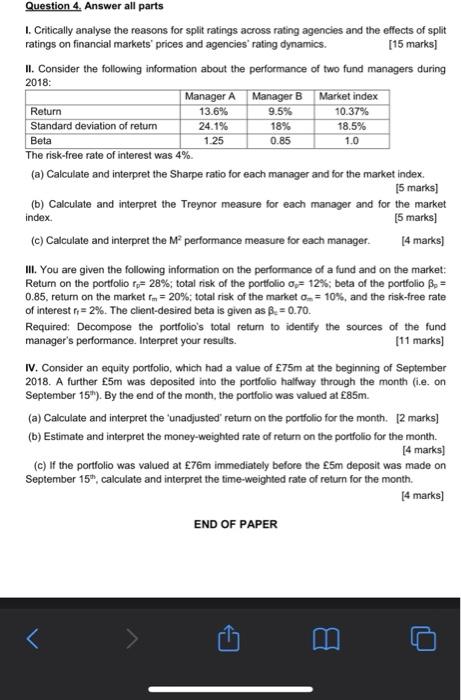

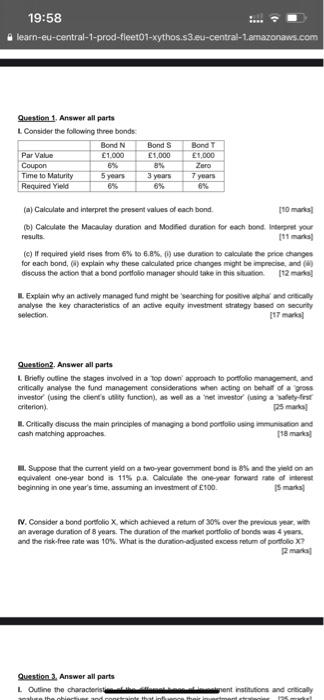

10.37% 1.0 Question 4. Answer all parts 1. Critically analyse the reasons for split ratings across rating agencies and the effects of split ratings on financial markets' prices and agencies" rating dynamics. [15 marks) II. Consider the following information about the performance of two fund managers during 2018: Manager A Manager B Market index Return 13.6% 9.5% Standard deviation of return 24.1% 18% 18.5% Beta 1.25 0.85 The risk-free rate of interest was 4% (a) Calculate and interpret the Sharpe ratio for each manager and for the market index. 15 marks] (b) Calculate and interpret the Treynor measure for each manager and for the market index (5 marks] (c) Calculate and interpret the MP performance measure for each manager [4 marks) III. You are given the following information on the performance of a fund and on the market: Return on the portfolio r= 28%; total risk of the portfolio o = 12%; beta of the portfolio Be= 0.85, return on the market rm = 20%; total risk of the market - = 10%, and the risk-free rate of interest r = 2%. The client-desired beta is given as B-= 0.70. Required: Decompose the portfolio's total return to identify the sources of the fund manager's performance. Interpret your results. [11 marks) IV. Consider an equity portfolio, which had a value of 75m at the beginning of September 2018. A further 5m was deposited into the portfolio halfway through the month (i.e. on September 15"). By the end of the month, the portfolio was valued at 85m. (a) Calculate and interpret the 'unadjusted' return on the portfolio for the month. 12 marks] (b) Estimate and interpret the money-weighted rate of return on the portfolio for the month. [4 marks) (c) If the portfolio was valued at 76m immediately before the 5m deposit was made on September 15", calculate and interpret the time-weighted rate of return for the month. [4 marks) END OF PAPER 19:58 learn-eu-central-1-prod-fleet01-xythos.s3.eu-central-1.amazonaws.com Question 1. Answer all parts L. Consider the following three bonds Bond N Par Value 1.000 Coupon 6% Time to Maturity 5 years Required Yield 6% Bonds 1,000 8% 3 years 6% Bondy 1,000 Zero 7 years 6% (a) Calculate and interpret the present values of each bond 110 mars Calculate the Macaulay duration and Modhed duration for each bond. Interpret you results (c) If required yield rises from 6% to 6.8%. )use duration to calculate the price changes for each bond, () explain why these calculated price changes might be precise, and discuss the action that a bond portfolio manager should take in this situation. [12 Explain why an actively managed fund might be searching for positive and entically analyse the key characteristics of an active equity investment strategy based on security selection Question. Answer all parts 1. Briefly outine the stages involved in a top downl' approach to portfolio Management and critically analyse the fund management considerations when acting on behalf of a gross investor (using the client's utility function, as well as a net investor using a safety first criterion) ps made Critically discuss the main principles of managing a bond portfolio using immunition and cash matching approaches 118 mars! 1. Suppose that the current yield on a two-year government bond is 85 and the old on equivalent one-year bond is 11% pa Calculate the one year forwarde of met beginning in one year's time, assuming an investment of 100 N. Consider a bond portfolio X, which achieved a retum of 30% over the previous year, with an average duration of 8 years. The duration of the market portfolio of bonds was 4 years and the risk-free rate was 10%. What is the duration adjusted excess Teum of portfolio X? mata Question Answer all parts L Outline the characters the chic entinstons and entical nar 10.37% 1.0 Question 4. Answer all parts 1. Critically analyse the reasons for split ratings across rating agencies and the effects of split ratings on financial markets' prices and agencies" rating dynamics. [15 marks) II. Consider the following information about the performance of two fund managers during 2018: Manager A Manager B Market index Return 13.6% 9.5% Standard deviation of return 24.1% 18% 18.5% Beta 1.25 0.85 The risk-free rate of interest was 4% (a) Calculate and interpret the Sharpe ratio for each manager and for the market index. 15 marks] (b) Calculate and interpret the Treynor measure for each manager and for the market index (5 marks] (c) Calculate and interpret the MP performance measure for each manager [4 marks) III. You are given the following information on the performance of a fund and on the market: Return on the portfolio r= 28%; total risk of the portfolio o = 12%; beta of the portfolio Be= 0.85, return on the market rm = 20%; total risk of the market - = 10%, and the risk-free rate of interest r = 2%. The client-desired beta is given as B-= 0.70. Required: Decompose the portfolio's total return to identify the sources of the fund manager's performance. Interpret your results. [11 marks) IV. Consider an equity portfolio, which had a value of 75m at the beginning of September 2018. A further 5m was deposited into the portfolio halfway through the month (i.e. on September 15"). By the end of the month, the portfolio was valued at 85m. (a) Calculate and interpret the 'unadjusted' return on the portfolio for the month. 12 marks] (b) Estimate and interpret the money-weighted rate of return on the portfolio for the month. [4 marks) (c) If the portfolio was valued at 76m immediately before the 5m deposit was made on September 15", calculate and interpret the time-weighted rate of return for the month. [4 marks) END OF PAPER 19:58 learn-eu-central-1-prod-fleet01-xythos.s3.eu-central-1.amazonaws.com Question 1. Answer all parts L. Consider the following three bonds Bond N Par Value 1.000 Coupon 6% Time to Maturity 5 years Required Yield 6% Bonds 1,000 8% 3 years 6% Bondy 1,000 Zero 7 years 6% (a) Calculate and interpret the present values of each bond 110 mars Calculate the Macaulay duration and Modhed duration for each bond. Interpret you results (c) If required yield rises from 6% to 6.8%. )use duration to calculate the price changes for each bond, () explain why these calculated price changes might be precise, and discuss the action that a bond portfolio manager should take in this situation. [12 Explain why an actively managed fund might be searching for positive and entically analyse the key characteristics of an active equity investment strategy based on security selection Question. Answer all parts 1. Briefly outine the stages involved in a top downl' approach to portfolio Management and critically analyse the fund management considerations when acting on behalf of a gross investor (using the client's utility function, as well as a net investor using a safety first criterion) ps made Critically discuss the main principles of managing a bond portfolio using immunition and cash matching approaches 118 mars! 1. Suppose that the current yield on a two-year government bond is 85 and the old on equivalent one-year bond is 11% pa Calculate the one year forwarde of met beginning in one year's time, assuming an investment of 100 N. Consider a bond portfolio X, which achieved a retum of 30% over the previous year, with an average duration of 8 years. The duration of the market portfolio of bonds was 4 years and the risk-free rate was 10%. What is the duration adjusted excess Teum of portfolio X? mata Question Answer all parts L Outline the characters the chic entinstons and entical nar