Answered step by step

Verified Expert Solution

Question

1 Approved Answer

10. If such flexibility, risk, and income are major factors in selecting a financing alternative, how should these considerations be defined and measured? Case 31

10. If such flexibility, risk, and income are major factors in selecting a financing alternative, how should these considerations be defined and measured?

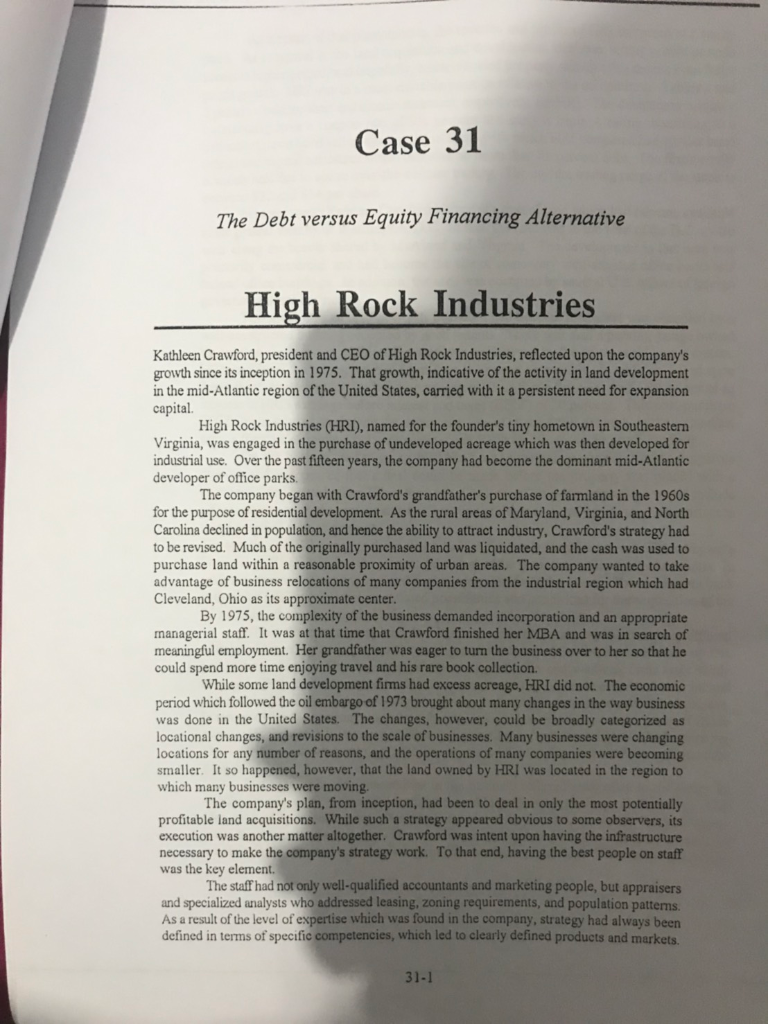

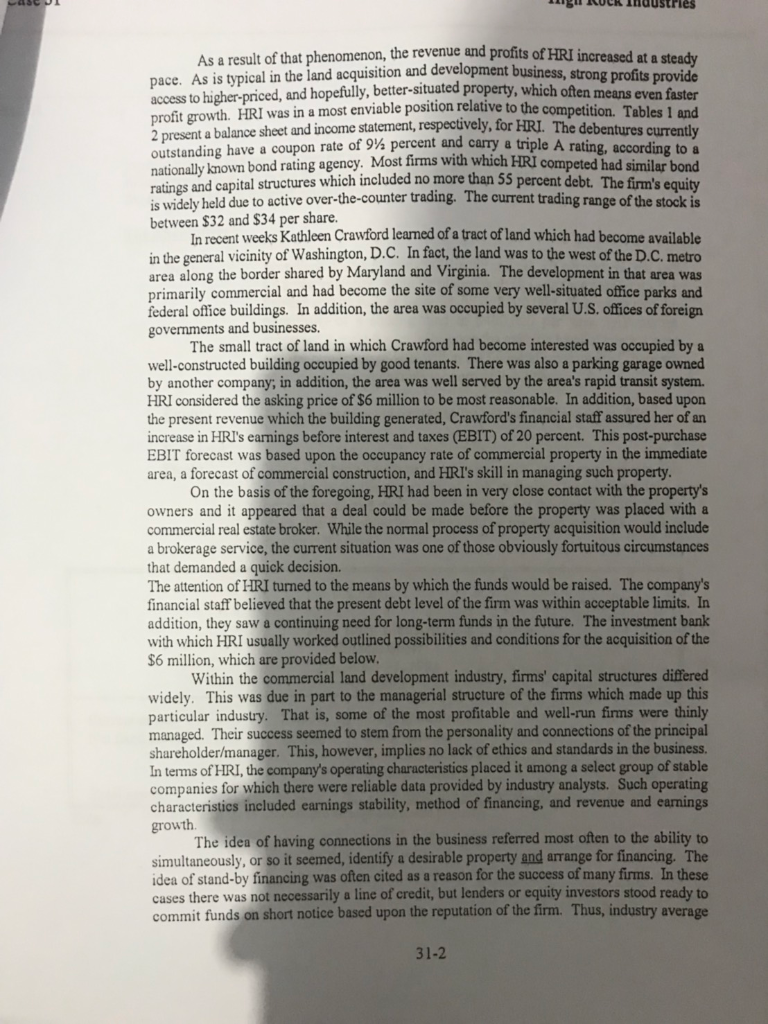

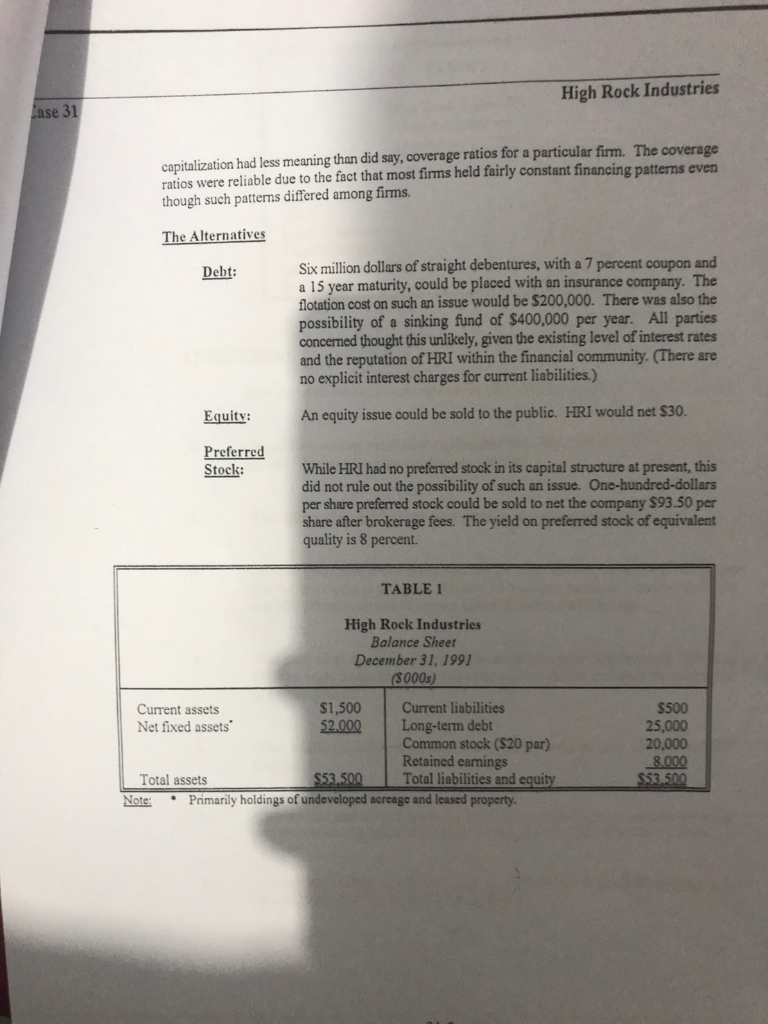

Case 31 The Debt versus Equity Financing Alternative High Rock Industries Kathleen Crawford, president and CEO of High Rock Industries, reflected upon the company's growth since its inception in 1975. That growth, indicative of the activity in land development in the mid-Atlantic region of the United States, carried with it a persistent need for expansion capital High Rock Industries (HRI), named for the founder's tiny hometown in Southeastern Virginia, was engaged in the purchase of undeveloped acreage which was then developed for industrial use. Over the past fifteen years, the company had become the dominant mid-Atlantic developer of office parks The company began with Crawford's grandfather's purchase of farmland in the 1960s for for the purpose of residential development. As the rural areas of Maryland, Virginia, and North Carolina declined in population, and hence the ability to attract industry, Crawford's strategy had to be revised. Much of the originally purchased land was liquidated, and the cash was used to purchase land within a reasonable proximity of urban areas. The company wanted to take advantage of business relocations of many companies from the industrial region which had Cleveland, Ohio as its approximate center. By 1975, the complexity of the business demanded incorporation and an appropriate managerial staff. It was at that time that Crawford finished her MBA and was in search of meaningful employment. Her grandfather was eager to turn the business over to her so that he could spend more time enjoying travel and his rare book collection. While some land development firms had excess acreage, HRI did not. The economic period which followed the oil embargo of 1973 brought about many changes in the way business was done in the United States. The changes, however, could be broadly categorized as locational changes, and revisions to the scale of businesses. Many businesses were changing locations for any number of reasons, and the operations of many companies were becoming smaller. It so happened, however, that the land owned by HRI was located in the region to which many businesses were moving. The company's plan, from inception, had been to deal in only the most potentially profitable land acquisitions. While such a strategy appeared obvious to some observers, its execution was another matter altogether. Crawford was intent upon having the infrastructure necessary to make the company's strategy work. To that end, having the best people on staff was the key element The staff had not only well-qualified accountants and marketing people, but appraisers and specialized analysts who addressed leasing, zoning requirements, and population patterns As a result of the level of expertise which was found in the company, strategy had always been defined in terms of specific competencies, which led to clearly defined products and markets 31-1 f HRI increased at a steady n and development business, strong profits provide