12.1.1 Establishing Common Units, or Monetizing Comparing two (or more) projects requires all of the costs and benefits to be converted into a single unit

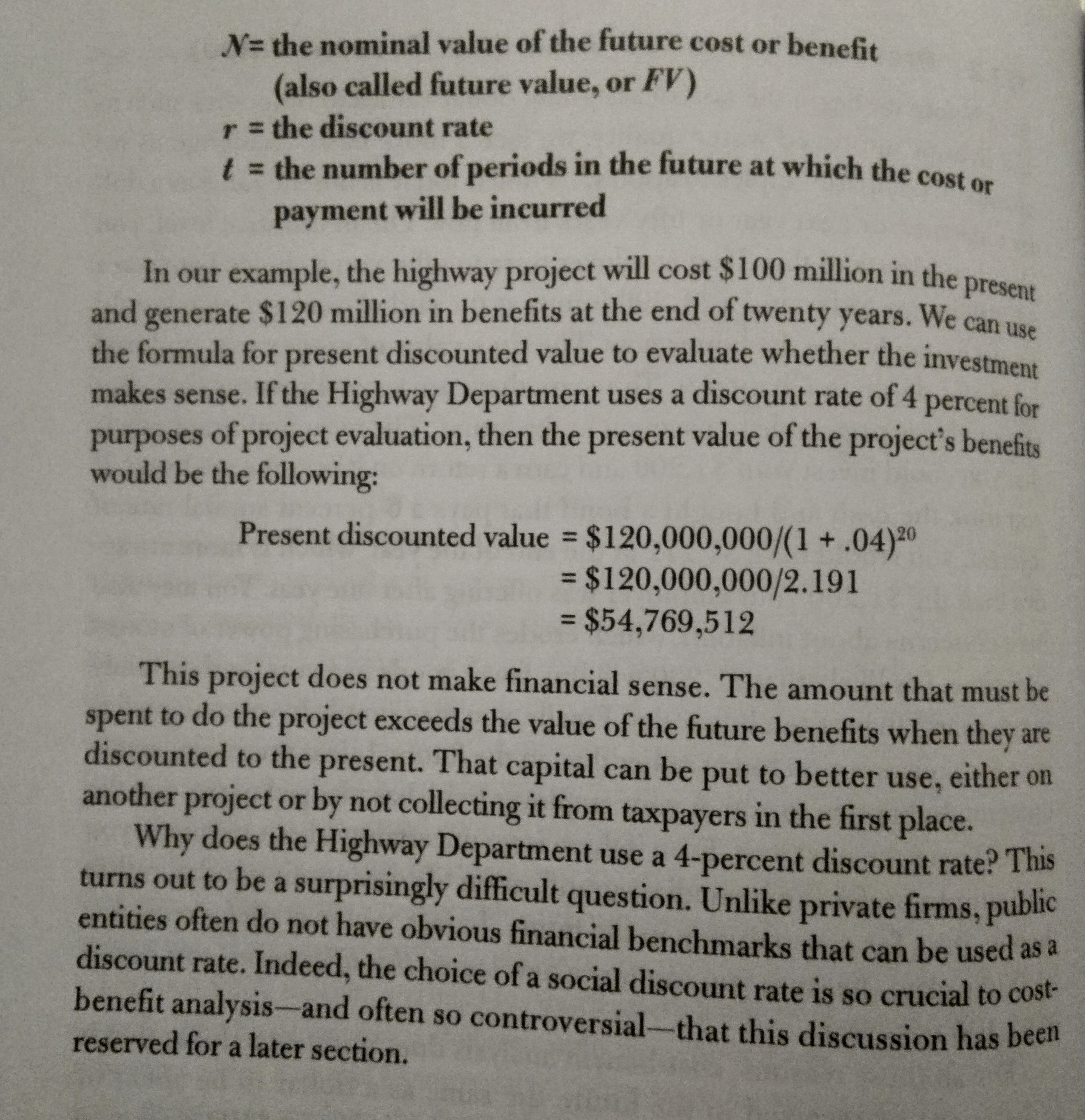

12.1.1 Establishing Common Units, or "Monetizing" Comparing two (or more) projects requires all of the costs and benefits to be converted into a single unit of measure, which is usually dollars. Only thencan we avoid the seemingly intractable challenge of comparing dissimilar things-the classic "apples and oranges." The fundamental challenge of cost. benefit analysis is to assign dollar values to the kinds of costs and benefits out. lined above. When all of the costs and benefits for competing projects are tallied up using a single measure, then the merits can be compared directly- apples to apples. Is it really possible to put a dollar value on things like faster commutes, diminished air quality, or even the loss of human life? The reality is that we have no choice as long as the goal of policy analysis is to use society's resources most productively. We must constantly make trade-offs, and cost-benefit analy. sis is a crucial tool for informing such decisions. Even when one simply refuses to put a price tag on some outcome-the extinction of a species or the loss of companionship from a spouse-cost-benefit analysis still makes the decision- making process explicit and transparent: this is what society is getting from a policy or proposal; this is what we must give up. The Office of Management and Budget, which is the office within the White House that advises the execu- tive branch on budget and regulatory issues, advises its senior managers: "A comprehensive enumeration of the different types of benefits and costs, mone- tized or not, can be helpful in identifying the full range of program effects." Shouldn't we just spend enough public money to avoid adverse outcomes like traffic fatalities, so that we don't have to put a price on lost human lives? At first glance, this seems a reasonable and humane strategy. Suppose the cost of saving the 31 projected traffic fatalities in the previous example would be an additional $200 million, perhaps for extra safety features or additional police patrols. The facile answer is that we ought to commit those additional public resources, since it would be immoral to "put a price tag on human life." Yet any such decision is made in the face of finite resources. In another department of the same municipal government, a program analyst may be advocating for better prenatal care. An additional $200 million could save 236 lives and improve the health of thousands of other children and families. Or $200 million might be spent expanding early childhood education or fighting violent crime-both of which would also improve the lives of many people. Or the $200 million could be returned to taxpayers, who could invest in their own health or otherwise spend the money in ways that would make their lives better. The goal of public policy is to make the best use of society's finite resources which requires some mechanism for evaluating decisions toward that end. Cost benefit analysis is a powerful but imperfect tool for allocating resources em ciently. The alternative is to make decisions without any objective metric at all12 COST- BENEFIT ANA 12.1.2 Present Discounted Value (Net Present Value) Even before we begin the task of assigning dollar values to outcomes such as lost lives or improved water quality, we face a more basic challenge as we attempt to compare "apples to apples." A dollar today is not the same as a dol- har tomorrow or next year or fifty years from now. On an intuitive level, you already understand this. If an