Expenses in 2015 total $708,459, with the preschool operating essentially in a break-even mode. The largest expenditures are for payroll and employee benefits, but the preschool also pays $3,200 per month for space shared with the church. Current tuition rates are reported in Table 1. As is true of many not-for-profit organizations and small businesses, the Ark Preschool maintains a small administrative staff. In addition to the director and education administrator, the preschool employs 15 part-time and full-time teachers, a resource specialist, and a part-time office assistant. Both the director and administrator have early childhood education credentials and serve as substitute teachers when needed. Linda Gonzalez, the preschool director, is responsible for the overall management of the school, including teacher hiring and training, program planning, community relations and coordination with the sponsoring church. Linda meets quarterly with the preschool advisory board, comprised of five parents of preschool children, one of which is also a church member. Linda is directly responsible to the senior minister of the Cornerstone Church and its Staff-Parish Committee. The education administrator, Stacey Okada, assists the director in daily activities and is responsible for general financial oversight, reviewing and approving financial expenditures, deposits, and the transfer of funds between checking and savings accounts. The preschool recently hired Gloria Lloyd, the mother of several former students, to handle record-keeping activities and bookkeeping on a part- time basis. Sara Green Sara began her career as a CPA in a small regional accounting firm. After several years, she returned to graduate school for an advanced degree and currently teaches accounting at a local university. Although she no longer practices as a CPA, Sara keeps her license active by completing 40 continuing education units each year. Her children attended the Ark Preschool when they were younger, and her family are members of Cornerstone Church. Sara also served on the church finance committee for five years but resigned when her evening teaching responsibilities interfered with committee meetings. Ken Robinson, a retiree with little finance experience who served as church treasurer, asked Sara to perform the annual review of the church and preschool financial records. Knowing the demands of performing an audit and the demands miscalculations of hours worked, most of them a half-hour or less, Sara was happy to see that payroll summaries generally were accurate. This was an improvement over prior years. Sara turned to reconciliations of bank statements, which Gloria completed on a monthly basis. Using bank statements and the preschool check register, Sara reconciled the December 31, 2015 cash account and found it agreed with Gloria's reconciliation. Beginning with the January statement and the computer ledgers, she matched bank disbursements with amounts recorded on the preschool records and supporting documentation. She knew the preschool had entered into automatic payments for recurring disbursements for advertising with Yelp, an online publisher of crowd-sourced business reviews, but frowned when she saw several ATM payments lacking any documentation, Sara listed general principles for achieving internal control over cash for a small organization: No employee should handle a transaction from beginning to end. Separate cash handling from record keeping. Centralize cash handling as much as possible. Record cash receipts on a timely basis. Make deposits daily. Encourage parents to receive receipts. Make all expenditures by check or electronic funds transfer. An employee not handling cash should prepare monthly bank reconciliations. An appropriate administrator should review the reconciliations monthly. Compare cash receipts and disbursements to forecasted amounts and budgets. Sara summarized her concerns on a legal pad, presented in Table 4. Sara sat back in her chair and thought about the children, teachers and parents at the preschool as well as the congregation at Cornerstone Church. She had read news reports of other schools using state funds for employee vacations, mortgage payments and shopping sprees. She believed the director and office staff were caring people, but was concerned with the lack of control procedures. Sara was reasonably confident that no fraudulent activity had taken place at the preschool, but knew additional controls needed to be implemented Schedule Monday through Friday Half day 9am - 3pm 7am - 6pm Table 1 The Ark Tuition Schedule Class Ages Monthly Rate 2/3 combo $843.00 3 and 4 826.00 2/3 combo 1,000.00 3 and 4 975.00 2/3 combo 1200.00 3 and 4 1110.00 2/3 combo $575.00 3 and 4 560.00 2 and 3 746.00 3 and 4 670.00 2/3 combo 955.00 3 and 4 945.00 Mon/Wed/Friday Half-day 9am-3pm 7am - 6pm Tues/Thursday Half day 9am - 3pm 7am-6pm 2/3 combo 3 and 4 2/3 combo 3 and 4 2/3 combo 3 and 4 $390.00 370.00 513.00 447.00 655.00 648.00 Infants and Toddlers 7am -6pm 2 days 3 days 4 days 5 days $740.00 1100.00 1428.00 