As a result of that phenomenon, the revenue and profits o pace. As is typical in the land acquisitio access to higher-priced, and hopefully, better-situated property, which often means even faster 2 present a balance sheet and income statement, respecively, for HRT. pend outstanding have a coupon rate of % percent and carry a triple A nationally kmown bond rating agency. Most firms with which HRI competed had similar bond profit growth. HRI was in a most enviable position relative to the com The deben currently and capital structures which included no more than 55 percent debt. The firm's equity In recent weeks Kathleen Crawford leamed of a tract of land which had become available is widely held due to active over-the-counter trading. The current trading range of the stock is between S32 and S34 per share. in the general vicinity of Washington, D.C. In fact, the land was to the west of the D.C. metro area along the border shared by Maryland and Virginia. The development in that area was rimarily commercial and had become the site of some very well-situated office parks and federal office buildings. In addition, the area was occupied by several U.S. offices of foreign govemments and businesses. The small tract of land in which Crawford had become interested was occupied by a well-constructed building occupied by good tenants. There was also a parking garage owned by another company, in addition, the area was well served by the area's rapid transit system. HRI considered the asking price of $6 million to be most reasonable. In addition, based upon the present revenue which the building generated, Crawford's financial staff assured her of an increase in HRI's earnings before interest and taxes (EBIT) of 20 percent. This post-purchase EBIT forecast was based upon the occupancy rate of commercial property in the immediate area, a forecast of commercial construction, and HRI's skill in managing such property On the basis of the foregoing, HRI had been in very close contact with the property's owners and it appeared that a deal could be made before the property was placed with a commercial real estate broker. While the normal process of property acquisition would include a brokerage service, the current situation was one of those obviously fortuitous circumstances that demanded a quick decision. The attention of HRI turned to the means by which the funds would be raised. The company's financial staff believed that the present debt level of the firm was within acceptable limits. In addition, they saw a continuing need for long-term funds in the future. The investment bank with which HRI usually worked outlined possibilities and conditions for the acquisition of the $6 million, which are provided below Within the commercial land development industry, firms' capital structures differed widely. This was due in part to the managerial structure of the firms which made up this particular industry. That is, some of the most profitable and well-run firms were thinly managed. Their success seemed to stem from the personality and connections of the principal hareholder/manager. This, however, implies no lack of ethics and standards in the business. In terms of HRI, the company's operating characteristics placed it among a select group of stable companies for which there were reliable data provided by industry analysts. Such operating characteristies included earnings stability, method of financing, and revenue and earnings th grow The idea of having