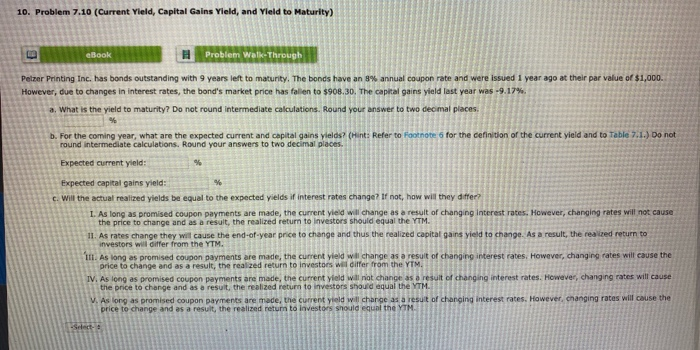

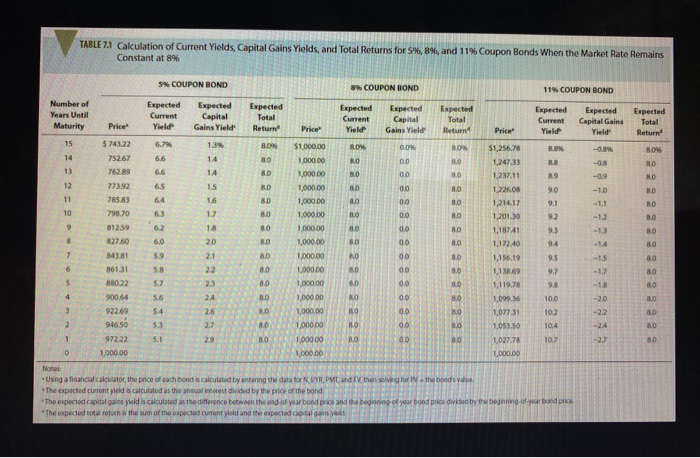

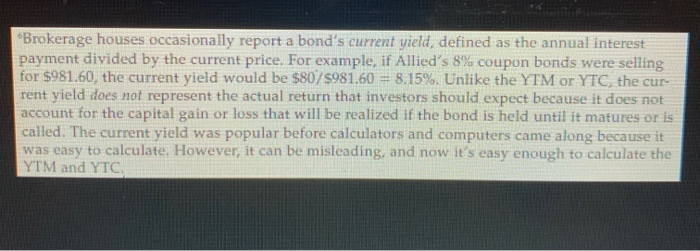

10. Problem 7.10 (Current Yield, Capital Gains Yield, and Yield to Maturity Problem Walkie-Thr Petzer Printing Inc. has bonds outstanding with 9 years left to maturity. The bonds have an 8% annual coupon rate and were issued 1 year ago at their par value of $1,000 However, due to changes in interest rates, the band's market price has fallen to $908.30. The capital gains yield last year was -9.17%. a. What is the yield to maturity? Do not round intermediate calculations. Round your answer to two deomal places b. For the coming year, what are the expected current and capital gains yields (Hint: Refer to footnote round Intermediate calculations. Round your answers to two decimal places for the definition of the current vield and to Table 2.1) Do not Expected current yield: Expected capital gains yield: c. Will the actual realized yields be equal to the expected yields if interest rates change? If not, how will they differ? 1. As long as promised coupon payments are made, the current yield will change as a result of changing interest rates. However, changing rates will not cause the price to change and as a result, the realized return to investors should equal the YTM 11. As rates change they will cause the end-of-year price to change and thus the realized capital gains yield to change. As a result, the realized return to investors will differ from the YTM. 11. As long as promised coupon payments are made, the current yield will change as a result of changing interest rates. However, changing rates will cause the price to change and as a result, the realized return to investors wil differ from the YTM IV. As long as promised coupon payments are made, the current yield will not change as a result of changing interest rates. However, changing rates will cause the price to change and as a result, the realized return to investors should equal the YTM ! V. As long as promised coupon payments are made, the current yield will change as a result of changing interest rates. However, changing rates will cause the price to change and as a result, the realized retum to investors should equal the YTM TABLE 7.1 Calculation of Current Yields, Capital Gains Yields, and Total Returns for S. 8 Constant at 8% and 11% Coupon Bonds When the Market Rate Remains Expected Total Return BO 123711 1,201.30 5% COUPON BOND % COUPON BOND 11% COUPON BOND Number of Expected Expected Expected Expected Expected Expected Expected Years Until Current Expected Capital Total Current Capital Total Maturity Price Yield Current Gains Yield Capital Gains Return Price Yield Gains Yield Return Yield Yield $743.22 $1.000.00 -0 % 752.67 1,000.00 1,247.33 762.89 1,000.00 1,000.00 1.226.08 1,000.00 1.214.17 1,000.00 1,000.00 198741 1,000.00 1,000.00 1,156,19 1,000.00 1,119.78 900,64 1,000.00 922.69 1,000.00 946.50 8.0 1,000.00 972 22 801.000.00 D 1 ,000.00 1,000.00 1.000.00 Note Using a calculator, the price of each bond is calculated by entering the data for NVIR. PMC and then sol l te The expected current yield calculated as the annual interest divided by the price of the bord The expected capital gains yield is calculated as the difference between the end of year bond price and the beginning of year bond price divided by the beginning of var bond The expected to the sum of the expected current yield and the expected a gainst 77 2389 9999999999999 99999999999999 8888888888888 888888888 69 1,000.00 "Brokerage houses occasionally report a bond's current yield, defined as the annual interest payment divided by the current price. For example, if Allied's 8% coupon bonds were selling for $981.60, the current yield would be $80/$981.60 = 8.15%. Unlike the YTM or YTC, the cur rent yield does not represent the actual return that investors should expect because it does not account for the capital gain or loss that will be realized if the bond is held until it matures or is called. The current yield was popular before calculators and computers came along because it was easy to calculate. However, it can be misleading, and now it's easy enough to calculate the YTM and YTC 10. Problem 7.10 (Current Yield, Capital Gains Yield, and Yield to Maturity Problem Walkie-Thr Petzer Printing Inc. has bonds outstanding with 9 years left to maturity. The bonds have an 8% annual coupon rate and were issued 1 year ago at their par value of $1,000 However, due to changes in interest rates, the band's market price has fallen to $908.30. The capital gains yield last year was -9.17%. a. What is the yield to maturity? Do not round intermediate calculations. Round your answer to two deomal places b. For the coming year, what are the expected current and capital gains yields (Hint: Refer to footnote round Intermediate calculations. Round your answers to two decimal places for the definition of the current vield and to Table 2.1) Do not Expected current yield: Expected capital gains yield: c. Will the actual realized yields be equal to the expected yields if interest rates change? If not, how will they differ? 1. As long as promised coupon payments are made, the current yield will change as a result of changing interest rates. However, changing rates will not cause the price to change and as a result, the realized return to investors should equal the YTM 11. As rates change they will cause the end-of-year price to change and thus the realized capital gains yield to change. As a result, the realized return to investors will differ from the YTM. 11. As long as promised coupon payments are made, the current yield will change as a result of changing interest rates. However, changing rates will cause the price to change and as a result, the realized return to investors wil differ from the YTM IV. As long as promised coupon payments are made, the current yield will not change as a result of changing interest rates. However, changing rates will cause the price to change and as a result, the realized return to investors should equal the YTM ! V. As long as promised coupon payments are made, the current yield will change as a result of changing interest rates. However, changing rates will cause the price to change and as a result, the realized retum to investors should equal the YTM TABLE 7.1 Calculation of Current Yields, Capital Gains Yields, and Total Returns for S. 8 Constant at 8% and 11% Coupon Bonds When the Market Rate Remains Expected Total Return BO 123711 1,201.30 5% COUPON BOND % COUPON BOND 11% COUPON BOND Number of Expected Expected Expected Expected Expected Expected Expected Years Until Current Expected Capital Total Current Capital Total Maturity Price Yield Current Gains Yield Capital Gains Return Price Yield Gains Yield Return Yield Yield $743.22 $1.000.00 -0 % 752.67 1,000.00 1,247.33 762.89 1,000.00 1,000.00 1.226.08 1,000.00 1.214.17 1,000.00 1,000.00 198741 1,000.00 1,000.00 1,156,19 1,000.00 1,119.78 900,64 1,000.00 922.69 1,000.00 946.50 8.0 1,000.00 972 22 801.000.00 D 1 ,000.00 1,000.00 1.000.00 Note Using a calculator, the price of each bond is calculated by entering the data for NVIR. PMC and then sol l te The expected current yield calculated as the annual interest divided by the price of the bord The expected capital gains yield is calculated as the difference between the end of year bond price and the beginning of year bond price divided by the beginning of var bond The expected to the sum of the expected current yield and the expected a gainst 77 2389 9999999999999 99999999999999 8888888888888 888888888 69 1,000.00 "Brokerage houses occasionally report a bond's current yield, defined as the annual interest payment divided by the current price. For example, if Allied's 8% coupon bonds were selling for $981.60, the current yield would be $80/$981.60 = 8.15%. Unlike the YTM or YTC, the cur rent yield does not represent the actual return that investors should expect because it does not account for the capital gain or loss that will be realized if the bond is held until it matures or is called. The current yield was popular before calculators and computers came along because it was easy to calculate. However, it can be misleading, and now it's easy enough to calculate the YTM and YTC