1560.00 Table 3 Internal Control Interview Questions and Answers Questions Answers Do families receive a tuition Each month Gloria prepares and emails every family a bill. bill? Who prepares it? How often are families billed? Who records tuition payments Stacey prepares a listing of payments and Gloria records them in the student accounts? in student accounts How do parents pay tuition? Most pay by check, but a few pay with cash. a By check? Cash? Automated bank payments? Is tuition paid in person? By Some parents mail payments, but most of them drop off mail? payments when they bring their children to school. If staff are in the office, parents pay in person, otherwise, they use the locked drop-box on the office door. Either Stacey or Linda removes payments from the drop-box. Are receipts given? Only if a parent asks for one, but that almost never happens. Explain the process for Linda stampa checks with an endorsement stamp and prepares handling tuition payments and the deposit. Stacey checks most deposits for accuracy and deposits. Linda walks the deposits to the bank sharing the same parking lot. Tuition is deposited on the day received, unless payment is received after the bank closes. All undeposited cash and/or checks are kept in a locked desk drawer. Is the fee schedule published The internet fee schedule (reproduced in table 3) is correct. on the internet correct? Are Discounts are given to siblings of current students, any discounts given? Are employees' children and children of church members. Some they standard for all children? scholarships are given based on need, but there is no formal policy. Is there a petty cash fund? Not exactly. Many parents don't want to bring in separate What are its uses? Who has payments for field trips or gymnastics classes, so they are access? Where is it kept? billed for these extra activities along with tuition. Still, teachers need cash for entrance fees and gas, so we withdraw cash from the bank in advance and hold it in a cash box we keep locked in a cabinet. Stacey and Linda have access to the cash Does the Preschool allow any There is only one automated payment for Yelp. We receive automated withdrawals from an email invoice but don't print it out. The Yelp account is in its bank account? Is an the Preschool's name. invoice received? Are all automated payments for accounts in the Preschool's name? Do you require an invoice for Most of the time. We pay Don Cuesta for gym and motion all payments? Are there any classes without an invoice. Most bills are received by mail. exceptions? Who approves payment of No one. invoices? Who has check signing Linda, Stacey and Gloria can sign, but usually Stacey authority? prepares and signs the checks. Stacey marks the invoices as paid and files them in a folder. Where are unused checks In a locked desk drawer. stored? Describe the policy on Teachers and office staff get prior approval for purchases, but reimbursement of expenses. Is there is no formal process or form required. They usually talk there a limit on dollar with Linda for approval. There is no limit if prior approval is amounts? obtained. Either Linda or Stacey decides the budget account charged. How are purchases of books, Linda approves and places orders. Linda also orders and play equipment and supplies approves routine purchases of supplies such as construction handled? paper, glue, crayons... Discuss any open accounts in There are only two open accounts - a teacher supply the Preschool's name. company and a Safeway Grocery Store. All of the office staff have cards allowing them to charge purchases at these two stores. Purchases on open account generate a receipt, which is usually matched against a monthly bill before payment. Who has Preschool ATM Only Linda, but she sometimes lets other office sta use the cards? What is the purpose of card. It is used to get cash for field trips and teacher gifts. the cards? Is there a There is no restriction on the size of transactions, but Linda restriction on the size of approves card use in advance. withdrawals? Is prior authorization required? The Preschool has three bank Any of the office staff can transfer funds. Usually, funds are accounts: checking, business transferred to keep only the amount needed for disbursements savings and money market in the checking account. Transfers are done online. accounts. Who has authority to transfer funds between accounts? How often are transfers made? Is a dedicated computer used No. There are three computers in the office and transfers can to make transfers? Is it be made on either Linda's computer or Stacey's. The password protected? Are the computers are used for email and internet purchases also, but computers used also for both of them have security software installed and are email? password protected. The WiFi is password protected also. Is the office door locked? Is The door is not locked when the preschool is open. the office left unattended? Sometimes the office is unattended but not for very long at a time Who reconciles the checking Gloria reconciles the bank account