connections in the business referred most often to the ability to simultaneously, or so it seemed, identify a desirable property and arrange for financing. The idea of stand-by financing was often cited as a reason for the success of many firms. In these cases there was not necessarily a line of credit, but lenders or equity investors stood ready to commit funds on short notice based upon the reputation of the firm. Thus, industry average 31-2 High Rock Industries capitalization had less meaning than did say, coverage ratios for a particular firm. The coverage ratios were reliable due to the fact that most firms held fairly constant financing patterns even though such patterns differed among firms. The Alternatives Six million dollars of straight debentures, with a 7 percent coupon and a 15 year maturity, could be placed with an insurance company. The lotation cost on such an issue would be $200,000. There was also the possibility of a sinking fund of $400,000 per year. All parties concerned thought this unlikely, given the existing level of interest rates and the reputation of HRI within the financial community. (There are no explicit interest charges for current liabilities.) Debt: An equity issue could be sold to the public. HRI would net $30 Equity Preferred Stock While HRI had no preferred stock in its capital structure at present, this did not rule out the possibility of such an issue. One-hundred-dollars per share preferred stock could be sold to net the company $93.50 per share after brokerage fees. The yield on preferred stock of equivalent quality is 8 percent. TABLE 1 High Rock Industries Balance Sheet December 31, 1991 000s) $1,500 Current liabilities 52.000 Long-term debt $500 25,000 20,000 8.000 Current assets Net fixed assets Common stock ($20 par) Retained earnings S53.500 Total liabilities and equity Total assets holdings of undeveloped acreage and leased property Note: Primarily ig RCk dustr 31 TABLE 2 High Rock Industries Income Statement December 31, 1992 $10,000,000 (5.589 300 $4,410,700 2.375000) $2,035,700 (610.710 1 424 990 Revenue Less: Cost of sales EBIT Less: Interest Taxable income Less: Taxes (30%) Profit after-tax QUESTIONS 1. Does the proposed acquisition seem to fit HRI's business pattern? Why or why not? 2. Should the proposed acquisition be financed with debt, preferred stock, or common equity? What are the relevant decision criteria? What information and data are most useful in answering Question 22 3. Calculate HRI's debt to total assets ratio and the times interest earned ratio before and after the new capital is acquired. Assume a 20 percent increase in current liabilities and a 20 percent increase in current assets. Discuss your findings. 4. What is the effect of a sinking fund requirement upon your calculations in Question 2? Why might interest rate levels or company risk factors influence the imposition of a sinking fund? What additional information would have been useful in your analysis of HRI? Explain 6. Consider your answers to Questions 2 and 3 above, then comment upon the meaning and usefulness of a probability estimate of the level of EBIT after the purchase. Is there information, in addition to the specifics of the financing alternatives, that should be provided by the investment bankers? 8. 31-4 High Rock Industries o It the stable developers such as HRI have a total debt-to-total assets ratio in the range of 48-55 percent, how much flexibility for future financing will HRI have if debt is issued at present? If such flexibility, risk, and income are major factors in selecting a financing alternative, how should these considerations be defined and measured? 