1. Using Value Chain analysis, identify three segments in the Value Chain in which the company creates value. Provide an example for each. 2. Using Resource Based View, identify two strategic resources the company possesses that can be used as competitive advantages. You must identify whether the strategic resources are tangible or intangible. 3. Analyze at least three of the aspects of the general environment of the industry the company is in. 4. Analyze three of the Five Forces for the industry the company is in.

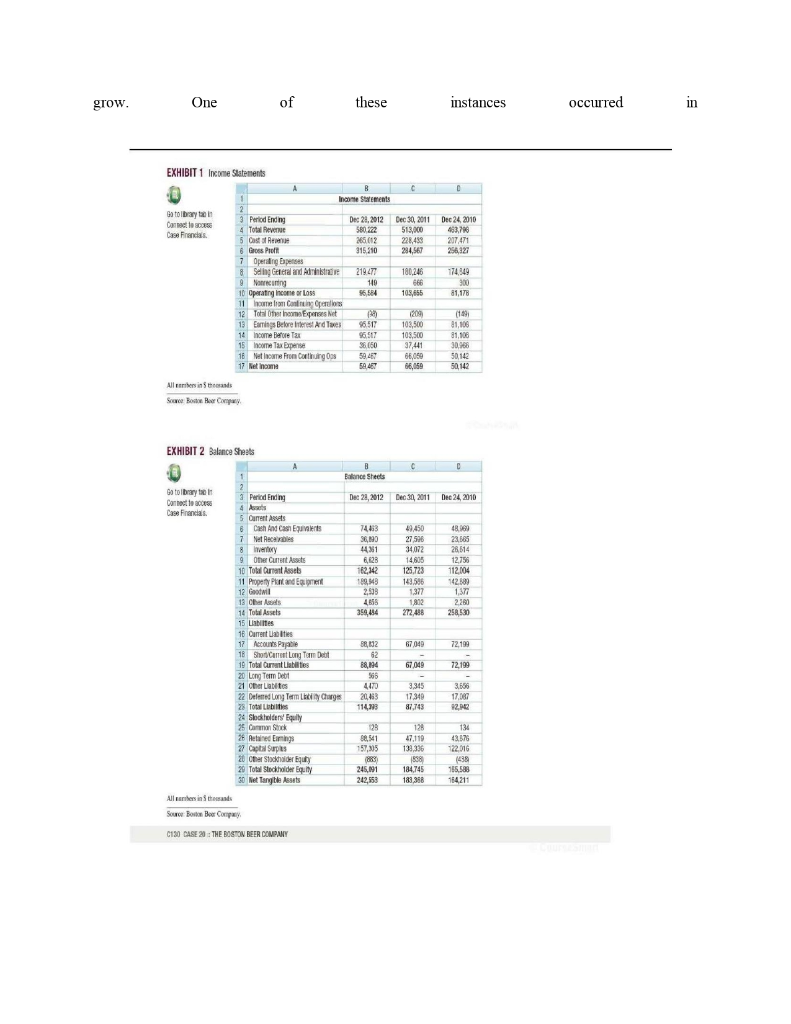

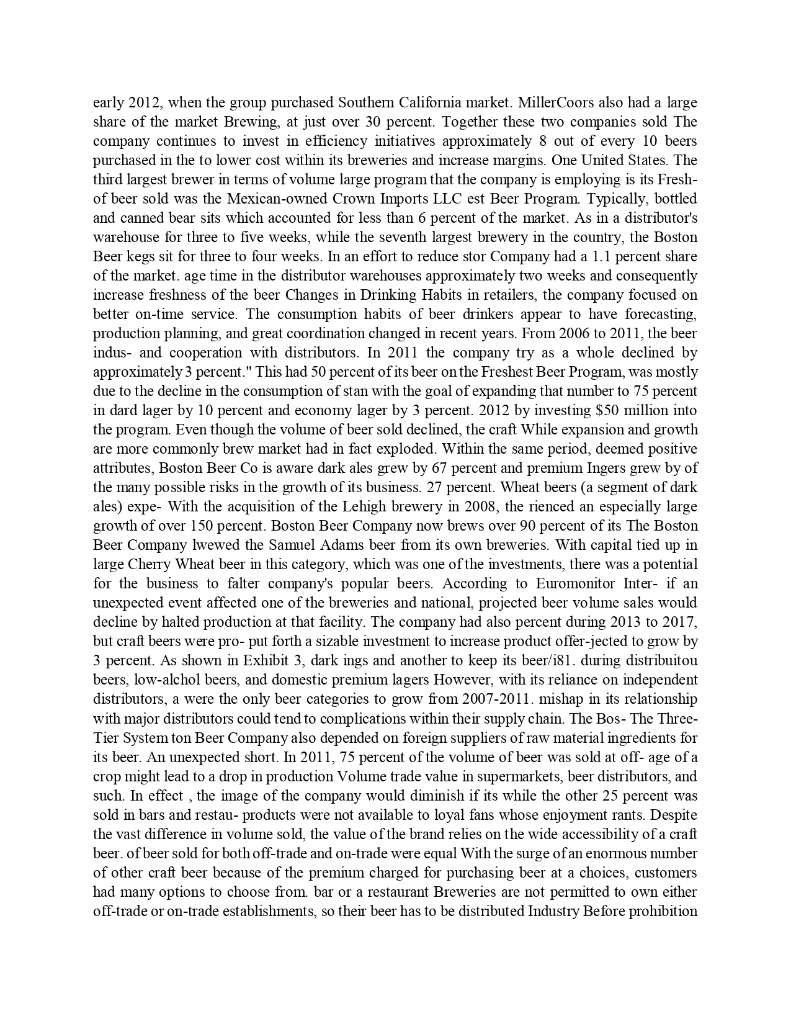

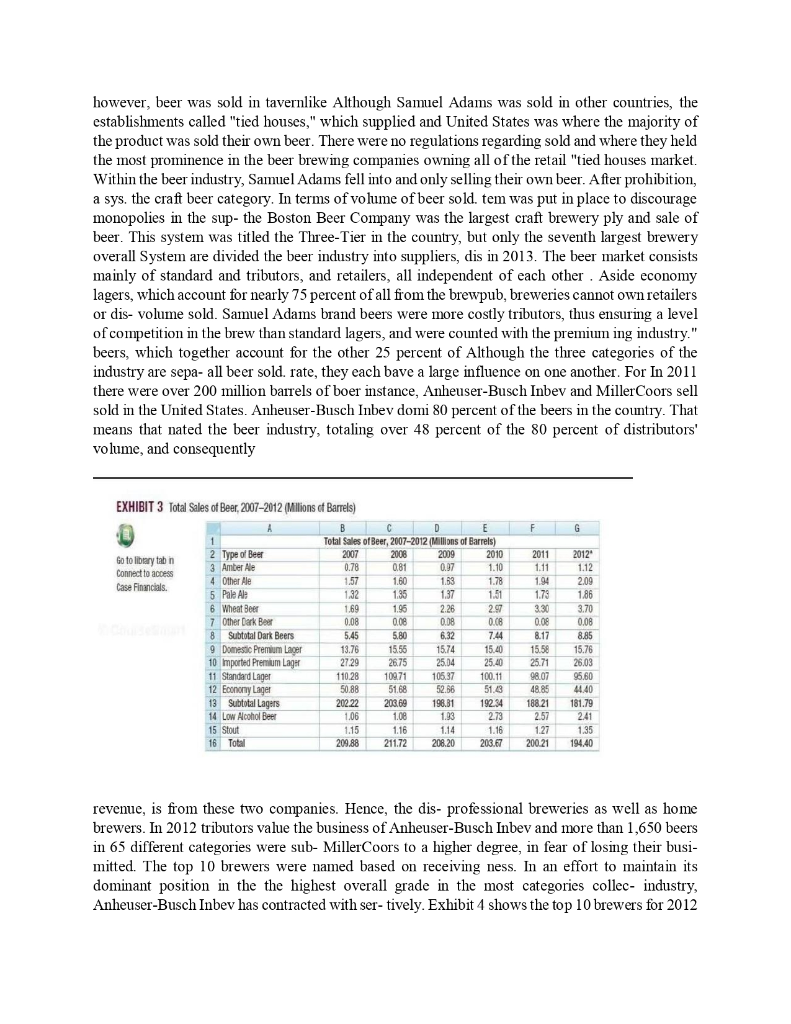

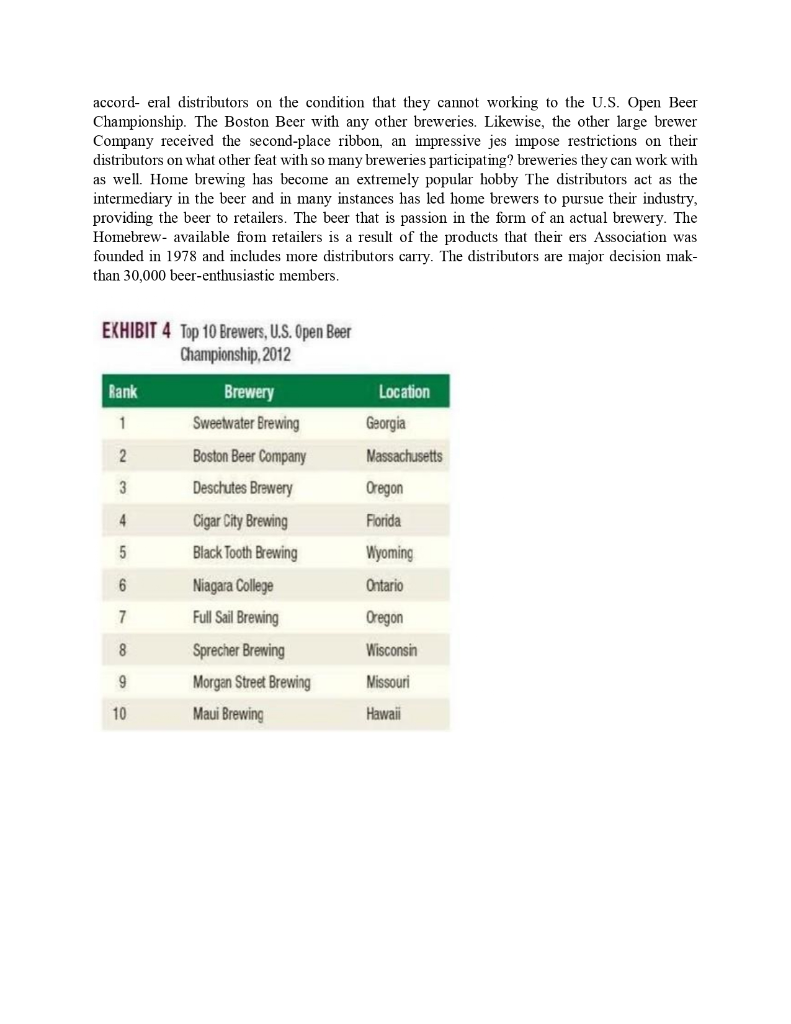

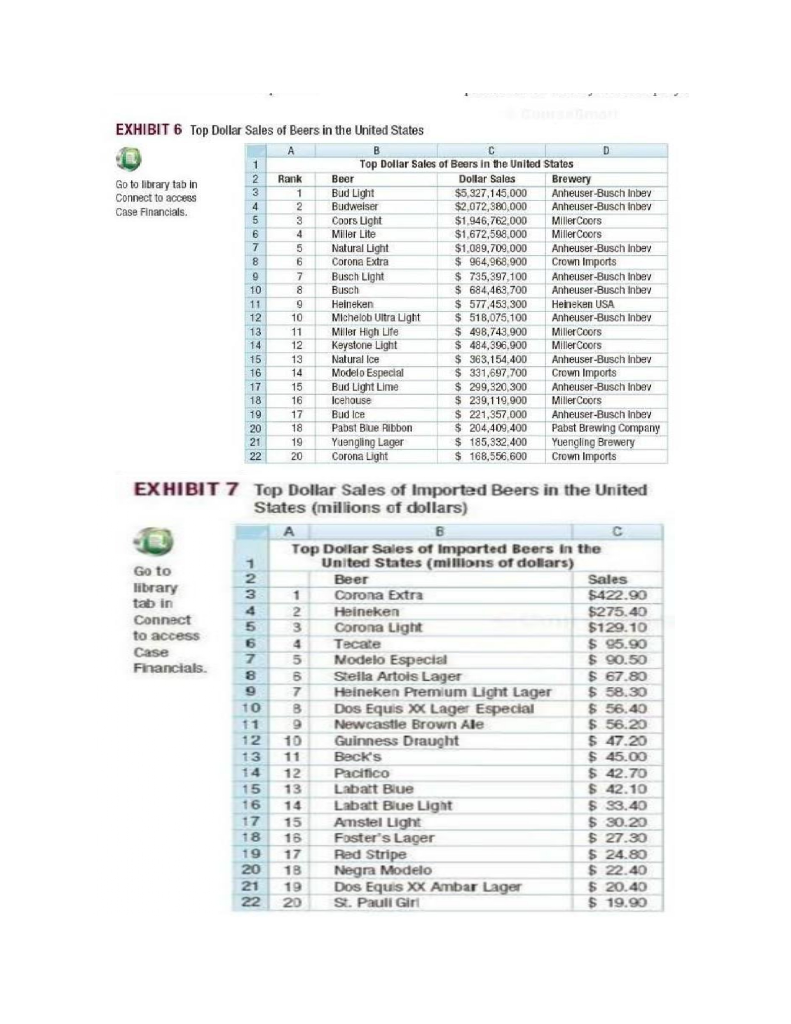

CASES CASE 20 THE BOSTON BEER COMPANY* The Boston Beer Company, known for its Samuel Adams more of the market. As the country's largest craft brew- brand, is the largest craft brewery in the United States, ery, the Boston Beer Company had revenue of over $500 holding a 1 percent stake in the overall beer market.' million in 2011 and sold over 2 million barrels of beer. faces growing competitive threats from other breweries. Other large craft breweries include New Belgium Brewing both large and small. In the past several years, the beer Company and Sierra Nevada Brewing Company, which industry as a whole has been on a decline, while sales of sold over 580,000 and 720,000 barrels of beer in 2011, wines and spirits have increased. The Boston Beer Com respectively. In addition, some smaller breweries have pany competes within the premium beer industry, which been merging to take advantage of economies of scale and includes craft beer and premium imported beers like enhance their competitive position. Heineken and Corona. Although the beer industry has been According to Boston Beer Company, there are on a decline, the premium beer industry has seen a small approximately 770 craft breweries that ship their prod- amount of growth, and the craft beer industry has seen a wet domestically, up from 420 in 2006. There are also an surge in popularity. Because of this success of the craft expected 800 craft breweries in the planning stage, expect- breweries in particular the major breweries have taken ing to be operational within the next 2-3 years. Boston notice and many new craft breweries have sprung up. Beer Company assumes that 300 of those 800 will be Anheuser-Busch Inbev and MillerCoors, LLC, account shipping breweries (ie, breweries that sell their prod- for over 80 percent of the beer market in the United uct beyond their local market). Thus, within the next few States. They have caught on to the current trend Andy Glede Samuel Adams beer may be competing with over beer industry toward higher quality beers and have started 1,000 other craft breweries around the country releasing their own higher quality beers. For example, The Boston Beer Company competes not only with Anheuser-Busch Inbev has released Bud Light Wheat and domestic craft breweries but also with premium beer Bud Light Platinum in an effort to provide quality beers to imports, such as Heineken and Corona, which sell beer their loyal customers. MillerCoors makes Blue Moon beer, in a similar price range, Like Anheuser-Busch Inbev and which is the most popular craft beer in the United States. MillerCoors, Heineken and Corona have large financial Anheuser-Busch Inbev released Shock Top to combat the resources and can influence the market. It is projected that popularity of Blue Moon. These companies have also premium imported beers will grow by 6 percent over the begun to purchase smaller craft breweries, whose products next five years, have been rising in popularity. Anheuser-Busch Inbev pur The Brewers Association defines a craft brewery as chased Goose Island Brewing Company in March 2011. brewing less than six million barrels per year and being less MillerCoors has started a group within the company titled than 25 percent owned or controlled by another economic Tenth and Blake Beer Company for the purpose of creating interest. Maintaining status as a craft brewery can be impor- and purchasing craft breweries. According to MillerCoors tant for image and therefore, sales. Thus, MillerCoors CEO Tom Lang, the plan is to grow Tenth and Blake Beer purchased less than a 25 percent stake in Terrapin Beer, still Company by 60 percent within the next three years. The allowing it to maintain its craft brewery status. The size of two major companies plan to use their massive marketing the Boston Beer Company, however, is an issue. With con- budgets to tell people about their craft beers. tinued growth, the brewery could potentially increase its According to the Brewers Association, 1.940 craft volume output to more than 6 million barrels per year, thus breweries and 1,989 total breweries operated in the losing its craft brewery status. Furthermore, with the size United States for some or all of 2011. While craft brewer of the company and their ability to market nationwide, the jes account for over 97 percent of all the breweries in the company runs the risk of alienating itself from other craft United States, they only produce approximately 25 percent breweries who believe Samuel Adams no longer fits the of all beer sold. However, with the rise in popularity of profile. Many craft breweries already believe the company, premium beers, the craft breweries will continue to grab which has been public since 1995, is more concerned with making money than with providing quality beer and edu- This case was developed by graduate students Peter J. Courtney and Eric S. cating the public on craft beers. Engelson and Professor Ahn B. Eisner Pace University, Material has been Size does have advantages, of course, with more money drawn from published sources to be used for dass discussie. Copyright for marketing and, especially in the beer business, with 2013 Alan B. Eister distribution. A heavy complaint for all craft breweries is C128 CASE 20 : THE BOSTON BEER COMPANY the difficulty they have distributing their product in the at two different prices, $15 to loyal customers and $20 ument three-tier system (discussed in a later section). The through an IPO run by Goldman Sachs. Koch decided large breweries have power over the independent distribu- to reward his loyal customers by advertising the stock tors because they account for most of their business. Thus, offering on the packages of his six-packs, estimating that they can influence the distributors and make it difficult for 30,000 buyers would be interested. He believed that those craft breweries to sell their product. Because of its size, who enjoyed the beer and supported it should be the ones the Boston Beer Company has fewer problems with dis- who have a stake in the company. After 100,000 potential tributors than its smaller competitors do. Consequently, the investors sent checks in, Koch randomly chose 30,000. company has less in common with other craft breweries Managers from Goldman Sachs were upset that they did and more with the major breweries in regards to distribu- not receive the lowest-price offering. Koch owns 100 per- tion. This is good for Boston Beer Company's distribution, cent of Class B Common stock, of which all major deci- but might be bad for its image. One brewer from The Defi-sions for the company are made. This is seen as a risk ant Brewing Company in Pearl River, New York, said that to potential investors because Koch can make important The Boston Beer Company was becoming too large to be decisions on the strategy for the company without receiv- considered a call brewery and that their substantial con ing approval nections with distributors