Question

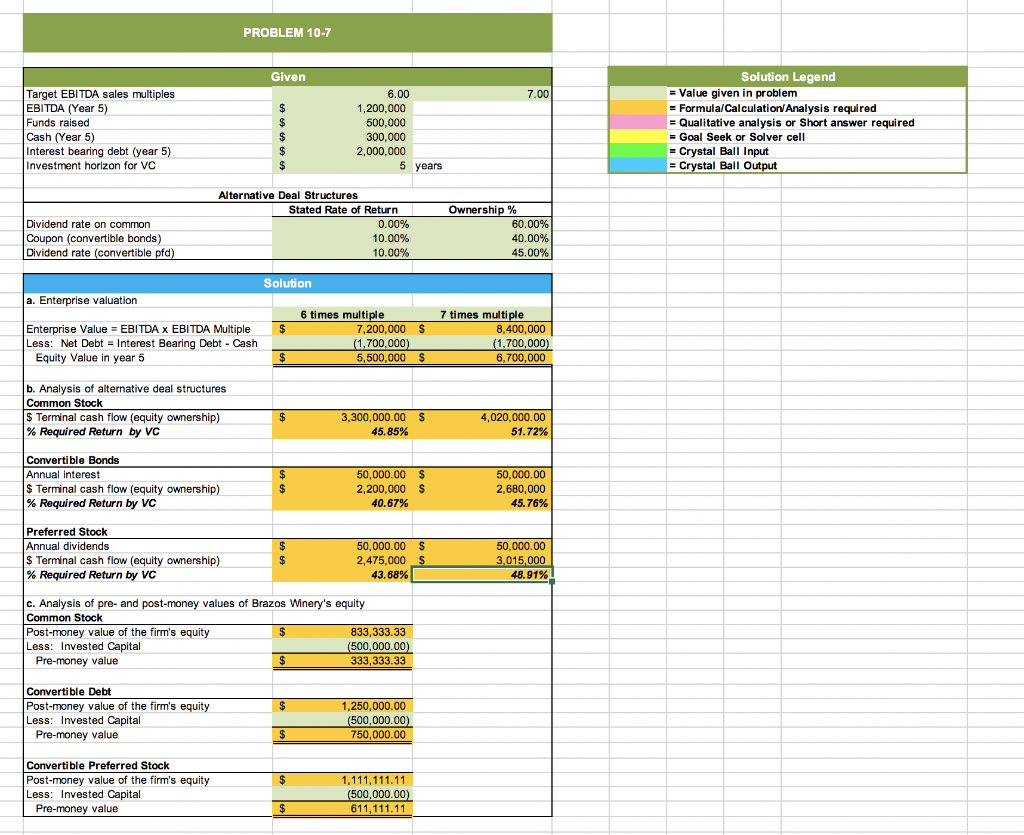

10.7 VC VALUATION AND DEAL STRUCTURING Brazos Winery was established eight years ago by Anna and Jerry Lutz with the purchase of 200 acres of

10.7 VC VALUATION AND DEAL STRUCTURING

Brazos Winery was established eight years ago by Anna and Jerry Lutz with the purchase of 200 acres of land. The purchase was followed by a period of intensive planting and development of the grape vineyard. The vineyard is now entering its second year of production.

In March 2015, the Lutzes determined that they needed to raise $500,000 to purchase equipment to bottle their private-label wines. Unfortunately, they have reached the limits of what their banker can finance and have put all their personal financial resources into the business. In short, they need more equity capital, and they cannot provide it themselves.

Their banker recommended that they contact a venture capital (VC) firm in New Orleans that sometimes makes investments in ventures such as the Brazos Winery. He also recommended that they prepare for the meeting by organizing their financial fore- cast for the next five years. The banker explained that VCs generally target a five-year term for their investments, so it was important that they provide the information needed to value the winery at the end of five years.

After a careful analysis of their plans for the winery, the Lutzes estimate that earnings before interest, taxes, depreciation, and amortization (EBITDA) in five years will be $1.2 million. In addition to the EBITDA forecast, the Lutzes estimate that they will need to borrow $2.4 million by 2013 to fund additional expansion of their operations. Their banker indicated that his bank could be counted on for $2 million in debt, assuming they were successful in raising the needed equity funds from the VC. Furthermore, the remaining $400,000 would be in the form of accounts payable. Finally, the Lutzes believe that their cash balance will reach $300,000 at the end of five years.

The Lutzes are particularly concerned about how much of the firms ownership they will have to give up in order to entice the VC to invest. The VC offers three alternative ways of funding the winerys $500,000 financing requirements. Each alternative call for a different ownership share:

- Straight common stock that pays no dividend. With this option, the VC asks for 60% of the firms common stock in five years.

- Convertible debt paying 10% annual interest and 40% of the firms common stock at conversion in Year 5.

- Convertible preferred stock with a 10% annual dividend and the right to convert the preferred stock into 45% ownership of the firms common stock at the end of Year 5.

a. If the VC estimates that the winery should have an enterprise value equal to six to seven times estimated EBITDA in five years, what do you estimate the value of the winery to be in 2019? What will the equity in the firm be worth? (Hint: Consider both the six- and seven-times-EBITDA multiple.)

b. Based on the deal terms offered, what rate of return does the VC require for each of the three financing alternatives? Which alternative should the Lutzes select based on the expected cost of financing?

c. What is the pre- and post-money value of the firm based on the three sets of deal terms offered by the VC? Why are the estimates different for each of the deal structures?

My question is how do I calculate and find the percentages of 45.85%, 51.72%, 40.67%, 45.76%, 43.68% and 48.91%.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting For Decision Makers

Authors: Peter Atrill, Eddie McLaney

9th Edition

1292251255, 9781292251257