Answered step by step

Verified Expert Solution

Question

1 Approved Answer

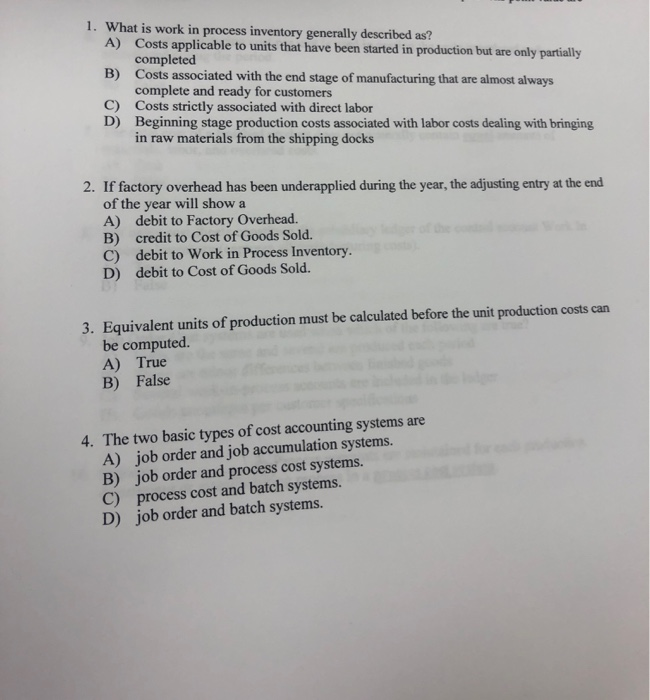

1. What is work in process inventory generally described as? A) B) C) Costs applicable to units that have been started in production but are

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Internal Audit As Change Agent The Activation And Successful Implementation Of Organizational Change

Authors: Peter Kundinger

3rd Edition

3751984070, 978-3751984072