contributed to this notion. Continued success for the business led to the purchase As the above discussion makes clear, The Boston Beer of a large brewery in Cincinnati in 1997. Since 2000, Company is facing a difficult competitive environment. Samuel Adams has won more awards in international beer They are facing direct competition from both larger and tasting competitions than any other brewery in the world. snaller breweries and from premium imported beers. In 2008 the Boston Beer Company purchased a world- Some of the smaller craft breweries are growing quickly class brewery in Lehigh, Pennsylvania, to support growth and want to be larger than the Boston Beer Company As of 2013, the Boston Beer Company was the larg. Other craft breweries feel that the Boston Beer Company est craft brewery in the United States, brewing over two is too large already. Thus, while further growth would be million barrels of Samuel Adams beer, but still only made beneficial in terms of revenue, growing too large could up approximately 1 percent of the total U.S. beer market. negatively affect the company's status as a craft brewery The company has expanded its selections to over 50 beer and the perceptions of its customers. The company must flavors, including seasonal and other flavorful beers, such pay close attention to maintaining its image for the grow as Samuel Adams Summer Ale, Samuel Adams Cherry ing customer base of premium beer drinkers. Wheat, and Samnuel Adams Octoberfest, as well as the non-beer brands Twisted Tea and HardCore Cider. The Boston Company Background Beer Company planned to use the profits gained from its Jim Koch started the Boston Beer Company in 1984 along non-beer brands to invest in Samuel Adams and build a with fellow Harvard MBA graduates Harry Rubin and stronger portfolio. Revenue for the company grew from Lorenzo Lamadrid. The company began with the sale of $380 million in 2007 to over $500 million in 2011, while the now popular Samuel Adams Boston Lager, named operating costs grew from $150 million to $180 million after the famous American patriot who was known to have Net income tripled from $22 million to $66 million in the been a brewer himself. The recipe for the lager was passed same period (see Exhibits 1 and 2). In July 2012, the com- ing back to the 1860s. Koch began home brewing the beach pany was selling at $113, nearly $100 over the initial pub- lic offering from 1995. in his own kitchen and soliciting local establishments in The goal of the Boston Beer Company was to become Boston to purchase and sell it. Just one year after its initial the leading brewer in the premium beer market. As of sales, Samuel Adams Boston Lager was voted "Best Beer 2013, it was the largest craft brewery, but it trailed Crown in America" at the Great American Beer Festival in Den- Imports, LLC, and Heineken USA in the premium beer ver, Colorado. In 1985 Samuel Adams grew immensely market. The company planned to surpass the large import- and sold 500 barrels of beer in Massachusetts, Connecti-ers by increasing brand availability and awareness through cut, and West Germany." advertising, drinker education, and the support of its over To avoid the high up-front capital costs of starting a 300-member salesforce. The salespeople for the company brewery, Koch contracted with several existing brewer- have a high level of product knowledge about beer and the ies to make his beer. This allowed the production of the brewing process and use this to educate distributors and the Boston Lager to grow quickly from the relatively small public on the benefits of Samuel Adams. In 2011 the Bos- quantities Koch could brew himself. Growth continued ton Beer Company formed a subsidiary called Alchemy after that, and in 1988 the Boston Beer Company opened & Science to seize new opportunities in the craft brew-a brewery in Boston. By 1989 the Boston Beer Companying industry. The purpose of this group will be to iden- produced 63,000 barrels of Samuel Adams beer annually. tify better beer ingredients, methods for better brewing, The company went public in 1995, selling Class A and purchasing opportunities for any breweries that would Common stock to potential investors. The stock was sold help the business grow. One of these instances instances occurred in EXHIBIT 1 Income Statements A Income Statements Gatobrary Carreto som Case France Dec 21, 2012 580 222 265.012 315510 Dec 30, 2011 Dec 24, 2010 513,000 463,786 228,453 207,471 284,567 25.12 3 Period Ending 4 Total Revenue 5 Castor 6 Gross Pro 7 Operating Expenses 8 Saling General and Art 9 Nang 10 Operating income or on 11 comme on Continuing Operations 12 Total transport 13 Earrings Before does 14 come forex 15 Toome Tax Expense 18 Nelone Pro Carthurgas 17 Retinama 21947 119 $6,584 180.246 666 105,055 174.349 300 81,178 $6517 96.517 56,060 59.407 5447 103,500 103,500 37.441 66,050 66,059 (1991 21,106 81,906 30.966 50.143 50.142 All in Serce Bo Beer Copy EXHIBIT 2 Balance Sheets c C Ballince Sheets Gatoibrary Contacto Case Financials Dec 21, 2012 Dec 30, 2011 Dec 24, 2010 74.363 36.990 4431 6,028 162,342 189MB 49.450 27576 34072 14.603 125.722 149.586 1377 1802 272,488 48.000 23.03 28,514 12,750 112.104 142.829 187 2260 2585 2009 4055 359,414 3 Periodinding 4 5 Current Assets 6 Cash And Cash Equivalents 7 Net Recals 8 livery 9 Other Content Assets 10 Total Quran Assets 11 Property Plant and Equipment 12 Goodwill 1. CHI MINH 14 Total Assets 15 Listites 16 Current Us 17 Accounts Payable 1B Shop Cantom Tom Dot 19 Total Current Liabilities 20 Long Term Dot 21 Charlantes 22 Deleted Long Term Charges 28 Total Lubis 24 Sledilders' Equity 25 Cannon Stock 26 Retained Emings 27 Capital Saplus 20 Other Stadtquly 29 Total Stockholde Equity 30 let Tangible esats 39,132 67,049 72,199 68,194 67049 72.199 4471 20,413 114 9,345 17.340 87.743 3.656 17.00 92.062 128 47.119 133 336 29541 157,305 X 245.1991 242,553 136 43576 22.016 (438 155.588 164,211 184,745 183.358 All abers in the Sou Boe Boer Compay C130 CASE 20THE BOSTON BEER COMPANY early 2012, when the group purchased Southern California market. MillerCoors also had a large share of the market Brewing, at just over 30 percent. Together these two companies sold The company continues to invest in efficiency initiatives approximately 8 out of every 10 beers purchased in the to lower cost within its breweries and increase margins. One United States. The third largest brewer in terms of volume large program that the company is employing is its Fresh- of beer sold was the Mexican-owned Crown Imports LLC est Beer Program. Typically, bottled and canned bear sits which accounted for less than 6 percent of the market. As in a distributor's warehouse for three to five weeks, while the seventh largest brewery in the country, the Boston Beer kegs sit for three to four weeks. In an effort to reduce stor Company had a 1.1 percent share of the market. age time in the distributor warehouses approximately two weeks and consequently increase freshness of the beer Changes in Drinking Habits in retailers, the company focused on better on-time service. The consumption habits of beer drinkers appear to have forecasting, production planning, and great coordination changed in recent years. From 2006 to 2011, the beer indus- and cooperation with distributors. In 2011 the company try as a whole declined by approximately 3 percent." This had 50 percent of its beer on the Freshest Beer Program, was mostly due to the decline in the consumption of stan with the goal of expanding that number to 75 percent in dard lager by 10 percent and economy lager by 3 percent. 