each month. account? How often? What is done with checks There really is no formal policy. outstanding for many months? Describe how payroll is All employees, except for Linda, use a clock to record time. processed. Stacey totals biweekly payroll amounts, and employees review and sign their summaries. Linda reviews the payroll numbers. Payroll amounts are sent online to ADP for processing by either Stacey or Linda, both of whom have passwords that change periodically. ADP tracks vacation and sick pay totals to date, writes checks and prepares W-2 forms. Linda documents any payroll changes using infomation from withholding forms. The church Staff Parish Committee is required to authorize changes in pay rates. After Linda and Stacey review payroll amounts from ADP, checks are disbursed manually. Payroll records are kept in a locked file and access is controlled somewhat. What is the role of the Advisory only. Linda was hired by the Staff Parish Preschool board? Committee of Comerstone Church and reports directly to the senior pastor. How many weeks of vacation Vacation is based on how long an employee has been does each employee receive? working. The Preschool closes for one week in late August and one week between Christmas and New Year. The maximum number of vacation days, in addition to these two weeks, is three weeks. Who handles Preschool All three staff are involved in most of the management and responsibilities when an office accounting activities. When one is absent, the others step in staff member is on vacation? to handle the job. The exception is Gloria. They generally wait for her to come back from vacation to reconcile bank accounts Table 4 Notes from Preschool Review Procedures Followed 1. Using the monthly check register, I verified disbursements against requests for payment or a bill and documentation of expenditures. 2. I compared deposits, disbursements, and supporting documents with the bank statement. These tests were made for three months in 2015. I verified the primary bank checking account reconciliation for three months. 3. I checked payroll hours worked against timesheets and the payroll company statements for three payrolls. Exceptions In general, controls are weak in the preschool. Procedures designed to reduce errors are not consistently followed. The following issues, at a minimum, need to be resolved. 1. Disbursements by checks frequently were made without receipts or documentation. Large transactions using a debit card were made with no primary bank checking account reconciliation for three months. 3.I checked payroll hours worked against timesheets and the payroll company statements for three payrolls. Exceptions In general, controls are weak in the preschool. Procedures designed to reduce errors are not consistently followed. The following issues, at a minimum, need to be resolved. 1. Disbursements by checks frequently were made without receipts or documentation. Large transactions using a debit card were made with no documentation or explanation. In the month of December alone, $1,410.30 of debit withdrawals and $1,364.15 of checks were processed without any form of documentation. Some of these expenditures recur each month. 2. Documentation has improved for authorization of payroll; however, I found many timesheets unsigned by either the employee or supervisor. Calculation errors were made in determining hours worked, but were corrected in the subsequent pay period. 3. In the month of April, both the deposit worksheet and deposit slip for $10,062.80 were missing. Additionally, deposit worksheets often were not double- checked and only one signature was present. REFERENCES Bierstaker J. L... J.E. Hunton and J.C. Thibodeau. 2009. Documentation and Business process Flowcharts Help or Hinder an Auditor's Ability to identify Missing Controls? Auditing: A Journal of Practice & Theory 28: 79-94. California Department of Social Services. 1998. Code of Regulations Title 22, Div. 12. Sections 1021.6-1012.17. Sacramento, CA: Department of Social Services. Committee on Sponsoring Organizations of the Treadway Commission (COSO). 2013. Internal Control - Integrated Framework. New York, NY: AICPA. IBISWorld. 2012. Child Day Care Services in the U.S. U.S. Industry Reports. Santa Monica, CA: IBISWorld. KPMG. 2014. Better Understanding the Process through Flowcharting: An Implementation Guide Amstelveen, Netherlands: KPMG. Available at: http://www.execed.kpmg.com/content/PDF/Flowcharting-Implementation- Guide.pdf Laughlin, L. 2013. Who's Minding the kids? Child Care Arrangements: Spring 2011. Current Population Reports. Washington, D.C.: U.S. Census Bureau. May, C. B. and G.S. May. 2014. Effective Writing: A Handbook for Accountants. 10th CASE: WHO'S IN CONTROL OF THE ARK? Sara Green released her seat belt and reached into the back seat of her car for the list of audit and control questions she had prepared for the director of the Ark Preschool. She paused, listening to the sounds of children's laughter, before closing the car door and walking into the building. Sara's two children had attended the Ark Preschool and she stood for a moment in the hallway as memories washed over her. Sara remembered Thanksgiving dinners with her children dressed in grocery bag costumes of Native Americans and Pilgrims, Mother's Day teas with cookies made by children and teachers, and the annual fall festivals. Startled from her reverie by slamming doors, Sara made her way to the preschool office. Sara entered a tiny office crammed with three desks, computers, boxes, and supplies, and was surprised to see three middle-aged women waiting anxiously for her. After clearing papers from the only empty seat, Sara greeted the preschool director, the education administrator, and the office assistant. The director and administrator run the preschool on a daily basis handling tuition receipts, bill payments, crying children, worried parents and tired teachers. The part-time office assistant, a former engineer, primarily records transactions into a Quicken system and reconciles bank statements. Sara had asked to meet with the administrator to ask a few questions about organizational goals and accounting processes at the preschool, but all three wanted to take part in the conversation. Sara settled into her chair and pulled out her list of questions. After briefly explaining the importance of internal control, she asked the staff about preschool operating, reporting and compliance objectives. They responded that operating objectives of the Ark Preschool include financial solvency, sufficient cash when needed, reduction of waste, effective scheduling of teachers to minimize overtime, and protection of preschool equipment from theft. Their financial reporting objectives include monthly budget updates, timely reconciliation of bank accounts, and reliable annual reports to Cornerstone Church. The most important compliance objective is adherence to wage and labor laws, federal and state income reporting regulations, and state preschool licensing requirements. Sara listened carefully as the administrator answered questions with the director and assistant adding their comments. Ringing telephones and teachers clocking out at the end of the day interrupted the interview, but Sara quickly realized all three administrators were clearly invested in the preschool and we were eager to explain how it worked. She leaned forward and started taking notes. 1 Child Care in the United States By the early 2010's, childcare had grown to be a $47 billion industry in the United States alone (IBISWorld 2012). In 2012, 65% of women with children aged three to five worked outside of the home, requiring assistance with child care (U.S. Census Bureau 2012). A patchwork of parents, family members, nonrelatives in the home, and external providers take care of children under school-age. Most home- based providers care for the children of no more than two families and are located in private homes, Day care centers generally care for 50 to 100 children, and are either for-profit corporations or not-for-profits sponsored by churches, community centers, parent cooperatives or Head Start (Laughlin 2013). State and local regulations ensure facilities are safe, supervision is adequate and children are protected. Safety inspections are common, but the greatest regulatory issue for most childcare facilities is the maintenance of adequate ratios of children to staff members. While regulations vary across the United States, all states place limits on the number of children under the supervision of each caregiver. For example, California's Title 22 (1998) requires that a single caregiver attend to no more than four infants, six toddlers from 18 to 30 months, or twelve children between age two and kindergarten. Staffing is a major issue for most preschools and it is difficult to attract caregivers who are both qualified and willing to work long hours for modest pay. Over 441,000 individuals were employed as preschool teachers in 2014, the average annual pay was $32,040, and most jobs required an associate's degree (Bureau of Labor Statistics 2014). Jobs are expected to grow by 6.7% over the period from 2014 through 2024. | The Ark Preschool The Ark Preschool is a not-for-profit preschool operating as an outreach ministry of the Cornerstone Church. It opened in 1985 when the first director saw a need for quality childcare in the community. Over time, the school adapted to meet the needs of both families who were members of the church and families in the community, and expanded operations to provide full-day childcare from infancy to school age. As an outreach ministry of the church, the preschool's purpose is to provide quality care and early education in a loving environment, and the preschool prides itself on its family feel. In its first ten years, the preschool was indeed a close- knit family with the director employing four of her daughters as teachers. The preschool has employed several directors since 1985, but the mission has remained the same: to celebrate the spirit and encourage the development of each child. A day at the preschool includes story time, alphabet