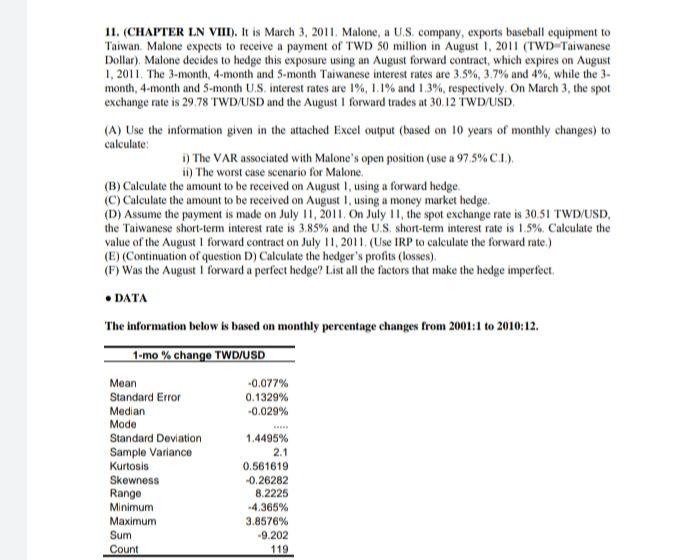

11. (CHAPTER LN VIIT). It is March 3, 2011. Malone, a US company, exports baseball equipment to Taiwan. Malone expects to receive a payment of TWD 50 million in August 1, 2011 (TWD Taiwanese Dollar). Malone decides to hedge this exposure using an August forward contract, which expires on August 1. 2011. The 3-month, 4-month and S-month Taiwanese interest rates are 3.5%, 3.7% and 4%, while the 3. month, 4-month and S-month U.S. interest rates are 1%, 1.1% and 1,3%, respectively. On March 3, the spot exchange rate is 29.78 TWD/USD and the August 1 forward trades at 30.12 TWD/USD. (A) Use the information given in the attached Excel output (based on 10 years of monthly changes) to calculate 1) The VAR associated with Malone's open position (use a 97 5% CI). ii) The worst case scenario for Malone (B) Calculate the amount to be received on August 1, using a forward hedge (C) Calculate the amount to be received on August 1, using a money market hedge. (D) Assume the payment is made on July 11, 2011. On July 11, the spot exchange rate is 30.51 TWD USD. the Taiwanese short-term interest rate is 3.85% and the US short-term interest rate is 1.5%. Calculate the value of the August I forward contract on July 11, 2011. (Use IRP to calculate the forward rate) (E) (Continuation of question D) Calculate the hedger's profits (losses). (F) Was the August I forward a perfect hedge? List all the factors that make the hedge imperfect DATA The information below is based on monthly percentage changes from 2001:1 to 2010:12. 1-mo % change TWD/USD Mean -0.077% Standard Error 0.1329% Median -0.029% Mode Standard Deviation 1.4495% Sample Variance 2.1 Kurtosis 0.561619 Skewness -0.26282 Range 8.2225 Minimum -4.365% Maximum 3.8576% Sum -9.202 Count 119 11. (CHAPTER LN VIIT). It is March 3, 2011. Malone, a US company, exports baseball equipment to Taiwan. Malone expects to receive a payment of TWD 50 million in August 1, 2011 (TWD Taiwanese Dollar). Malone decides to hedge this exposure using an August forward contract, which expires on August 1. 2011. The 3-month, 4-month and S-month Taiwanese interest rates are 3.5%, 3.7% and 4%, while the 3. month, 4-month and S-month U.S. interest rates are 1%, 1.1% and 1,3%, respectively. On March 3, the spot exchange rate is 29.78 TWD/USD and the August 1 forward trades at 30.12 TWD/USD. (A) Use the information given in the attached Excel output (based on 10 years of monthly changes) to calculate 1) The VAR associated with Malone's open position (use a 97 5% CI). ii) The worst case scenario for Malone (B) Calculate the amount to be received on August 1, using a forward hedge (C) Calculate the amount to be received on August 1, using a money market hedge. (D) Assume the payment is made on July 11, 2011. On July 11, the spot exchange rate is 30.51 TWD USD. the Taiwanese short-term interest rate is 3.85% and the US short-term interest rate is 1.5%. Calculate the value of the August I forward contract on July 11, 2011. (Use IRP to calculate the forward rate) (E) (Continuation of question D) Calculate the hedger's profits (losses). (F) Was the August I forward a perfect hedge? List all the factors that make the hedge imperfect DATA The information below is based on monthly percentage changes from 2001:1 to 2010:12. 1-mo % change TWD/USD Mean -0.077% Standard Error 0.1329% Median -0.029% Mode Standard Deviation 1.4495% Sample Variance 2.1 Kurtosis 0.561619 Skewness -0.26282 Range 8.2225 Minimum -4.365% Maximum 3.8576% Sum -9.202 Count 119