2012 by investing $50 million into the program. Even though the volume of beer sold declined, the craft While expansion and growth are more commonly brew market had in fact exploded. Within the same period, deemed positive attributes, Boston Beer Co is aware dark ales grew by 67 percent and premium Ingers grew by of the many possible risks in the growth of its business. 27 percent. Wheat beers (a segment of dark ales) expe- With the acquisition of the Lehigh brewery in 2008, the rienced an especially large growth of over 150 percent. Boston Beer Company now brews over 90 percent of its The Boston Beer Company lwewed the Samuel Adams beer from its own breweries. With capital tied up in large Cherry Wheat beer in this category, which was one of the investments, there was a potential for the business to falter company's popular beers. According to Euromonitor Inter- if an unexpected event affected one of the breweries and national, projected beer volume sales would decline by halted production at that facility. The company had also percent during 2013 to 2017, but craft beers were pro- put forth a sizable investment to increase product offer-jected to grow by 3 percent. As shown in Exhibit 3, dark ings and another to keep its beer/i81. during distribuitou beers, low-alchol beers, and domestic premium lagers However, with its reliance on independent distributors, a were the only beer categories to grow from 2007-2011. mishap in its relationship with major distributors could tend to complications within their supply chain. The Bos- The Three- Tier System ton Beer Company also depended on foreign suppliers of raw material ingredients for its beer. An unexpected short. In 2011, 75 percent of the volume of beer was sold at off-age of a crop might lead to a drop in production Volume trade value in supermarkets, beer distributors, and such. In effect, the image of the company would diminish if its while the other 25 percent was sold in bars and restau- products were not available to loyal fans whose enjoyment rants. Despite the vast difference in volume sold, the value of the brand relies on the wide accessibility of a craft beer. of beer sold for both off-trade and on-trade were equal With the surge of an enormous number of other craft beer because of the premium charged for purchasing beer at a choices, customers had many options to choose from. bar or a restaurant Breweries are not permitted to own either off-trade or on-trade establishments, so their beer has to be distributed Industry Before prohibition however, beer was sold in tavernlike Although Samuel Adams was sold in other countries, the establishments called "tied houses," which supplied and United States was where the majority of the product was sold their own beer. There were no regulations regarding sold and where they held the most prominence in the beer brewing companies owning all of the retail "tied houses market. Within the beer industry, Samuel Adams fell into and only selling their own beer. After prohibition, a sys. the craft beer category. In terms of volume of beer sold. tem was put in place to discourage monopolies in the sup- the Boston Beer Company was the largest craft brewery ply and sale of beer. This system was titled the Three-Tier in the country, but only the seventh largest brewery overall System are divided the beer industry into suppliers, dis in 2013. The beer market consists mainly of standard and tributors, and retailers, all independent of each other. Aside economy lagers, which account for nearly 75 percent of all from the brewpub, breweries cannot own retailers or dis- volume sold. Samuel Adams brand beers were more costly tributors, thus ensuring a level of competition in the brew than standard lagers, and were counted with the premiun ing industry." beers, which together account for the other 25 percent of Although the three categories of the industry are sepa- all beer sold. rate, they each bave a large influence on one another. For In 2011 there were over 200 million barrels of boer instance, Anheuser-Busch Inbev and MillerCoors sell sold in the United States. Anheuser-Busch Inbev domi 80 percent of the beers in the country. That means that nated the beer industry, totaling over 48 percent of the 80 percent of distributors' volume, and consequently EXHIBIT 3 Total Sales of Beer, 2007-2012 (Millions of Barrels) F G Go to library tab in Connect to access Case Financials. 1 2 Type of Beer 3 Amber Ale 4 Other Ale 4 5 Pale Al: 6 Wheat Beer 7 Other Dark Bear 8 Subtotal Dark Beers 9 Domestic Premium Lager 10 Imported Premium Lager 11 Standard Lager 12 Economy Lager 13 Subtotal Lagers 14 Low Alcohol Beer 15 Stout 16 Total B D Total Sales of Beer, 2007-2012 Millions of Barrels) , 2007 2008 2009 2010 0.78 081 097 1.10 1.57 1.60 1.63 1.78 1.32 1.35 137 1.51 1.69 1.96 2.26 297 0.08 0.08 0.08 0.08 5.45 5.80 6.32 7.44 13.76 15.55 15.74 15.20 27.29 26.75 25.04 25.40 110.28 109.71 105.37 100.11 50.88 51.68 52.66 51.43 202.22 203.69 198,81 192.34 1.06 1.08 1.93 2.73 1.15 1.16 1.14 1.16 209.88 211.72 208.20 203.67 2011 1.11 194 1.79 3.30 0.08 8.17 15.58 25.71 98.07 48 88 188.21 2.57 1.27 200.21 2012 1.12 2.09 1.86 3.70 0.08 8.85 15.76 26.03 95,60 44.40 181.79 241 1.35 194.40 revenue, is from these two companies. Hence, the dis- professional breweries as well as home brewers. In 2012 tributors value the business of Anheuser-Busch Inbev and more than 1,650 beers in 65 different categories were sub- MillerCoors to a higher degree, in fear of losing their busi- mitted. The top 10 brewers were named based on receiving ness. In an effort to maintain its dominant position in the the highest overall grade in the most categories collec- industry, Anheuser-Busch Inbev has contracted with ser- tively. Exhibit 4 shows the top 10 brewers for 2012 accord- eral distributors on the condition that they cannot working to the U.S. Open Beer Championship. The Boston Beer with any other breweries. Likewise, the other large brewer Company received the second-place ribbon, an impressive jes impose restrictions on their distributors on what other feat with so many breweries participating? breweries they can work with as well. Home brewing has become an extremely popular hobby The distributors act as the intermediary in the beer and in many instances has led home brewers to pursue their industry, providing the beer to retailers. The beer that is passion in the form of an actual brewery. The Homebrew- available from retailers is a result of the products that their ers Association was founded in 1978 and includes more distributors carry. The distributors are major decision mak- than 30,000 beer-enthusiastic members. Location EXHIBIT 4 Top 10 Brewers, U.S. Open Beer Championship, 2012 Rank Brewery 1 Sweetwater Brewing 2 Boston Beer Company 3 Deschutes Brewery Georgia Massachusetts Oregon 4 Florida 5 Wyoming 6 Ontario 7 Cigar City Brewing Black Tooth Brewing Niagara College Full Sail Brewing Sprecher Brewing Morgan Street Brewing Maui Brewing Oregon 8 Wisconsin 9 Missouri 10 Hawaii Best Portfolio EXHIBIT 5 Top 10 Beer Categories in 2012 Best Beer Best Brewery Russian River Pliny the Elder Sierra Nevada Brewing Company Bell's Two Hearted Ale Dogfish Head Craft Brewery Dogfish Head 90 Minute IPA Stone Brewing Company Sierra Nevada Pale Ale Russian River Brewing Company Stone Arrogant Bastard Ale Bell's Brewery Bell's Hopslam New Belgium Brewing Company Sierra Nevada Celebration Firestone Walker Brewing Company Stone Ruination IPA Deschutes Brewery Sierra Nevada Torpedo Lagunitas Brewing Company North Coast Old Rasputin Founders Brewing Company Samuel Adams Boston Lager (31st) Boston Beer Company (11th) Boston Beer Company (41 beers) Dogfish Head Craft Brewery (34 beers) New Glarus Brewing Company (28 beers) Rogue Ales (27 