10. Case 31 The Debt versus Equity Financing Alternative High Rock Industries Kathleen Crawford, president and CEO of High Rock Industries, reflected upon the company's growth since its inception in 1975. That growth, indicative of the activity in land development in the mid-Atlantic region of the United States, carried with it a persistent need for expansion capital High Rock Industries (HRI), named for the founder's tiny hometown in Southeastern Virginia, was engaged in the purchase of undeveloped acreage which was then developed for industrial use. Over the past fifteen years, the company had become the dominant mid-Atlantic developer of office parks The company began with Crawford's grandfather's purchase of farmland in the 1960s for for the purpose of residential development. As the rural areas of Maryland, Virginia, and North Carolina declined in population, and hence the ability to attract industry, Crawford's strategy had to be revised. Much of the originally purchased land was liquidated, and the cash was used to purchase land within a reasonable proximity of urban areas. The company wanted to take advantage of business relocations of many companies from the industrial region which had Cleveland, Ohio as its approximate center. By 1975, the complexity of the business demanded incorporation and an appropriate managerial staff. It was at that time that Crawford finished her MBA and was in search of meaningful employment. Her grandfather was eager to turn the business over to her so that he could spend more time enjoying travel and his rare book collection. While some land development firms had excess acreage, HRI did not. The economic period which followed the oil embargo of 1973 brought about many changes in the way business was done in the United States. The changes, however, could be broadly categorized as locational changes, and revisions to the scale of businesses. Many businesses were changing locations for any number of reasons, and the operations of many companies were becoming smaller. It so happened, however, that the land owned by HRI was located in the region to which many businesses were moving. The company's plan, from inception, had been to deal in only the most potentially profitable land acquisitions. While such a strategy appeared obvious to some observers, its execution was another matter altogether. Crawford was intent upon having the infrastructure necessary to make the company's strategy work. To that end, having the best people on staff was the key element The staff had not only well-qualified accountants and marketing people, but appraisers and specialized analysts who addressed leasing, zoning requirements, and population patterns As a result of the level of expertise which was found in the company, strategy had always been defined in terms of specific competencies, which led to clearly defined products and markets 31-1 f HRI increased at a steady n and development business, strong profits provide As a result of that phenomenon, the revenue and profits o pace. As is typical in the land acquisitio access to higher-priced, and hopefully, better-situated property, which often means even faster 2 present a balance sheet and income statement, respecively, for HRT. pend outstanding have a coupon rate of % percent and carry a triple A nationally kmown bond rating agency. Most firms with which HRI competed had similar bond profit growth. HRI was in a most enviable position relative to the com The deben currently and capital structures which included no more than 55 percent debt. The firm's equity In recent weeks Kathleen Crawford leamed of a tract of land which had become available is widely held due to active over-the-counter trading. The current trading range of the stock is between S32 and S34 per share. in the general vicinity of Washington, D.C. In fact, the land was to the west of the D.C. metro area along the border shared by Maryland and Virginia. The development in that area was rimarily commercial and had become the site of some very well-situated office parks and federal office buildings. In addition, the area was occupied by several U.S. offices of foreign govemments and businesses. The small tract of land in which Crawford had become interested was occupied by a well-constructed building occupied by good tenants. There was also a parking garage owned by another company, in addition, the area was well served by the area's rapid transit system. HRI considered the asking price of $6 million to be most reasonable. In addition, based upon the present revenue which the building generated, Crawford's financial staff assured her of an increase in HRI's earnings before interest and taxes (EBIT) of 20 percent. This post-purchase EBIT forecast was based upon the occupancy rate of commercial property in the immediate area, a forecast of commercial construction, and HRI's skill in managing such property On the basis of the foregoing, HRI had been in very close contact with the property's owners and it appeared that a deal could be made before the property was placed with a commercial real estate broker. While the normal process of property acquisition would include a brokerage service, the current situation was one of those obviously fortuitous circumstances that demanded a quick decision. The attention of HRI turned to the means by which the funds would be raised. The company's financial staff believed that the present debt level of the firm was within acceptable limits. In addition, they saw a continuing need for long-term funds in the future. The investment bank with which HRI usually worked outlined possibilities and conditions for the acquisition of the $6 million, which are provided below Within the commercial land development industry, firms' capital structures differed widely. This was due in part to the managerial structure of the firms which made up this particular industry. That is, some of the most profitable and well-run firms were thinly managed. Their success seemed to stem from the personality and connections of the principal hareholder/manager. This, however, implies no lack of ethics and standards in the business. In terms of HRI, the company's operating characteristics placed it among a select group of stable companies for which there were reliable data provided by industry analysts. Such operating characteristies included earnings stability, method of financing, and revenue and earnings th grow The idea of having connections in the business referred most often to the ability to simultaneously, or so it seemed, identify a desirable property and arrange for financing. The idea of stand-by financing was often cited as a reason for the success of many firms. In these cases there was not necessarily a line of credit, but lenders or equity investors stood ready to commit funds on short notice based upon the reputation of the firm. Thus, industry average 31-2 High Rock Industries capitalization had less meaning than did say, coverage ratios for a particular firm. The coverage ratios were reliable due to the fact that most firms held fairly constant financing patterns even though such patterns differed among firms. The Alternatives Six million dollars of straight debentures, with a 7 percent coupon and a 15 year maturity, could be placed with an insurance company. The lotation cost on such an issue would be $200,000. There was also the possibility of a sinking fund of $400,000 per year. All parties concerned thought this unlikely, given the existing level of interest rates and the reputation of HRI within the financial community. (There are no explicit interest charges for current liabilities.) Debt: An equity issue could be sold to the public. HRI would net $30 Equity Preferred Stock While HRI had no preferred stock in its capital structure at present, this did not rule out the possibility of such an issue. One-hundred-dollars per share preferred stock could be sold to net the company $93.50 per share after brokerage fees. The yield on preferred stock of equivalent quality is 8 percent. TABLE 1 High Rock Industries Balance Sheet December 31, 1991 000s) $1,500 Current liabilities 52.000 Long-term debt $500 25,000 20,000 8.000 Current assets Net fixed assets Common stock ($20 par) Retained earnings S53.500 Total liabilities and equity Total assets holdings of undeveloped acreage and leased property Note: Primarily ig RCk dustr 31 TABLE 2 High Rock Industries Income Statement December 31, 1992 $10,000,000 (5.589 300 $4,410,700 2.375000) $2,035,700 (610.710 1 424 990 Revenue Less: Cost of sales EBIT Less: Interest Taxable income Less: Taxes (30%) Profit after-tax QUESTIONS 1. Does the proposed acquisition seem to fit HRI's business pattern? Why or why not? 2. Should the proposed acquisition be financed with debt, preferred stock, or common equity? What are the relevant decision criteria? What information and data are most useful in answering Question 22 3. Calculate HRI's debt to total assets ratio and the times interest earned ratio before and after the new capital is acquired. Assume a 20 percent increase in current liabilities and a 20 percent increase in current assets. Discuss your findings. 4. What is the effect of a sinking fund requirement upon your calculations in Question 2? Why might interest rate levels or company risk factors influence the imposition of a sinking fund? What additional information would have been useful in your analysis of HRI? Explain 6. Consider your answers to Questions 2 and 3 above, then comment upon the meaning and usefulness of a probability estimate of the level of EBIT after the purchase. Is there information, in addition to the specifics of the financing alternatives, that should be provided by the investment bankers? 8. 31-4 High Rock Industries o It the stable developers such as HRI have a total debt-to-total assets ratio in the range of 48-55 percent, how much flexibility for future financing will HRI have if debt is issued at present? If such flexibility, risk, and income are major factors in selecting a financing alternative, how should these considerations be defined and measured? 10

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Forensics Body Of Knowledge

Authors: Darrell D. Dorrell, Gregory A. Gadawski

1st Edition

0470880856, 978-0470880852