and counting games, outdoor play, nature walks, water play, crafts for small motor skills, music and singing. At any time, between 60 and 75 children are enrolled at the preschool either as full-time or part-time students. Annual tuition has grown to $709,596 in 2015, an average of $59,000 per month. Expenses in 2015 total $708,459, with the preschool operating essentially in a break-even mode. The largest expenditures are for payroll and employee benefits, but the preschool also pays $3,200 per month for space shared with the church. Current tuition rates are reported in Table 1. As is true of many not-for-profit organizations and small businesses, the Ark Preschool maintains a small administrative staff. In addition to the director and education administrator, the preschool employs 15 part-time and full-time teachers, a resource specialist, and a part-time office assistant. Both the director and administrator have early childhood education credentials and serve as substitute teachers when needed. Linda Gonzalez, the preschool director, is responsible for the overall management of the school, including teacher hiring and training, program planning, community relations and coordination with the sponsoring church. Linda meets quarterly with the preschool advisory board, comprised of five parents of preschool children, one of which is also a church member. Linda is directly responsible to the senior minister of the Cornerstone Church and its Staff-Parish Committee. The education administrator, Stacey Okada, assists the director in daily activities and is responsible for general financial oversight, reviewing and approving financial expenditures, deposits, and the transfer of funds between checking and savings accounts. The preschool recently hired Gloria Lloyd, the mother of several former students, to handle record-keeping activities and bookkeeping on a part- time basis. Sara Green Sara began her career as a CPA in a small regional accounting firm. After several years, she returned to graduate school for an advanced degree and currently teaches accounting at a local university. Although she no longer practices as a CPA, Sara keeps her license active by completing 40 continuing education units each year. Her children attended the Ark Preschool when they were younger, and her family are members of Cornerstone Church. Sara also served on the church finance committee for five years but resigned when her evening teaching responsibilities interfered with committee meetings. Ken Robinson, a retiree with little finance experience who served as church treasurer, asked Sara to perform the annual review of the church and preschool financial records. Knowing the demands of performing an audit and the demands miscalculations of hours worked, most of them a half-hour or less, Sara was happy to see that payroll summaries generally were accurate. This was an improvement over prior years. Sara turned to reconciliations of bank statements, which Gloria completed on a monthly basis. Using bank statements and the preschool check register, Sara reconciled the December 31, 2015 cash account and found it agreed with Gloria's reconciliation. Beginning with the January statement and the computer ledgers, she matched bank disbursements with amounts recorded on the preschool records and supporting documentation. She knew the preschool had entered into automatic payments for recurring disbursements for advertising with Yelp, an online publisher of crowd-sourced business reviews, but frowned when she saw several ATM payments lacking any documentation, Sara listed general principles for achieving internal control over cash for a small organization: No employee should handle a transaction from beginning to end. Separate cash handling from record keeping. Centralize cash handling as much as possible. Record cash receipts on a timely basis. Make deposits daily. Encourage parents to receive receipts. Make all expenditures by check or electronic funds transfer. An employee not handling cash should prepare monthly bank reconciliations. An appropriate administrator should review the reconciliations monthly. Compare cash receipts and disbursements to forecasted amounts and budgets. Sara summarized her concerns on a legal pad, presented in Table 4. Sara sat back in her chair and thought about the children, teachers and parents at the preschool as well as the congregation at Cornerstone Church. She had read news reports of other schools using state funds for employee vacations, mortgage payments and shopping sprees. She believed the director and office staff were caring people, but was concerned with the lack of control procedures. Sara was reasonably confident that no fraudulent activity had taken place at the preschool, but knew additional controls needed to be implemented Schedule Monday through Friday Half day 9am - 3pm 7am - 6pm Table 1 The Ark Tuition Schedule Class Ages Monthly Rate 2/3 combo $843.00 3 and 4 826.00 2/3 combo 1,000.00 3 and 4 975.00 2/3 combo 1200.00 3 and 4 1110.00 2/3 combo $575.00 3 and 4 560.00 2 and 3 746.00 3 and 