Answered step by step

Verified Expert Solution

Question

1 Approved Answer

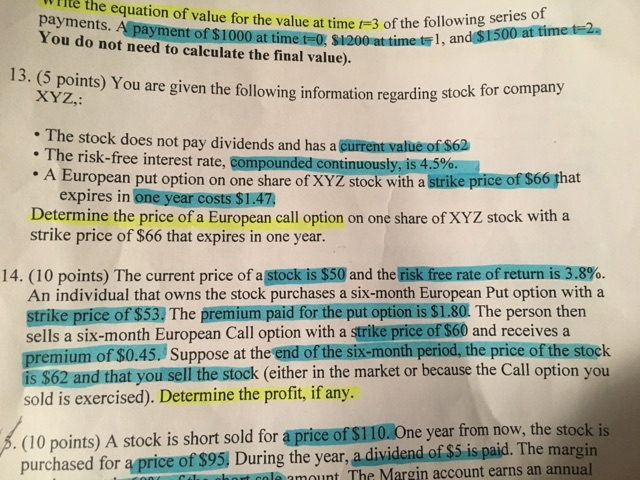

#14 please You are given the following information regarding stock for company XYZ, : The stock does not pay dividends and has a current value

#14 please

You are given the following information regarding stock for company XYZ, : The stock does not pay dividends and has a current value of $62 The risk-free interest rate, compounded continuously, is 4.5%. A European put option on one share of XYZ stock with a strike price of $66 that expires in one year costs $1.47. Determine the price of a European call option on one share of XYZ stock with a strike price of $66 that expires in one year. The current price of a stock is $50 and the risk free rate of return is 3.8%. An individual that owns the stock purchases a six-month European Put option with a strike price of $53. The premium paid for the put option is $1.80. The person then sells a six-month European Call option with a strike price of $60 and receives a premium of $0.45. Suppose at the end of the six-month period, the price of the stock is $62 and that you sell the stock (either in the market or because the Call option you sold is exercised). Determine the profit, if anyStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

DeFi And The Future Of Finance

Authors: Campbell R. Harvey, Ashwin Ramachandran, Joey Santoro, Vitalik Buterin, Fred Ehrsam

1st Edition

1119836018, 978-1119836018