Answered step by step

Verified Expert Solution

Question

1 Approved Answer

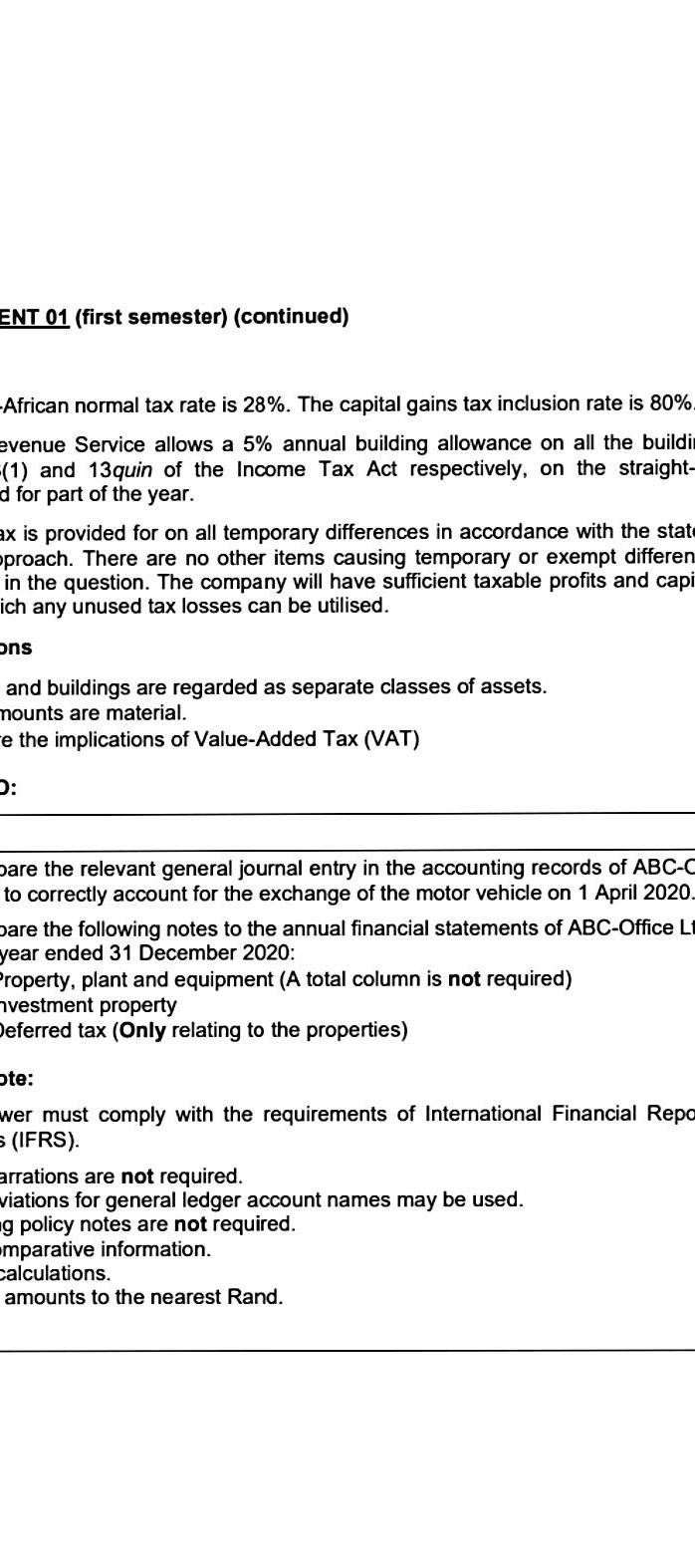

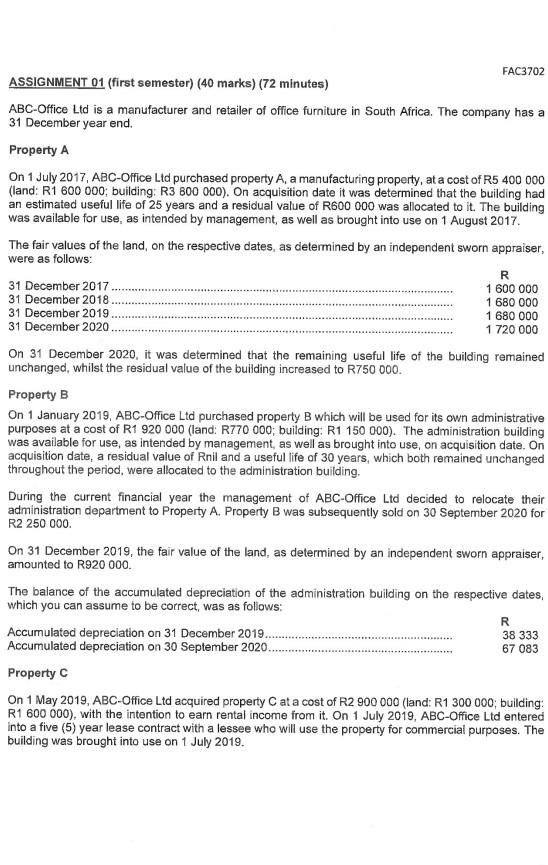

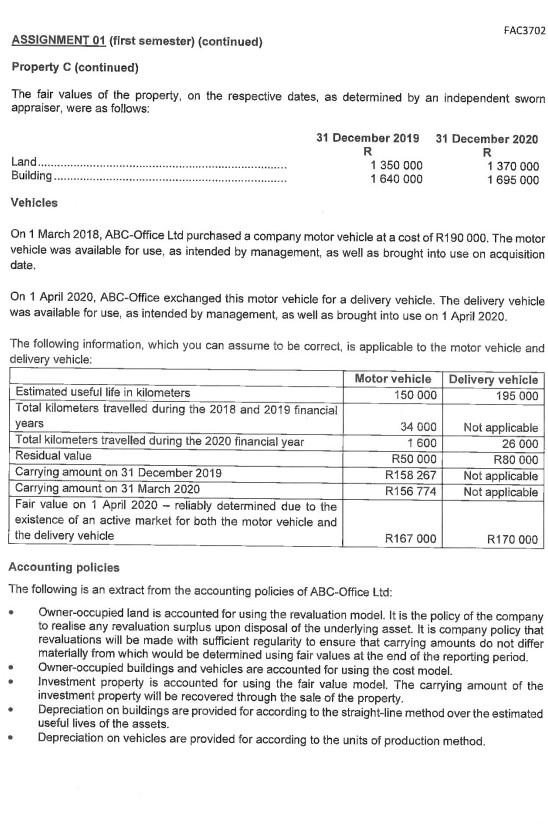

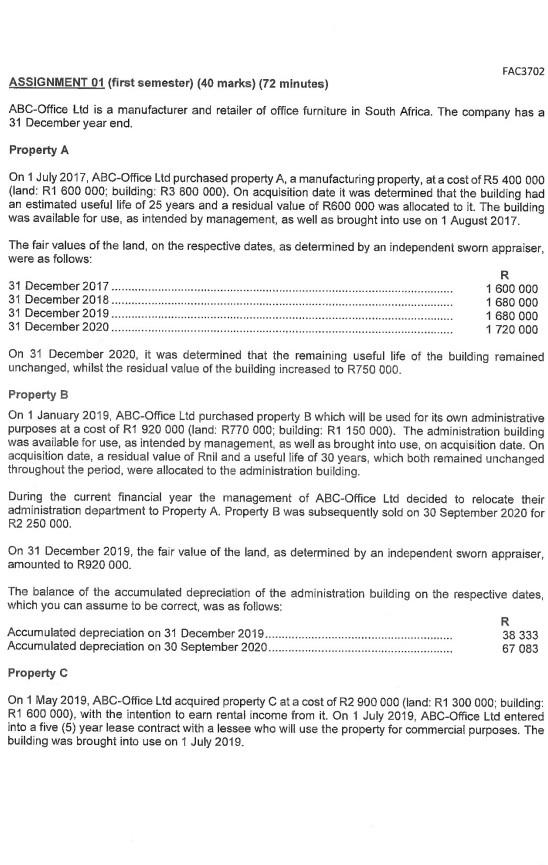

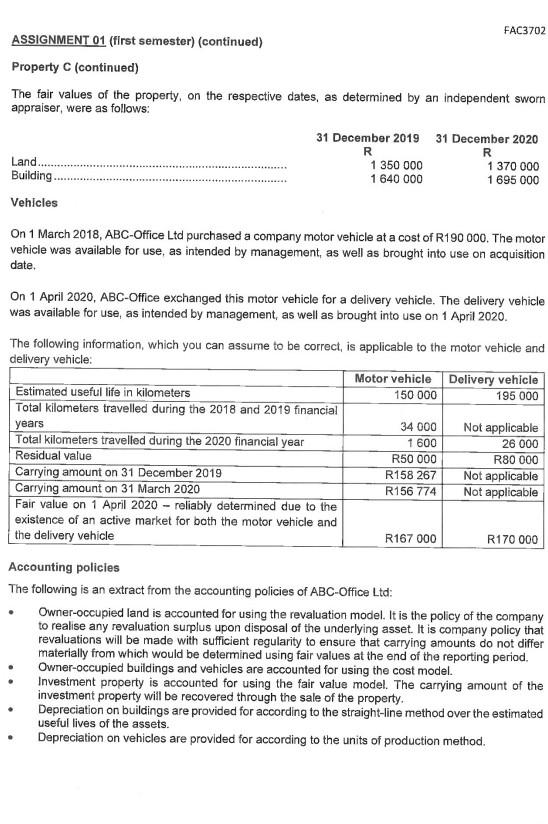

14:13 All FAC702 ASSIGNMENT $1 {first semester (40 marks) (72 minutes) ABC Office Lid sa manufacturer and retailer of office Furniture in South Africa. The

14:13 All FAC702 ASSIGNMENT $1 {first semester (40 marks) (72 minutes) ABC Office Lid sa manufacturer and retailer of office Furniture in South Africa. The company has a 31 December year end Property A On 1 Say 2017. ABC-Office Lid purchased property manufacturing property at a cost of Rs 400 000 fland R1 600 000 building: R3 800 000). On acquisition date was determined that the building had an estimated useful life of years and a residurivalue of R100 000 was allocated to it. The building was available for use, as intended by management as well as brought into use on 1 August 2017 The tar value of the land, on the respective dates, as determined by an independent sworn appraiser were as follows 31 December 2017 1 600 000 31 December 2010 1680 000 31 December 2010 1 680 000 31 December 2020 1 720 000 On 31 December 2020, was determined that the remaining sell We of the building remained unchanged whilst the residual value of the building increased to R750 000 Property B On 1 January 2019. ABC-Orice Lid purchased property which will be used for its own administrative purposes at a cost of R1 920 000 land: RT70 000, building Rt 150 000) The administration building was available for use as intended by management as well as brought into on acquisition date on acquisition date a residual value of Rnt and a useful We of 30 years, which both remained unchanged throughout the period wwe socited to the administration building During the current financial year the management of ABC-Office Lad decided to relocate thes administration department to Property A Property B was subsequently sold on 30 September 2020 for R2 250 000 On 31 December 2019. The fair value of the land, as determined by an independent swom appraiser amounted to R$20 000 The balance of the accumulated depreciation of the administration building on the respective dates which you can me to be corred, was as follows R Accumulated depreciation on 31 December 2019 38 333 Accumulated depreciation on 30 September 2020 67083 Property On 1 May 2019. ABC-Office Lid acquired property Cat a cost of R2 900 000 (and Rt 300 000, building R1 600 000), with the intention to eam rental income from it on 1 July 2019, ABC Office Lad entered nto a five (5) year late contract with a lessee who will use the property for commercial purposes. The building was brought to use on 1 Juy 2018 1 >> SIGNMENT 01 (rat semester (continued FAC3702 Property (continued The far values of the property, on the respective dates, as determined by an independent wor 31 December 2013 31 December 2020 Land 1 350 000 Bulding 1 840 000 Vehicles R 1 370 000 1 605 000 III O 14:13 ASSIGNMENT 81 (First semester (continued Property continued) The far values of the property, on the respective de determined by an independent om were as follow 31 December 2019 31 December 2020 R Land 1 350 000 Building 1370 000 1840 000 1 695 000 Vehicles years 1800 On March 2018, ABC-Office Lid purchased a company motor vehicle at a cost of R190 000. The motor vehicle was available for use an intended by management as well as brought into use on acquisition del On 1 Apel 2020. ABC-te exchanged this motor vehicle for a delivery vehicle. The delivery vehicle was available for use, as nended by management, m well as brought into use on 1 April 2020 The following information, which you can assume to be conect, is applicable to the motor vehicle and delivery vehicle Motor vehicle Delivery vehicle Estimated te in ometers 150 000 195 000 Total kilometers travelled Guring the 2016 and 2019 financial 34000 Not applicable Tot ameters traveled during the 2020 nacelea 26000 Residual value Re000 VO Carrying amount on 31 December 2010 R158 267 Not applicable Carrying amount on 31 March 2020 R156774 Not applicable Fair value on 1 April 2020-rably determined due to the existence of an active market for both the motor vehicle and the delivery vehicle R16 000 R170 000 Accounting policies The following is an extract from the accounting policies of ABC Orice Lad Owner- coupied land is accounted for using the evaluation model is the policy of the company to raise any revaluation surplus upon dispose of the underlying asset it is company policy that de window Owner-occupied buldngt and vehides to accounted for using the cost model The carrying out of the for according to the hedheted Depreciation on vehicles are provided for according to the units of production method. FAC3702 ASSIGNMENT 01 (first semester continued xation e South African normal tax rate is 28%. The capital gains tax indlusion rate is 80% The SA Revenue Service allows a 5 annual building allowance on all the buildings, according to section 1301) and 13quin of the Income Tax Act respectively, on the straightene methodno portioned for part of the year Deferred tax is provided for an altemporary differences in accordance with the statement of financial position approach. There are no other to causing comporary or exempt terences except those mentioned the question. The company will have suficient tacable profits and capital gains in future against which any unused taxes can be used Assumptions Land and buildings are regarded as separate classes of assets. Alamounts are material o 14:14 AO Revations will be made wins intreguany lo ensure we carrying amours do not offer materially from which would be determined using fair values at the end of the reporting period Owner-occupied buildings and vehicles are accounted for using the cost model Investment property is accounted for using their value model. The carrying amount of the investment