4 670.00 2/3 combo 955.00 3 and 4 945.00 Mon/Wed/Friday Half-day 9am-3pm 7am - 6pm Tues/Thursday Half day 9am - 3pm 7am-6pm 2/3 combo 3 and 4 2/3 combo 3 and 4 2/3 combo 3 and 4 $390.00 370.00 513.00 447.00 655.00 648.00 Infants and Toddlers 7am -6pm 2 days 3 days 4 days 5 days $740.00 1100.00 1428.00 1560.00 Table 3 Internal Control Interview Questions and Answers Questions Answers Do families receive a tuition Each month Gloria prepares and emails every family a bill. bill? Who prepares it? How often are families billed? Who records tuition payments Stacey prepares a listing of payments and Gloria records them in the student accounts? in student accounts How do parents pay tuition? Most pay by check, but a few pay with cash. a By check? Cash? Automated bank payments? Is tuition paid in person? By Some parents mail payments, but most of them drop off mail? payments when they bring their children to school. If staff are in the office, parents pay in person, otherwise, they use the locked drop-box on the office door. Either Stacey or Linda removes payments from the drop-box. Are receipts given? Only if a parent asks for one, but that almost never happens. Explain the process for Linda stampa checks with an endorsement stamp and prepares handling tuition payments and the deposit. Stacey checks most deposits for accuracy and deposits. Linda walks the deposits to the bank sharing the same parking lot. Tuition is deposited on the day received, unless payment is received after the bank closes. All undeposited cash and/or checks are kept in a locked desk drawer. Is the fee schedule published The internet fee schedule (reproduced in table 3) is correct. on the internet correct? Are Discounts are given to siblings of current students, any discounts given? Are employees' children and children of church members. Some they standard for all children? scholarships are given based on need, but there is no formal policy. Is there a petty cash fund? Not exactly. Many parents don't want to bring in separate What are its uses? Who has payments for field trips or gymnastics classes, so they are access? Where is it kept? billed for these extra activities along with tuition. Still, teachers need cash for entrance fees and gas, so we withdraw cash from the bank in advance and hold it in a cash box we keep locked in a cabinet. Stacey and Linda have access to the cash Does the Preschool allow any There is only one automated payment for Yelp. We receive automated withdrawals from an email invoice but don't print it out. The Yelp account is in its bank account? Is an the Preschool's name. invoice received? Are all automated payments for accounts in the Preschool's name? Do you require an invoice for Most of the time. We pay Don Cuesta for gym and motion all payments? Are there any classes without an invoice. Most bills are received by mail. exceptions? Who approves payment of No one. invoices? Who has check signing Linda, Stacey and Gloria can sign, but usually Stacey authority? prepares and signs the checks. Stacey marks the invoices as paid and files them in a folder. Where are unused checks In a locked desk drawer. stored? Describe the policy on Teachers and office staff get prior approval for purchases, but reimbursement of expenses. Is there is no formal process or form required. They usually talk there a limit on dollar with Linda for approval. There is no limit if prior approval is amounts? obtained. Either Linda or Stacey decides the budget account charged. How are purchases of books, Linda approves and places orders. Linda also orders and play equipment and supplies approves routine purchases of supplies such as construction handled? paper, glue, crayons... Discuss any open accounts in There are only two open accounts - a teacher supply the Preschool's name. company and a Safeway Grocery Store. All of the office staff have cards allowing them to charge purchases at these two stores. Purchases on open account generate a receipt, which is usually matched against a monthly bill before payment. Who has Preschool ATM Only Linda, but she sometimes lets other office sta use the cards? What is the purpose of card. It is used to get cash for field trips and teacher gifts. the cards? Is there a There is no restriction on the size of transactions, but Linda restriction on the size of approves card use in advance. withdrawals? Is prior authorization required? The Preschool has three bank Any of the office staff can transfer funds. Usually, funds are accounts: checking, business transferred to keep only the amount needed for disbursements savings and money market in the checking account. Transfers are done online. accounts. Who has authority to transfer funds between accounts? How often are transfers made? Is a dedicated computer used No. There are three computers in the office and transfers can to make transfers? Is it be made on either Linda's computer or Stacey's. The password protected? Are the computers are used for email and internet purchases also, but computers used also for both of them have security software installed and are