beers) Bell's Brewery (26 beers) New Belgium Brewing Company (26 beers) Sierra Nevada Brewing Company (25 beers) Three Floyds Brewing Company 25 beers) Goose Island Brewing Company (23 beers) Great Divide Brewing Company (23 beers) ranked list of the top 10 beers, top 10 breweries, and top 10 Sierra Nevada Brewing Company most diverse breweries." Ken Grossman and Paul Camusi started the Sierra Nevada The Boston Beer Company also competes with the Brewing Company in 1980. It is the second largest craft noncraft breweries that sell premium imports and standard brewery behind the Boston Beer Company and the 10th and economy lagers. In regards to dollar sales, a list of the largest brewery in the United States. It was also voted top 20 beers in the United States is shown in Exhibit 6, the best craft brewery by the Homebrewers Association followed by a list of the top imports in Exhibit 7. Samuel Sierra Nevada makes a pale ale that is the highest-selling Adams did not crack the top 20 list." pale ale in the country. The company sold approximately EXHIBIT 6 Top Dollar Sales of Beers in the United States B C D 1 Top Dollar Sales of Beers in the United States Go to library tab in 2 Rank Beer Dollar Sales Brewery Connect to access 3 1 Bud Light $5,327,145,000 Anheuser-Busch Inbey Case Financials. 4 2 Budweiser $2.072 380.000 Anheuser-Busch Inbev 5 3 Coors Light $1,946,762,000 Miller Coors 6 6 4 Miller Lite $1,672,598,000 Miller Coors 7 5 Natural Light $1.089,709,000 Anheuser-Busch Inbey 8 6 Corona Extra $ 964,968,900 Crown Imports 9 9 7 Busch Light $ 735,397,100 Anheuser-Busch Inbev 10 8 Busch $ 684,469,700 Anheuser-Busch Inbev 11 9 Heineken $ 577,453,300 Heineken USA 12 10 Michelob Ultra Light $518,075.100 Anheuser-Busch Inbev 13 11 Miller High Life $ 498,743,900 Miller Ccors 14 12 Keystone Light $ 484,396.900 Miller Coors 15 13 Natural Ice $363, 154,400 Anheuser-Busch Inbev 16 14 Modelo Especial $ 331,697,700 Crown Imports 17 15 Bud Light Lime $ 299,320,300 Anheuser-Busch Inbev 18 16 Icehouse $ 239,119,900 Miller Coors 19 17 Bud Ice $ 221,357,000 Anheuser-Busch Inbev 20 18 Pabst Blue Ribbon $ 204,409,400 Pabst Brewing Company 21 19 Yuengling Lager $ 185,332,400 Yuengling Brewery 22 20 Corona Light $ 168,556,600 Crown Imports EXHIBIT 7 Top Dollar Sales of Imported Beers in the United States (millions of dollars) B C Top Dollar Sales of Imported Beers in the 1 Go to United States (milions of dollars) 2 Beer library beer Sales 1 tab in Corona Extra $422.90 4 2 Connect Heineken $275.40 5 to access 3 Corona Light $129.10 6 4 Tecate Case $ 95.90 7 5 Financials. . Modelo Especial $ 90.50 8 6 5 Stella Artois Lager $67.80 9 7. Heineken Premium Light Lager $ 58.30 10 B Dos Equis XOC Lager Especial $ 56.40 $ 11 9 Newcastle Brown Ale $ 56.20 12 10 Guinness Draught $ 47.20 13. 11 Beck's $ 45.00 14 12 Pacifico $ $42.70 15 15 13 13 Labatt Blue $ 42.10 16 14 Labatt Blue Light $S3.40 17 17 15 Amstel Light $ 30.20 18 se 16 Foster's Lager $ 27.30 19 17 $ 24.80 20 18 Negra Modelo $ 22.40 21 19 Dos Equis XX Ambar Lager $ 20.40 22 20 St. Paull Girl $ 19.90 Rad Stripe 865.000 barrels of beer in 2012 and distributes in all Heineken imports popular brands such as Heineken. 50 states. Sierra Nevada was one of the earliest craft Amstel Light, SolDos Equis, and Newcastle. The breweries, and its founders are consequently referred to as Heineken beer alone cellected more than $590 million in to open another brewing facility within the next few years it has the ability to advertise its products nationally. The by promoting the craft beer industry and by their efforts popular "Most Interesting Man in the World" commercials to be environmentally friendly in their beer's production began airing. Most of the brands offered by Heineken are One of Sierra Nevada Brewing's goals is to overtake the in the price range of Samuel Adanus, making them a close Boston Beer Company as the largest craft brewery in the competito." Anheuser-Busch Inbev NV New Belgium Brewing Company Anheuser-Busch Inbev is one of the largest beer compa Jeff Lebesch founded New Belgium Brewing Company nies in the world, with roughly $40 billion in revenue in in Fort Collins, Colorado 1991. New Belgium Brew- 2012. The brewing portion of the company remains the ing Company is the third largest craft brewery in the largest brewery in the country and has an an approximate United States behind the Boston Beer Company and Sierra 50 percent stake in the United States beer industry. They Nevada, and the 8th largest brewery in the country. The have the two best-selling beers in the country with Bud company's flagship beer is an amber ale called Fat Tire, Light and Budweiser and the fifth best-selling beer with is over 25 different s in production. In 2012 the Natural 1 Light. However, they have seen the sale of their company sold over 700,000 barrels of beer and was dis- products decline over the last several years. In an effort tributed in 29 states. Over the last several years, the com to combat the lower volume of sales, they have raised the pany has seen growth of approximately 15 percent. New prices of their ber. North Carolina by 2015 to compete with the other major explosive growth of the craft beer industry. Although it Additionally, the company has also been witness to the breweries. Like Sierra Nevada, New Belgium focuses on could never be considered a craft brewery because of its energy-efficient practices. New Belgium Brewing also size, Anheuser-Busch plans to make more craftlike beers, hopes to become the largest craft brewery in the country." as it has done with its brand Shock Top. They also plan Avg. Price for a 6 Package of Beer $4.99 Market Share 0.198 0.097 0.074 $4.99 $4.99 EXHIBIT 8 Map of Domeslic Beer Brands Domestic Beers Alcohol by volume (%) Bud Light 4.20 Coors Light 4.20 Budweiser 5.00 Miller Light 4.20 Corona Extra 4.60 Natural Light 4.20 Busch Light 4.10 Busch 4.60 $499 0.041 $7.99 0.035 $3.49 0.035 $399 0.032 $149 0.029 4.70 $399 0.024 4.13 $3.49 0.022 Miller High Lite Keystone Light Blue Moon Belgian White Heineken 5.36 $8.49 0.015 5.00 $5.99 0.010 4.90 $8.49 0.019 5.20 $8.49 0.008 5.60 $8.49 0.008 Samuel Adams Boston Lager Shock Top Belgian White Sierra Nevada Pale Ale New Belgium Fat Tire Yuenging Lager Dogfish Head Pale Alo Brookyn Brewery Lager 5.20 $8.99 0.007 4.40 $8.49 0.005 0.004 5.00 $9.99 5.20 $7.99 0.004 to invest in and purchase small craft weweries, like that Belgian White. They have also started the group Teach of Goose Island, which makes the popular beer 312. The and Blake to focus on the craft beer industry and premium company is also not opposed to merging with other large imports and plan to expand the group by 60 percent over breweries. In June of 2012, the company was partaking in the next few years. Some of their other premium beers talks with the maker of Corona to purchase the company include Leinenkugel's Honey Weiss, George Killian's Irish The size and influence that Anheuser-Busch has pose a Red, Batch 19, Henry Weinbard's IPA, Colorado Native, threat to the Boston Beer Company because their substan Pilsner Urquell, Peroni Nastro Azzuro, and Grolsch." tial lead in available capital. Thinking about the Future for Beer Millercoors, LLC The Boston Beer Company created high-quality craft MillerCoors, LLC, is the second largest brewing com- beers and sold them at a higher prices than standard and pany in the country, a joint venture between the Miller and economiy lagers. It was the largest craft brewery in the Coors brands, accounting for approximately 30 percent country and the seventh largest overall brewery. While of the market. They have two out of the top five most Boston Bear was delighted to be the largest