Question

12 Month USD LIBOR - 2.34613 With the current 12-month USD LIBOR for i US and the rates found for your currencies, estimate the spot

12 Month USD LIBOR - 2.34613

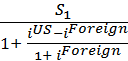

With the current 12-month USD LIBOR for iUS and the rates found for your currencies, estimate the spot rate in one year using the International Fisher Effect equation below:

S2 = S11+ iUS-iForeign1+ iForeign

1. Foreign Currency 12-Month LIBOR:

United Kingdom 0.97513

Spot Rate in 12-Months Based on USD LIBOR and Foreign Interest Rate Show initial equation and its terms and not just the final answer for full credit.

-------------------------------------------------------------------------------------------

2. Foreign Currency 12-Month LIBOR:

Tanzania 5.08%

Spot Rate in 12-Months Based on USD LIBOR and Foreign Interest Rate Show initial equation and its terms and not just the final answer for full credit.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sabotage The Business Of Finance

Authors: Ronen Palan

1st Edition

0141986247, 978-0141986241