email? password protected. The WiFi is password protected also. Is the office door locked? Is The door is not locked when the preschool is open. the office left unattended? Sometimes the office is unattended but not for very long at a time Who reconciles the checking Gloria reconciles the bank account each month. account? How often? What is done with checks There really is no formal policy. outstanding for many months? Describe how payroll is All employees, except for Linda, use a clock to record time. processed. Stacey totals biweekly payroll amounts, and employees review and sign their summaries. Linda reviews the payroll numbers. Payroll amounts are sent online to ADP for processing by either Stacey or Linda, both of whom have passwords that change periodically. ADP tracks vacation and sick pay totals to date, writes checks and prepares W-2 forms. Linda documents any payroll changes using infomation from withholding forms. The church Staff Parish Committee is required to authorize changes in pay rates. After Linda and Stacey review payroll amounts from ADP, checks are disbursed manually. Payroll records are kept in a locked file and access is controlled somewhat. What is the role of the Advisory only. Linda was hired by the Staff Parish Preschool board? Committee of Comerstone Church and reports directly to the senior pastor. How many weeks of vacation Vacation is based on how long an employee has been does each employee receive? working. The Preschool closes for one week in late August and one week between Christmas and New Year. The maximum number of vacation days, in addition to these two weeks, is three weeks. Who handles Preschool All three staff are involved in most of the management and responsibilities when an office accounting activities. When one is absent, the others step in staff member is on vacation? to handle the job. The exception is Gloria. They generally wait for her to come back from vacation to reconcile bank accounts Table 4 Notes from Preschool Review Procedures Followed 1. Using the monthly check register, I verified disbursements against requests for payment or a bill and documentation of expenditures. 2. I compared deposits, disbursements, and supporting documents with the bank statement. These tests were made for three months in 2015. I verified the primary bank checking account reconciliation for three months. 3. I checked payroll hours worked against timesheets and the payroll company statements for three payrolls. Exceptions In general, controls are weak in the preschool. Procedures designed to reduce errors are not consistently followed. The following issues, at a minimum, need to be resolved. 1. Disbursements by checks frequently were made without receipts or documentation. Large transactions using a debit card were made with no primary bank checking account reconciliation for three months. 3.I checked payroll hours worked against timesheets and the payroll company statements for three payrolls. Exceptions In general, controls are weak in the preschool. Procedures designed to reduce errors are not consistently followed. The following issues, at a minimum, need to be resolved. 1. Disbursements by checks frequently were made without receipts or documentation. Large transactions using a debit card were made with no documentation or explanation. In the month of December alone, $1,410.30 of debit withdrawals and $1,364.15 of checks were processed without any form of documentation. Some of these expenditures recur each month. 2. Documentation has improved for authorization of payroll; however, I found many timesheets unsigned by either the employee or supervisor. Calculation errors were made in determining hours worked, but were corrected in the subsequent pay period. 3. In the month of April, both the deposit worksheet and deposit slip for $10,062.80 were missing. Additionally, deposit worksheets often were not double- checked and only one signature was present. REFERENCES Bierstaker J. L... J.E. Hunton and J.C. Thibodeau. 2009. Documentation and Business process Flowcharts Help or Hinder an Auditor's Ability to identify Missing Controls? Auditing: A Journal of Practice & Theory 28: 79-94. California Department of Social Services. 1998. Code of Regulations Title 22, Div. 12. Sections 1021.6-1012.17. Sacramento, CA: Department of Social Services. Committee on Sponsoring Organizations of the Treadway Commission (COSO). 2013. Internal Control - Integrated Framework. New York, NY: AICPA. IBISWorld. 2012. Child Day Care Services in the U.S. U.S. Industry Reports. Santa Monica, CA: IBISWorld. KPMG. 2014. Better Understanding the Process through Flowcharting: An Implementation Guide Amstelveen, Netherlands: KPMG. Available at: http://www.execed.kpmg.com/content/PDF/Flowcharting-Implementation- Guide.pdf Laughlin, L. 2013. Who's Minding the kids? Child Care Arrangements: Spring 2011. Current Population Reports. Washington, D.C.: U.S. Census Bureau. May, C. B. and G.S. May. 2014. Effective Writing: A Handbook for Accountants. 10th

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts