Answered step by step

Verified Expert Solution

Question

1 Approved Answer

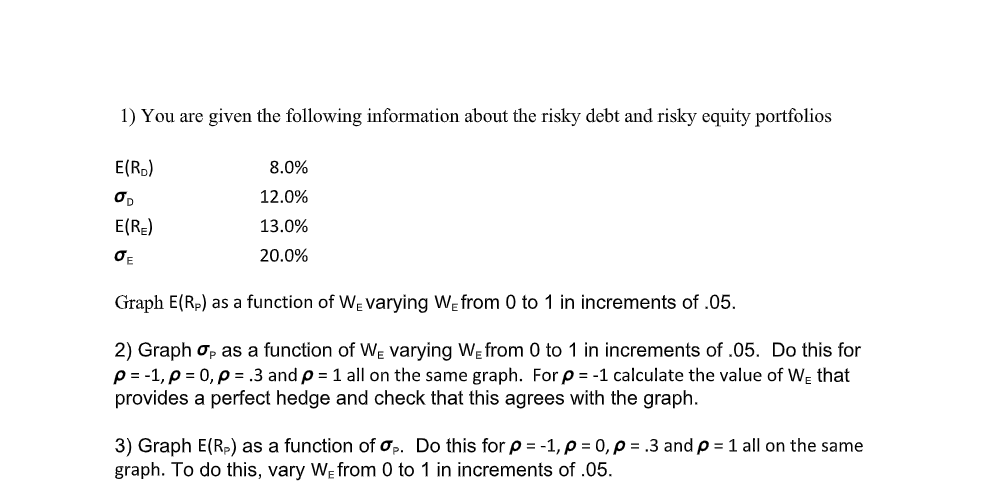

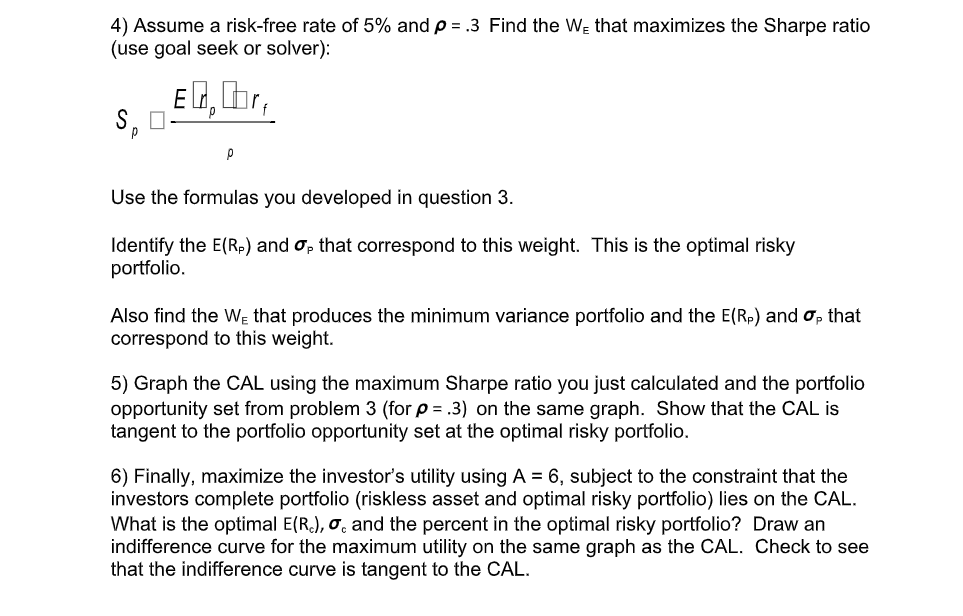

1) You are given the following information about the risky debt and risky equity portfolios 8.0% E(Ro) E(R) 12.0% 13.0% 20.0% Graph E(Rp) as a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Nonprofit Fundraising Solution Powerful Revenue Strategies To Take You To The Next Level

Authors: Laurence Pagnoni , Michael Solomon

1st Edition

0814432964,0814432972