property will be recovered through the sale of the property Depreciation on buildings are provided for according to the straighine metod over the estimated Useful lives of the late Depreciation on vehicles are provided for according to the units of production method FAC3702 ASSIGNMENT 01 (first semester) continued Taxation The South African normal tax rate is 28%. The capital gains tax inclusion rates 80% The SA Revenue Service aliowa 5% a building aliowance on the buildings, according to section 131 and 13quin of the Income Tax Act respectively on the straight line method, not apportioned for part of the year Deferred tax is provided for on all temporary terences in accordance win the statement of financial position approach. There we no other items causing tempowy or exempt diferences except those mentioned in the question. The company will have sufficient taxable profits and capital gains in future against which any used taxes can be used Assumptions Land and buildings are regarded as separate cases of assets Al amounts are material ignore the implications of Value Added Tax (VAT) REQUIRED Marks a) Prepare the relevant general journal entry in the accounting records of ABC Office 5 Lad to correctly account for the exchange of the motor vehicle on 1 April 2020. Prepare the following notes to the annual financial statements of ABC Office Lid for 35 the year ended 31 December 2000 Property, plant and equipment A total column is not required) Investment property Deferred tax (Only relating to the properties) Please note: Your answer must comply with the requirements of international Financial Reporting Standards (IFRS) Journal narrations are not required No abbreviations for general ledger account names may be used Accounting policy notes are not required Ignore comparative information Show al callations Round al amounts to the nearest Rand 1401 >> 30 = III o 2017, ABC-Office Ltd purchased property A, a manufacturing property, at a cost of 600 000; building: R3 800 000). On acquisition date it was determined that the ated useful life of 25 years and a residual value of R600 000 was allocated to it. lable for use, as intended by management, as well as brought into use on 1 Augus alues of the land, on the respective dates, as determined by an independent swor ollows: mber 2017 mber 2018 mber 2019 mber 2020 ecember 2020, it was determined that the remaining useful life of the buildin ed, whilst the residual value of the building increased to R750 000. -B uary 2019, ABC-Office Ltd purchased property B which will be used for its own ad at a cost of R1 920 000 (land: R770 000; building: R1 150 000). The administrat lable for use, as intended by management, as well as brought into use, on acquisiti n date, a residual value of Rnil and a useful life of 30 years, which both remained ut the period, were allocated to the administration building. he current financial year the management of ABC-Office Ltd decided to re ation department to Property A. Property B was subsequently sold on 30 Septem 00. ecember 2019, the fair value of the land, as determined by an independent swor d to R920 000. nce of the accumulated depreciation of the administration building on the respe u can assume to be correct, was as follows: ated depreciation on 31 December 2019. ated depreciation on 30 September 2020. 