employer were to offer you a choice between a $1,200 bonus today and a $1,200 bonus at the end of one year, you would almost certainly take the bonus now. The time value of money was explored in greater depth in Chapter 9. To recap, there are several reasons that pay- ment today is preferable to payment in the future. The most important one is that you could invest your $1,200 and earn a return on it over the next year. If you took the cash and bought a bond that pays a 6-percent annual rate of interest, you would have $1,272 at the end of the year, which is more attrac tive than the $1,200 your employer was offering after one year. You may also have concerns about inflation, which erodes the purchasing power of money over time. It's likely that $1,200 will buy fewer goods in a year (and certainly in ten years) than it can buy today. Finally, you may simply have some prefer- ence for consumption today rather than in the future, Life is uncertain; some- thing might happen to you or your employer (who has pledged to pay you the money) over the next year. Even if there is no uncertainty about payment, you may simply prefer the immediate gratification of consumption today, rather than waiting for consumption in the future. In fact, you may prefer receiving $1,000 today-because you can buy a new stereo this afternoon-to a bonus of $1,100 next year. For all these reasons, cost-benefit analysis does not treat a dollar that is to be spent or received in the future the same as a dollar to be spent or received in the present. Suppose a highway project will cost $100 million in the present and generate $120 million in benefits at the end of twenty years. We know that the $120 million in future benefits are worth less than if we received them today. But how much less? The most common tool for dealing with this problem is to discount all future cash flows to their equivalent value in the present, so that we can accurately compare costs and benefits that accrue at different points in time. You should recall from Chapter 9 that the formula for calculating the present discounted value (often also referred to as net present value, NPV, or simply present value) of some future sum is the following: discounted value (or net present value) = N/(1 + r)'N= the nominal value of the future cost or benefit (also called future value, or FV) r = the discount rate t = the number of periods in the future at which the cost or payment will be incurred In our example, the highway project will cost $100 million in the present and generate $120 million in benefits at the end of twenty years. We can use the formula for present discounted value to evaluate whether the investment makes sense. If the Highway Department uses a discount rate of 4 percent for purposes of project evaluation, then the present value of the project's benefits would be the following: Present discounted value = $120,000,000/(1 + .04)20 = $120,000,000/2.191 = $54,769,512 This project does not make financial sense. The amount that must be spent to do the project exceeds the value of the future benefits when they are discounted to the present. That capital can be put to better use, either on another project or by not collecting it from taxpayers in the first place. Why does the Highway Department use a 4-percent discount rate? This turns out to be a surprisingly difficult question. Unlike private firms, public entities often do not have obvious financial benchmarks that can be used as a discount rate. Indeed, the choice of a social discount rate is so crucial to cost- benefit analysis-and often so controversial-that this discussion has been reserved for a later

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance