Answered step by step

Verified Expert Solution

Question

1 Approved Answer

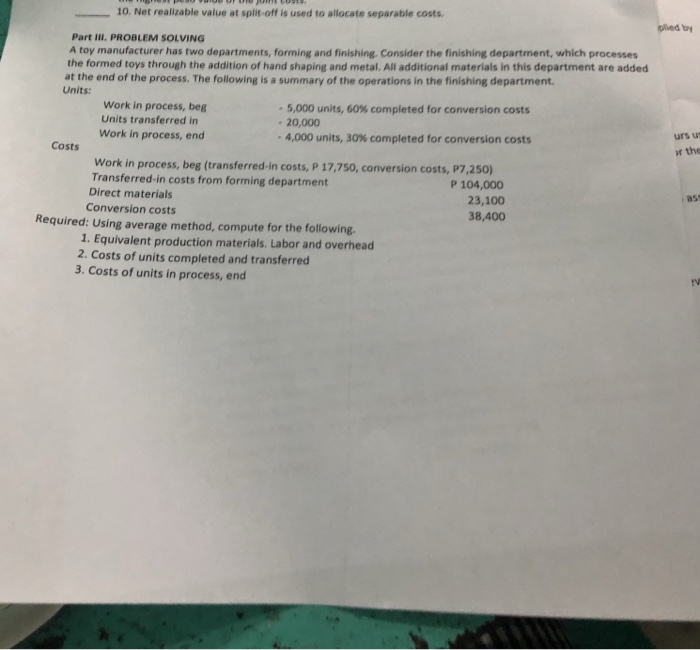

10. Net realizable value at split-off is used to allocate separable costs. pied by Part IlI, PROBLEM SOLVING A toy manufacturer has two departments, forming

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Electronic Health Records An Audit And Internal Control Guide

Authors: Rebecca S. Busch

1st Edition

0470258209, 978-0470258200