Answered step by step

Verified Expert Solution

Question

1 Approved Answer

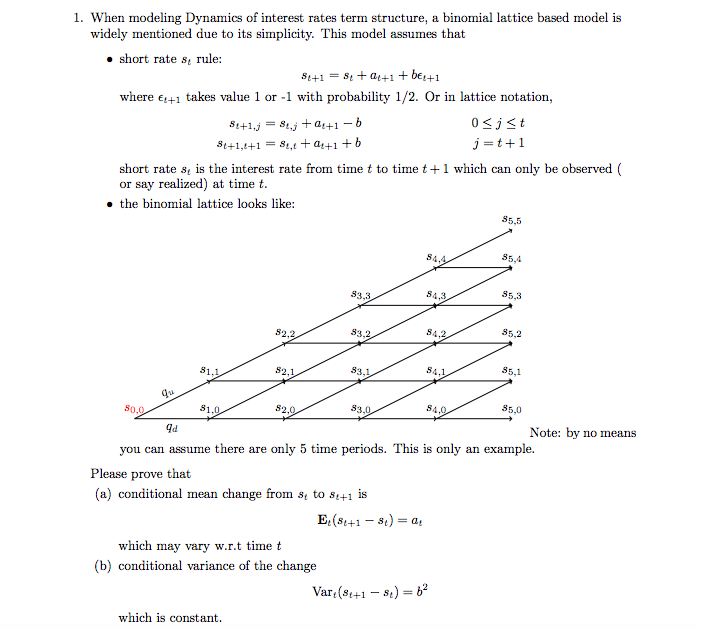

1. When modeling Dynamics of interest rates term structure, a binomial lattice based model is widely mentioned due to its simplicity. This model assumes

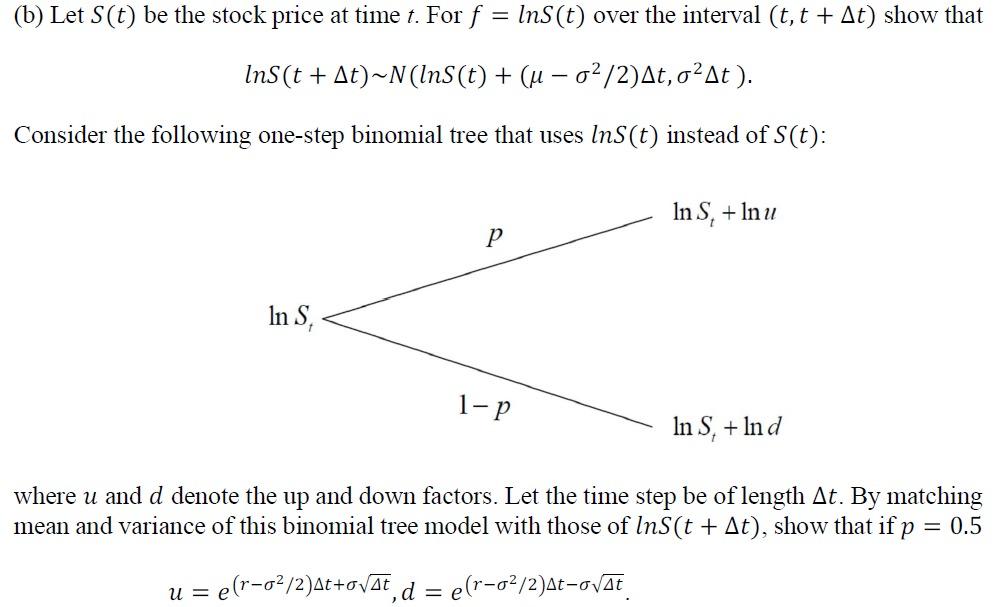

1. When modeling Dynamics of interest rates term structure, a binomial lattice based model is widely mentioned due to its simplicity. This model assumes that short rate s, rule: Se+1=8e+at+1+Bee+1 where +1 takes value 1 or -1 with probability 1/2. Or in lattice notation, 8t+1,j St+1,1+1 =8,t+a+1+b 0 j t j=t+1 short rates, is the interest rate from time t to time t+1 which can only be observed ( or say realized) at time t. the binomial lattice looks like: 85,5 85,4 844 85,3 84,3 83,3 85,2 84.2 83.2 82.2 85,1 84.1 83,1 82.1 81,1 85,0 84.0 qu 83.0 $2,0 80,0 qd you can assume there are only 5 time periods. This is only an example. Please prove that (a) conditional mean change from s to s+1 is Note: by no means which may vary w.r.t time t (b) conditional variance of the change which is constant. Et (8+1-8) a = Var(8+1 st) 62 - = (b) Let s(t) be the stock price at time t. For f = lns (t) over the interval (t,t + At) show that InS(t + At)~N (InS(t) + ( o/2) At, o At). Consider the following one-step binomial tree that uses Ins(t) instead of s(t): P In S, 1-P In S, + Inu In S,+Ind where u and d denote the up and down factors. Let the time step be of length At. By matching mean and variance of this binomial tree model with those of InS(t + At), show that if p = 0.5 u = e(r-o/2)At+od = e e(r-02/2)At-oAt

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657