Answered step by step

Verified Expert Solution

Question

1 Approved Answer

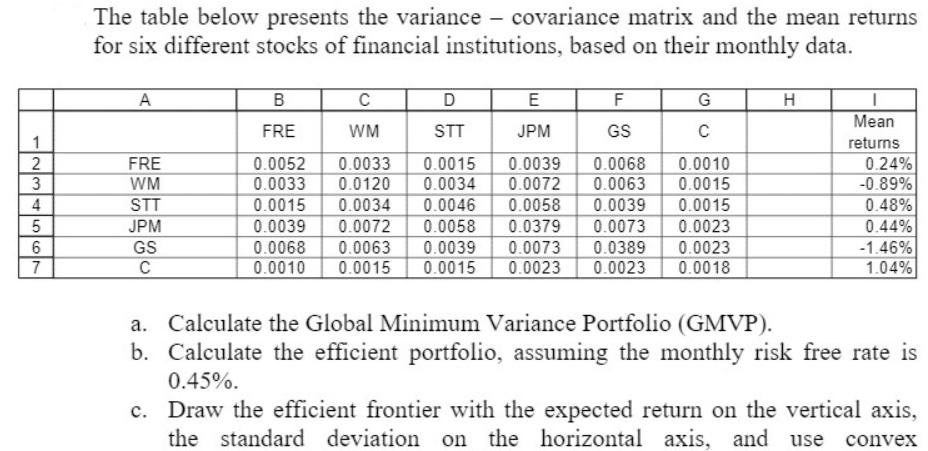

1234567 The table below presents the variance - covariance matrix and the mean returns for six different stocks of financial institutions, based on their

1234567 The table below presents the variance - covariance matrix and the mean returns for six different stocks of financial institutions, based on their monthly data. A FRE WM STT JPM GS C B FRE C WM D STT E JPM F GS G C 0.0033 0.0015 0.0068 0.0010 0.0039 0.0034 0.0072 0.0063 0.0015 0.0052 0.0033 0.0120 0.0015 0.0034 0.0046 0.0039 0.0072 0.0058 0.0379 0.0073 0.0068 0.0063 0.0039 0.0073 0.0058 0.0039 0.0015 0.0023 0.0389 0.0023 0.0010 0.0015 0.0015 0.0023 0.0023 0.0018 H I Mean returns 0.24% -0.89% 0.48% 0.44% -1.46% 1.04% a. Calculate the Global Minimum Variance Portfolio (GMVP). b. Calculate the efficient portfolio, assuming the monthly risk free rate is 0.45%. c. Draw the efficient frontier with the expected return on the vertical axis, the standard deviation on the horizontal axis, and use

Step by Step Solution

★★★★★

3.47 Rating (147 Votes )

There are 3 Steps involved in it

Step: 1

Okay here are the steps to solve this problem a To calculate the Global Minimum Variance Portfolio G...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Essentials Of Statistics A Tool For Social Research

Authors: Joseph F. Healey

3rd Edition

111182956X, 978-1133713586, 1133713580, 978-1111829568