craft brewery, popular beers with Miller Lite and Coors Light and would the goal was to become the third largest overall brewery like to catch up with Anheuser-Busch Inbev. The company in the country. Brand recognition is key to any business, trades publicly as Molson Coors Brewing Company and and it is especially obvious in the beer industry. Anheuser- SAB Miller, CASES CASE 20 THE BOSTON BEER COMPANY* The Boston Beer Company, known for its Samuel Adams more of the market. As the country's largest craft brew- brand, is the largest craft brewery in the United States, ery, the Boston Beer Company had revenue of over $500 holding a 1 percent stake in the overall beer market.' million in 2011 and sold over 2 million barrels of beer. faces growing competitive threats from other breweries. Other large craft breweries include New Belgium Brewing both large and small. In the past several years, the beer Company and Sierra Nevada Brewing Company, which industry as a whole has been on a decline, while sales of sold over 580,000 and 720,000 barrels of beer in 2011, wines and spirits have increased. The Boston Beer Com respectively. In addition, some smaller breweries have pany competes within the premium beer industry, which been merging to take advantage of economies of scale and includes craft beer and premium imported beers like enhance their competitive position. Heineken and Corona. Although the beer industry has been According to Boston Beer Company, there are on a decline, the premium beer industry has seen a small approximately 770 craft breweries that ship their prod- amount of growth, and the craft beer industry has seen a wet domestically, up from 420 in 2006. There are also an surge in popularity. Because of this success of the craft expected 800 craft breweries in the planning stage, expect- breweries in particular the major breweries have taken ing to be operational within the next 2-3 years. Boston notice and many new craft breweries have sprung up. Beer Company assumes that 300 of those 800 will be Anheuser-Busch Inbev and MillerCoors, LLC, account shipping breweries (ie, breweries that sell their prod- for over 80 percent of the beer market in the United uct beyond their local market). Thus, within the next few States. They have caught on to the current trend Andy Glede Samuel Adams beer may be competing with over beer industry toward higher quality beers and have started 1,000 other craft breweries around the country releasing their own higher quality beers. For example, The Boston Beer Company competes not only with Anheuser-Busch Inbev has released Bud Light Wheat and domestic craft breweries but also with premium beer Bud Light Platinum in an effort to provide quality beers to imports, such as Heineken and Corona, which sell beer their loyal customers. MillerCoors makes Blue Moon beer, in a similar price range, Like Anheuser-Busch Inbev and which is the most popular craft beer in the United States. MillerCoors, Heineken and Corona have large financial Anheuser-Busch Inbev released Shock Top to combat the resources and can influence the market. It is projected that popularity of Blue Moon. These companies have also premium imported beers will grow by 6 percent over the begun to purchase smaller craft breweries, whose products next five years, have been rising in popularity. Anheuser-Busch Inbev pur The Brewers Association defines a craft brewery as chased Goose Island Brewing Company in March 2011. brewing less than six million barrels per year and being less MillerCoors has started a group within the company titled than 25 percent owned or controlled by another economic Tenth and Blake Beer Company for the purpose of creating interest. Maintaining status as a craft brewery can be impor- and purchasing craft breweries. According to MillerCoors tant for image and therefore, sales. Thus, MillerCoors CEO Tom Lang, the plan is to grow Tenth and Blake Beer purchased less than a 25 percent stake in Terrapin Beer, still Company by 60 percent within the next three years. The allowing it to maintain its craft brewery status. The size of two major companies plan to use their massive marketing the Boston Beer Company, however, is an issue. With con- budgets to tell people about their craft beers. tinued growth, the brewery could potentially increase its According to the Brewers Association, 1.940 craft volume output to more than 6 million barrels per year, thus breweries and 1,989 total breweries operated in the losing its craft brewery status. Furthermore, with the size United States for some or all of 2011. While craft brewer of the company and their ability to market nationwide, the jes account for over 97 percent of all the breweries in the company runs the risk of alienating itself from other craft United States, they only produce approximately 25 percent breweries who believe Samuel Adams no longer fits the of all beer sold. However, with the rise in popularity of profile. Many craft breweries already believe the company, premium beers, the craft breweries will continue to grab which has been public since 1995, is more concerned with making money than with providing quality beer and edu- This case was developed by graduate students Peter J. Courtney and Eric S. cating the public on craft beers. Engelson and Professor Ahn B. Eisner Pace University, Material has been Size does have advantages, of course, with more money drawn from published sources to be used for dass discussie. Copyright for marketing and, especially in the beer business, with 2013 Alan B. Eister distribution. A heavy complaint for all craft breweries is C128 CASE 20 : THE BOSTON BEER COMPANY the difficulty they have distributing their product in the at two different prices, $15 to loyal customers and $20 ument three-tier system (discussed in a later section). The through an IPO run by Goldman Sachs. Koch decided large breweries have power over the independent distribu- to reward his loyal customers by advertising the stock tors because they account for most of their business. Thus, offering on the packages of his six-packs, estimating that they can influence the distributors and make it difficult for 30,000 buyers would be interested. He believed that those craft breweries to sell their product. Because of its size, who enjoyed the beer and supported it should be the ones the Boston Beer Company has fewer problems with dis- who have a stake in the company. After 100,000 potential tributors than its smaller competitors do. Consequently, the investors sent checks in, Koch randomly chose 30,000. company has less in common with other craft breweries Managers from Goldman Sachs were upset that they did and more with the major breweries in regards to distribu- not receive the lowest-price offering. Koch owns 100 per- tion. This is good for Boston Beer Company's distribution, cent of Class B Common stock, of which all major deci- but might be bad for its image. One brewer from The Defi-sions for the company are made. This is seen as a risk ant Brewing Company in Pearl River, New York, said that to potential investors because Koch can make important The Boston Beer Company was becoming too large to be decisions on the strategy for the company without receiv- considered a call brewery and that their substantial con ing approval nections with distributors contributed to this notion. Continued success for the business led to the purchase As the above discussion makes clear, The Boston Beer of a large brewery in Cincinnati in 1997. Since 2000, Company is facing a difficult competitive environment. Samuel Adams has won more awards in international beer They are facing direct competition from both larger and tasting competitions than any other brewery in the world. snaller breweries and from premium imported beers. In 2008 the Boston Beer Company purchased a world- Some of the smaller craft breweries are growing quickly class brewery in Lehigh, Pennsylvania, to support growth and want to be larger than the Boston Beer Company As of 2013, the Boston Beer Company was the larg. Other craft breweries feel that the Boston Beer Company est craft brewery in the United States, brewing over two is too large already. Thus, while further growth would be million barrels of Samuel Adams beer, but still only made beneficial in terms of revenue, growing too large could up approximately 1 percent of the total U.S. beer market. negatively affect the company's status as a craft brewery The company has expanded its selections to over 50 beer and the perceptions of its customers. The company must flavors, including seasonal and other flavorful beers, such pay close attention to maintaining its image for the grow as Samuel Adams Summer Ale, Samuel Adams Cherry ing customer base of premium beer drinkers. Wheat, and Samnuel Adams Octoberfest, as well as the non-beer brands Twisted Tea and HardCore Cider. The Boston Company Background Beer Company planned to use the profits gained from its Jim Koch started the Boston Beer Company in 1984 along non-beer brands to invest in Samuel Adams and build a with fellow Harvard MBA graduates Harry Rubin and stronger portfolio. Revenue for the company grew from Lorenzo Lamadrid. The company began with the sale of $380 million in 2007 to over $500 million in 2011, while the now popular Samuel Adams Boston Lager, named operating costs grew from $150 million to $180 million after the famous American patriot who was known to have Net income tripled from $22 million to $66 million in the been a brewer himself. The recipe for the lager was passed same period (see Exhibits 1 and 2). In July 2012, the com- ing back to the 1860s. Koch began home brewing the beach pany was selling at $113, nearly $100 over the initial pub- lic offering from 1995. in his own kitchen and soliciting local establishments in The goal of the Boston Beer Company was to become Boston to purchase and sell it. Just one year after its initial the leading brewer in the premium beer market. As of sales, Samuel Adams Boston Lager was voted "Best Beer 2013, it was the largest craft brewery, but it trailed Crown in America" at the Great American Beer Festival in Den- Imports, LLC, and Heineken USA in the premium beer ver, Colorado. In 1985 Samuel Adams grew immensely market. The company planned to surpass the large import- and sold 500 barrels of beer in Massachusetts, Connecti-ers by increasing brand availability and awareness through cut, and West Germany." advertising, drinker education, and the support of its over To avoid the high up-front capital costs of starting a 300-member salesforce. The salespeople for the company brewery, Koch contracted with several existing brewer- have a high level of product knowledge about beer and the ies to make his beer. This allowed the production of the brewing process and use this to educate distributors and the Boston Lager to grow quickly from the relatively small public on the benefits of Samuel Adams. In 2011 the Bos- quantities Koch could brew himself. Growth continued ton Beer Company formed a subsidiary called Alchemy after that, and in 1988 the Boston Beer Company opened & Science to seize new opportunities in the craft brew-a brewery in Boston. By 1989 the Boston Beer Companying industry. The purpose of this group will be to iden- produced 63,000 barrels of Samuel Adams beer annually. tify better beer ingredients, methods for better brewing, The company went public in 1995, selling Class A and purchasing opportunities for any breweries that would Common stock to potential investors. The stock was sold help the business grow. One of these instances instances occurred in EXHIBIT 1 Income Statements A Income Statements Gatobrary Carreto som Case France Dec 21, 2012 580 222 265.012 315510 Dec 30, 2011 Dec 24, 2010 513,000 463,786 228,453 207,471 284,567 25.12 3 Period Ending 4 Total Revenue 5 Castor 6 Gross Pro 7 Operating Expenses 8 Saling General and Art 9 Nang 10 Operating income or on 11 comme on Continuing Operations 12 Total transport 13 Earrings Before does 14 come forex 15 Toome Tax Expense 18 Nelone Pro Carthurgas 17 Retinama 21947 119 $6,584 180.246 666 105,055 174.349 300 81,178 $6517 96.517 56,060 59.407 5447 103,500 103,500 37.441 66,050 66,059 (1991 21,106 81,906 30.966 50.143 50.142 All in Serce Bo Beer Copy EXHIBIT 2 Balance Sheets c C Ballince Sheets Gatoibrary Contacto Case Financials Dec 21, 2012 Dec 30, 2011 Dec 24, 2010 74.363 36.990 4431 6,028 162,342 189MB 49.450 27576 34072 14.603 125.722 149.586 1377 1802 272,488 48.000 23.03 28,514 12,750 112.104 142.829 187 2260 2585 2009 4055 359,414 3 Periodinding 4 5 Current Assets 6 Cash And Cash Equivalents 7 Net Recals 8 livery 9 Other Content Assets 10 Total Quran Assets 11 Property Plant and Equipment 12 Goodwill 1. CHI MINH 14 Total Assets 15 Listites 16 Current Us 17 Accounts Payable 1B Shop Cantom Tom Dot 19 Total Current Liabilities 20 Long Term Dot 21 Charlantes 22 Deleted Long Term Charges 28 Total Lubis 24 Sledilders' Equity 25 Cannon Stock 26 Retained Emings 27 Capital Saplus 20 Other Stadtquly 29 Total Stockholde Equity 30 let Tangible esats 39,132 67,049 72,199 68,194 67049 72.199 4471 20,413 114 9,345 17.340 87.743 3.656 17.00 92.062 128 47.119 133 336 29541 157,305 X 245.1991 242,553 136 43576 22.016 (438 155.588 164,211 184,745 183.358 All abers in the Sou Boe Boer Compay C130 CASE 20THE BOSTON BEER COMPANY early 2012, when the group purchased Southern California market. MillerCoors also had a large share of the market Brewing, at just over 30 percent. Together these two companies sold The company continues to invest in efficiency initiatives approximately 8 out of every 10 beers purchased in the to lower cost within its breweries and increase margins. One United States. The third largest brewer in terms of volume large program that the company is employing is its Fresh- of beer sold was the Mexican-owned Crown Imports LLC est Beer Program. Typically, bottled and canned bear sits which accounted for less than 6 percent of the market. As in a distributor's warehouse for three to five weeks, while the seventh largest brewery in the country, the Boston Beer kegs sit for three to four weeks. In an effort to reduce stor Company had a 1.1 percent share of the market. age time in the distributor warehouses approximately two weeks and consequently increase freshness of the beer Changes in Drinking Habits in retailers, the company focused on better on-time service. The consumption habits of beer drinkers appear to have forecasting, production planning, and great coordination changed in recent years. From 2006 to 2011, the beer indus- and cooperation with distributors. In 2011 the company try as a whole declined by approximately 3 percent." This had 50 percent of its beer on the Freshest Beer Program, was mostly due to the decline in the consumption of stan with the goal of expanding that number to 75 percent in dard lager by 10 percent and economy lager by 3 percent. 2012 by investing $50 million into the program. Even though the volume of beer sold declined, the craft While expansion and growth are more commonly brew market had in fact exploded. Within the same period, deemed positive attributes, Boston Beer Co is aware dark ales grew by 67 percent and premium Ingers grew by of the many possible risks in the growth of its business. 27 percent. Wheat beers (a segment of dark ales) expe- With the acquisition of the Lehigh brewery in 2008, the rienced an especially large growth of over 150 percent. Boston Beer Company now brews over 90 percent of its The Boston Beer Company lwewed the Samuel Adams beer from its own breweries. With capital tied up in large Cherry Wheat beer in this category, which was one of the investments, there was a potential for the business to falter company's popular beers. According to Euromonitor Inter- if an unexpected event affected one of the breweries and national, projected beer volume sales would decline by halted production at that facility. The company had also percent during 2013 to 2017, but craft beers were pro- put forth a sizable investment to increase product offer-jected to grow by 3 percent. As shown in Exhibit 3, dark ings and another to keep its beer/i81. during distribuitou beers, low-alchol beers, and domestic premium lagers However, with its reliance on independent distributors, a were the only beer categories to grow from 2007-2011. mishap in its relationship with major distributors could tend to complications within their supply chain. The Bos- The Three- Tier System ton Beer Company also depended on foreign suppliers of raw material ingredients for its beer. An unexpected short. In 2011, 75 percent of the volume of beer was sold at off-age of a crop might lead to a drop in production Volume trade value in supermarkets, beer distributors, and such. In effect, the image of the company would diminish if its while the other 25 percent was sold in bars and restau- products were not available to loyal fans whose enjoyment rants. Despite the vast difference in volume sold, the value of the brand relies on the wide accessibility of a craft beer. of beer sold for both off-trade and on-trade were equal With the surge of an enormous number of other craft beer because of the premium charged for purchasing beer at a choices, customers had many options to choose from. bar or a restaurant Breweries are not permitted to own either off-trade or on-trade establishments, so their beer has to be distributed Industry Before prohibition however, beer was sold in tavernlike Although Samuel Adams was sold in other countries, the establishments called "tied houses," which supplied and United States was where the majority of the product was sold their own beer. There were no regulations regarding sold and where they held the most prominence in the beer brewing companies owning all of the retail "tied houses market. Within the beer industry, Samuel Adams fell into and only selling their own beer. After prohibition, a sys. the craft beer category. In terms of volume of beer sold. tem was put in place to discourage monopolies in the sup- the Boston Beer Company was the largest craft brewery ply and sale of beer. This system was titled the Three-Tier in the country, but only the seventh largest brewery overall System are divided the beer industry into suppliers, dis in 2013. The beer market consists mainly of standard and tributors, and retailers, all independent of each other. Aside economy lagers, which account for nearly 75 percent of all from the brewpub, breweries cannot own retailers or dis- volume sold. Samuel Adams brand beers were more costly tributors, thus ensuring a level of competition in the brew than standard lagers, and were counted with the premiun ing industry." beers, which together account for the other 25 percent of Although the three categories of the industry are sepa- all beer sold. rate, they each bave a large influence on one another. For In 2011 there were over 200 million barrels of boer instance, Anheuser-Busch Inbev and MillerCoors sell sold in the United States. Anheuser-Busch Inbev domi 80 percent of the beers in the country. That means that nated the beer industry, totaling over 48 percent of the 80 percent of distributors' volume, and consequently EXHIBIT 3 Total Sales of Beer, 2007-2012 (Millions of Barrels) F G Go to library tab in Connect to access Case Financials. 1 2 Type of Beer 3 Amber Ale 4 Other Ale 4 5 Pale Al: 6 Wheat Beer 7 Other Dark Bear 8 Subtotal Dark Beers 9 Domestic Premium Lager 10 Imported Premium Lager 11 Standard Lager 12 Economy Lager 13 Subtotal Lagers 14 Low Alcohol Beer 15 Stout 16 Total B D Total Sales of Beer, 2007-2012 Millions of Barrels) , 2007 2008 2009 2010 0.78 081 097 1.10 1.57 1.60 1.63 1.78 1.32 1.35 137 1.51 1.69 1.96 2.26 297 0.08 0.08 0.08 0.08 5.45 5.80 6.32 7.44 13.76 15.55 15.74 15.20 27.29 26.75 25.04 25.40 110.28 109.71 105.37 100.11 50.88 51.68 52.66 51.43 202.22 203.69 198,81 192.34 1.06 1.08 1.93 2.73 1.15 1.16 1.14 1.16 209.88 211.72 208.20 203.67 2011 1.11 194 1.79 3.30 0.08 8.17 15.58 25.71 98.07 48 88 188.21 2.57 1.27 200.21 2012 1.12 2.09 1.86 3.70 0.08 8.85 15.76 26.03 95,60 44.40 181.79 241 1.35 194.40 revenue, is from these two companies. Hence, the dis- professional breweries as well as home brewers. In 2012 tributors value the business of Anheuser-Busch Inbev and more than 1,650 beers in 65 different categories were sub- MillerCoors to a higher degree, in fear of losing their busi- mitted. The top 10 brewers were named based on receiving ness. In an effort to maintain its dominant position in the the highest overall grade in the most categories collec- industry, Anheuser-Busch Inbev has contracted with ser- tively. Exhibit 4 shows the top 10 brewers for 2012 accord- eral distributors on the condition that they cannot working to the U.S. Open Beer Championship. The Boston Beer with any other breweries. Likewise, the other large brewer Company received the second-place ribbon, an impressive jes impose restrictions on their distributors on what other feat with so many breweries participating? breweries they can work with as well. Home brewing has become an extremely popular hobby The distributors act as the intermediary in the beer and in many instances has led home brewers to pursue their industry, providing the beer to retailers. The beer that is passion in the form of an actual brewery. The Homebrew- available from retailers is a result of the products that their ers Association was founded in 1978 and includes more distributors carry. The distributors are major decision mak- than 30,000 beer-enthusiastic members. Location EXHIBIT 4 Top 10 Brewers, U.S. Open Beer Championship, 2012 Rank Brewery 1 Sweetwater Brewing 2 Boston Beer Company 3 Deschutes Brewery Georgia Massachusetts Oregon 4 Florida 5 Wyoming 6 Ontario 7 Cigar City Brewing Black Tooth Brewing Niagara College Full Sail Brewing Sprecher Brewing Morgan Street Brewing Maui Brewing Oregon 8 Wisconsin 9 Missouri 10 Hawaii Best Portfolio EXHIBIT 5 Top 10 Beer Categories in 2012 Best Beer Best Brewery Russian River Pliny the Elder Sierra Nevada Brewing Company Bell's Two Hearted Ale Dogfish Head Craft Brewery Dogfish Head 90 Minute IPA Stone Brewing Company Sierra Nevada Pale Ale Russian River Brewing Company Stone Arrogant Bastard Ale Bell's Brewery Bell's Hopslam New Belgium Brewing Company Sierra Nevada Celebration Firestone Walker Brewing Company Stone Ruination IPA Deschutes Brewery Sierra Nevada Torpedo Lagunitas Brewing Company North Coast Old Rasputin Founders Brewing Company Samuel Adams Boston Lager (31st) Boston Beer Company (11th) Boston Beer Company (41 beers) Dogfish Head Craft Brewery (34 beers) New Glarus Brewing Company (28 beers) Rogue Ales (27 beers) Bell's Brewery (26 beers) New Belgium Brewing Company (26 beers) Sierra Nevada Brewing Company (25 beers) Three Floyds Brewing Company 25 beers) Goose Island Brewing Company (23 beers) Great Divide Brewing Company (23 beers) ranked list of the top 10 beers, top 10 breweries, and top 10 Sierra Nevada Brewing Company most diverse breweries." Ken Grossman and Paul Camusi started the Sierra Nevada The Boston Beer Company also competes with the Brewing Company in 1980. It is the second largest craft noncraft breweries that sell premium imports and standard brewery behind the Boston Beer Company and the 10th and economy lagers. In regards to dollar sales, a list of the largest brewery in the United States. It was also voted top 20 beers in the United States is shown in Exhibit 6, the best craft brewery by the Homebrewers Association followed by a list of the top imports in Exhibit 7. Samuel Sierra Nevada makes a pale ale that is the highest-selling Adams did not crack the top 20 list." pale ale in the country. The company sold approximately EXHIBIT 6 Top Dollar Sales of Beers in the United States B C D 1 Top Dollar Sales of Beers in the United States Go to library tab in 2 Rank Beer Dollar Sales Brewery Connect to access 3 1 Bud Light $5,327,145,000 Anheuser-Busch Inbey Case Financials. 