2019, ABC-Office Ltd acquired property C at a cost of R2 900 000 (land: R1 300 0 00), with the intention to earn rental income from it. On 1 July 2019, ABC-Office e (5) year lease contract with a lessee who will use the property for commercial pu was brought into use on 1 July 2019. MENT 01 (first semester) (continued) -C (continued) ENT 01 (first semester) (continued) -African normal tax rate is 28%. The capital gains tax inclusion rate is 80%. evenue Service allows a 5% annual building allowance on all the buildi. -(1) and 13quin of the Income Tax Act respectively, on the straight- d for part of the year. ex is provided for on all temporary differences in accordance with the state pproach. There are no other items causing temporary or exempt differen in the question. The company will have sufficient taxable profits and capi ich any unused tax losses can be utilised. ons and buildings are regarded as separate classes of assets. mounts are material. e the implications of Value-Added Tax (VAT) D: Dare the relevant general journal entry in the accounting records of ABC-C to correctly account for the exchange of the motor vehicle on 1 April 2020. Dare the following notes to the annual financial statements of ABC-Office Lt year ended 31 December 2020: Property, plant and equipment (A total column is not required) vestment property Deferred tax (Only relating to the properties) te: wer must comply with the requirements of International Financial Repa 5 (IFRS). arrations are not required. viations for general ledger account names may be used. ng policy notes are not required. mparative information. calculations. amounts to the nearest Rand. FAC3702 R ASSIGNMENT 01 (first semester) (40 marks) (72 minutes) ABC-Office Ltd is a manufacturer and retailer of office furniture in South Africa. The company has a 31 December year end Property A On 1 July 2017, ABC-Office Ltd purchased property A, a manufacturing property, at a cost of R5 400 000 (land: R1 600 000, building. R3 800 000). On acquisition date it was determined that the building had an estimated useful life of 25 years and a residual value of R600 000 was allocated to it. The building was available for use, as intended by management, as well as brought into use on 1 August 2017 The fair values of the land, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2017 1 600 000 31 December 2018 1 680 000 31 December 2019. 