4 2 Budweiser $2.072 380.000 Anheuser-Busch Inbev 5 3 Coors Light $1,946,762,000 Miller Coors 6 6 4 Miller Lite $1,672,598,000 Miller Coors 7 5 Natural Light $1.089,709,000 Anheuser-Busch Inbey 8 6 Corona Extra $ 964,968,900 Crown Imports 9 9 7 Busch Light $ 735,397,100 Anheuser-Busch Inbev 10 8 Busch $ 684,469,700 Anheuser-Busch Inbev 11 9 Heineken $ 577,453,300 Heineken USA 12 10 Michelob Ultra Light $518,075.100 Anheuser-Busch Inbev 13 11 Miller High Life $ 498,743,900 Miller Ccors 14 12 Keystone Light $ 484,396.900 Miller Coors 15 13 Natural Ice $363, 154,400 Anheuser-Busch Inbev 16 14 Modelo Especial $ 331,697,700 Crown Imports 17 15 Bud Light Lime $ 299,320,300 Anheuser-Busch Inbev 18 16 Icehouse $ 239,119,900 Miller Coors 19 17 Bud Ice $ 221,357,000 Anheuser-Busch Inbev 20 18 Pabst Blue Ribbon $ 204,409,400 Pabst Brewing Company 21 19 Yuengling Lager $ 185,332,400 Yuengling Brewery 22 20 Corona Light $ 168,556,600 Crown Imports EXHIBIT 7 Top Dollar Sales of Imported Beers in the United States (millions of dollars) B C Top Dollar Sales of Imported Beers in the 1 Go to United States (milions of dollars) 2 Beer library beer Sales 1 tab in Corona Extra $422.90 4 2 Connect Heineken $275.40 5 to access 3 Corona Light $129.10 6 4 Tecate Case $ 95.90 7 5 Financials. . Modelo Especial $ 90.50 8 6 5 Stella Artois Lager $67.80 9 7. Heineken Premium Light Lager $ 58.30 10 B Dos Equis XOC Lager Especial $ 56.40 $ 11 9 Newcastle Brown Ale $ 56.20 12 10 Guinness Draught $ 47.20 13. 11 Beck's $ 45.00 14 12 Pacifico $ $42.70 15 15 13 13 Labatt Blue $ 42.10 16 14 Labatt Blue Light $S3.40 17 17 15 Amstel Light $ 30.20 18 se 16 Foster's Lager $ 27.30 19 17 $ 24.80 20 18 Negra Modelo $ 22.40 21 19 Dos Equis XX Ambar Lager $ 20.40 22 20 St. Paull Girl $ 19.90 Rad Stripe 865.000 barrels of beer in 2012 and distributes in all Heineken imports popular brands such as Heineken. 50 states. Sierra Nevada was one of the earliest craft Amstel Light, SolDos Equis, and Newcastle. The breweries, and its founders are consequently referred to as Heineken beer alone cellected more than $590 million in to open another brewing facility within the next few years it has the ability to advertise its products nationally. The by promoting the craft beer industry and by their efforts popular "Most Interesting Man in the World" commercials to be environmentally friendly in their beer's production began airing. Most of the brands offered by Heineken are One of Sierra Nevada Brewing's goals is to overtake the in the price range of Samuel Adanus, making them a close Boston Beer Company as the largest craft brewery in the competito." Anheuser-Busch Inbev NV New Belgium Brewing Company Anheuser-Busch Inbev is one of the largest beer compa Jeff Lebesch founded New Belgium Brewing Company nies in the world, with roughly $40 billion in revenue in in Fort Collins, Colorado 1991. New Belgium Brew- 2012. The brewing portion of the company remains the ing Company is the third largest craft brewery in the largest brewery in the country and has an an approximate United States behind the Boston Beer Company and Sierra 50 percent stake in the United States beer industry. They Nevada, and the 8th largest brewery in the country. The have the two best-selling beers in the country with Bud company's flagship beer is an amber ale called Fat Tire, Light and Budweiser and the fifth best-selling beer with is over 25 different s in production. In 2012 the Natural 1 Light. However, they have seen the sale of their company sold over 700,000 barrels of beer and was dis- products decline over the last several years. In an effort tributed in 29 states. Over the last several years, the com to combat the lower volume of sales, they have raised the pany has seen growth of approximately 15 percent. New prices of their ber. North Carolina by 2015 to compete with the other major explosive growth of the craft beer industry. Although it Additionally, the company has also been witness to the breweries. Like Sierra Nevada, New Belgium focuses on could never be considered a craft brewery because of its energy-efficient practices. New Belgium Brewing also size, Anheuser-Busch plans to make more craftlike beers, hopes to become the largest craft brewery in the country." as it has done with its brand Shock Top. They also plan Avg. Price for a 6 Package of Beer $4.99 Market Share 0.198 0.097 0.074 $4.99 $4.99 EXHIBIT 8 Map of Domeslic Beer Brands Domestic Beers Alcohol by volume (%) Bud Light 4.20 Coors Light 4.20 Budweiser 5.00 Miller Light 4.20 Corona Extra 4.60 Natural Light 4.20 Busch Light 4.10 Busch 4.60 $499 0.041 $7.99 0.035 $3.49 0.035 $399 0.032 $149 0.029 4.70 $399 0.024 4.13 $3.49 0.022 Miller High Lite Keystone Light Blue Moon Belgian White Heineken 5.36 $8.49 0.015 5.00 $5.99 0.010 4.90 $8.49 0.019 5.20 $8.49 0.008 5.60 $8.49 0.008 Samuel Adams Boston Lager Shock Top Belgian White Sierra Nevada Pale Ale New Belgium Fat Tire Yuenging Lager Dogfish Head Pale Alo Brookyn Brewery Lager 5.20 $8.99 0.007 4.40 $8.49 0.005 0.004 5.00 $9.99 5.20 $7.99 0.004 to invest in and purchase small craft weweries, like that Belgian White. They have also started the group Teach of Goose Island, which makes the popular beer 312. The and Blake to focus on the craft beer industry and premium company is also not opposed to merging with other large imports and plan to expand the group by 60 percent over breweries. In June of 2012, the company was partaking in the next few years. Some of their other premium beers talks with the maker of Corona to purchase the company include Leinenkugel's Honey Weiss, George Killian's Irish The size and influence that Anheuser-Busch has pose a Red, Batch 19, Henry Weinbard's IPA, Colorado Native, threat to the Boston Beer Company because their substan Pilsner Urquell, Peroni Nastro Azzuro, and Grolsch." tial lead in available capital. Thinking about the Future for Beer Millercoors, LLC The Boston Beer Company created high-quality craft MillerCoors, LLC, is the second largest brewing com- beers and sold them at a higher prices than standard and pany in the country, a joint venture between the Miller and economiy lagers. It was the largest craft brewery in the Coors brands, accounting for approximately 30 percent country and the seventh largest overall brewery. While of the market. They have two out of the top five most Boston Bear was delighted to be the largest craft brewery, popular beers with Miller Lite and Coors Light and would the goal was to become the third largest overall brewery like to catch up with Anheuser-Busch Inbev. The company in the country. Brand recognition is key to any business, trades publicly as Molson Coors Brewing Company and and it is especially obvious in the beer industry. Anheuser- SAB Miller