1 680 000 31 December 2020 1 720 000 On 31 December 2020, it was determined that the remaining useful life of the building remained unchanged, whilst the residual value of the building increased to R750 000. Property B On 1 January 2019, ABC-Office Ltd purchased property B which will be used for its own administrative purposes at a cost of R1 920 000 (and: R770 000; building: R1 150 000). The administration building was available for use, as intended by management, as well as brought into use, on acquisition date. On acquisition date, a residual value of Rnil and a useful life of 30 years, which both remained unchanged throughout the period, were allocated to the administration building, During the current financial year the management of ABC-Office Ltd decided to relocate their administration department to Property A. Property B was subsequently sold on 30 September 2020 for R2 250 000 On 31 December 2019, the fair value of the land, as determined by an independent sworn appraiser, amounted to R920 000 The balance of the accumulated depreciation of the administration building on the respective dates, which you can assume to be correct, was as follows: Accumulated depreciation on 31 December 2019. 38 333 Accumulated depreciation on 30 September 2020. 67 083 Property C On 1 May 2019, ABC-Office Ltd acquired property Cat a cost of R2 900 000 (land: R1 300 000, building: R1 600 000), with the intention to earn rental income from it. On 1 July 2019, ABC-Office Ltd entered into a five (5) year lease contract with a lessee who will use the property for commercial purposes. The building was brought into use on 1 July 2019. R FAC3702 ASSIGNMENT 01 (first semester) (continued) Property (continued) The fair values of the property, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2019 31 December 2020 R R Land. 1 350 000 1 370 000 Building 1 640 000 1 695 000 Vehicles On 1 March 2018, ABC-Office Ltd purchased a company motor vehicle at a cost of R190 000. The motor vehicle was available for use, as intended by management, as well as brought into use on acquisition date. On 1 April 2020, ABC-Office exchanged this motor vehicle for a delivery vehicle. The delivery vehicle was available for use, as intended by management, as well as brought into use on 1 April 2020. The following information, which you can assume to be correct, is applicable to the motor vehicle and delivery vehicle: Motor vehicle Delivery vehicle Estimated useful life in kilometers 150 000 195 000 Total kilometers travelled during the 2018 and 2019 financial years 34 000 Not applicable Total kilometers travelled during the 2020 financial year 1 600 26 000 Residual value R50 000 R80 000 Carrying amount on 31 December 2019 R158 267 Not applicable Carrying amount on 31 March 2020 R156 774 Not applicable Fair value on 1 April 2020 - reliably determined due to the existence of an active market for both the motor vehicle and the delivery vehicle R167 000 R170 000 Accounting policies The following is an extract from the accounting policies of ABC-Office Ltd: Owner-occupied land is accounted for using the revaluation model. It is the policy of the company to realise any revaluation surplus upon disposal of the underlying asset. It is company policy that revaluations will be made with sufficient regularity to ensure that carrying amounts do not differ materially from which would be determined using fair values at the end of the reporting period. Owner-occupied buildings and vehicles are accounted for using the cost model. Investment property is accounted for using the fair value model. The carrying amount of the investment property will be recovered through the sale of the property. Depreciation on buildings are provided for according to the straight-line method over the estimated useful lives of the assets. Depreciation on vehicles are provided for according to the units of production method. FAC3702 R ASSIGNMENT 01 (first semester) (40 marks) (72 minutes) ABC-Office Ltd is a manufacturer and retailer of office furniture in South Africa. The company has a 31 December year end Property A On 1 July 2017, ABC-Office Ltd purchased property A, a manufacturing property, at a cost of R5 400 000 (land: R1 600 000, building. R3 800 000). On acquisition date it was determined that the building had an estimated useful life of 25 years and a residual value of R600 000 was allocated to it. The building was available for use, as intended by management, as well as brought into use on 1 August 2017 The fair values of the land, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2017 1 600 000 31 December 2018 1 680 000 31 December 2019. 1 680 000 31 December 2020 1 720 000 On 31 December 2020, it was determined that the remaining useful life of the building remained unchanged, whilst the residual value of the building increased to R750 000. Property B On 1 January 2019, ABC-Office Ltd purchased property B which will be used for its own administrative purposes at a cost of R1 920 000 (and: R770 000; building: R1 150 000). The administration building was available for use, as intended by management, as well as brought into use, on acquisition date. On acquisition date, a residual value of Rnil and a useful life of 30 years, which both remained unchanged throughout the period, were allocated to the administration building, During the current financial year the management of ABC-Office Ltd decided to relocate their administration department to Property A. Property B was subsequently sold on 30 September 2020 for R2 250 000 On 31 December 2019, the fair value of the land, as determined by an independent sworn appraiser, amounted to R920 000 The balance of the accumulated depreciation of the administration building on the respective dates, which you can assume to be correct, was as follows: Accumulated depreciation on 31 December 2019. 38 333 Accumulated depreciation on 30 September 2020. 67 083 Property C On 1 May 2019, ABC-Office Ltd acquired property Cat a cost of R2 900 000 (land: R1 300 000, building: R1 600 000), with the intention to earn rental income from it. On 1 July 2019, ABC-Office Ltd entered into a five (5) year lease contract with a lessee who will use the property for commercial purposes. The building was brought into use on 1 July 2019. R FAC3702 ASSIGNMENT 01 (first semester) (continued) Property (continued) The fair values of the property, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2019 31 December 2020 R R Land. 1 350 000 1 370 000 Building 1 640 000 1 695 000 Vehicles On 1 March 2018, ABC-Office Ltd purchased a company motor vehicle at a cost of R190 000. The motor vehicle was available for use, as intended by management, as well as brought into use on acquisition date. On 1 April 2020, ABC-Office exchanged this motor vehicle for a delivery vehicle. The delivery vehicle was available for use, as intended by management, as well as brought into use on 1 April 2020. The following information, which you can assume to be correct, is applicable to the motor vehicle and delivery vehicle: Motor vehicle Delivery vehicle Estimated useful life in kilometers 150 000 195 000 Total kilometers travelled during the 2018 and 2019 financial years 34 000 Not applicable Total kilometers travelled during the 2020 financial year 1 600 26 000 Residual value R50 000 R80 000 Carrying amount on 31 December 2019 R158 267 Not applicable Carrying amount on 31 March 2020 R156 774 Not applicable Fair value on 1 April 2020 - reliably determined due to the existence of an active market for both the motor vehicle and the delivery vehicle R167 000 R170 000 Accounting policies The following is an extract from the accounting policies of ABC-Office Ltd: Owner-occupied land is accounted for using the revaluation model. It is the policy of the company to realise any revaluation surplus upon disposal of the underlying asset. It is company policy that revaluations will be made with sufficient regularity to ensure that carrying amounts do not differ materially from which would be determined using fair values at the end of the reporting period. Owner-occupied buildings and vehicles are accounted for using the cost model. Investment property is accounted for using the fair value model. The carrying amount of the investment property will be recovered through the sale of the property. Depreciation on buildings are provided for according to the straight-line method over the estimated useful lives of the assets. Depreciation on vehicles are provided for according to the units of production method. 14:13 All FAC702 ASSIGNMENT $1 {first semester (40 marks) (72 minutes) ABC Office Lid sa manufacturer and retailer of office Furniture in South Africa. The company has a 31 December year end Property A On 1 Say 2017. ABC-Office Lid purchased property manufacturing property at a cost of Rs 400 000 fland R1 600 000 building: R3 800 000). On acquisition date was determined that the building had an estimated useful life of years and a residurivalue of R100 000 was allocated to it. The building was available for use, as intended by management as well as brought into use on 1 August 2017 The tar value of the land, on the respective dates, as determined by an independent sworn appraiser were as follows 31 December 2017 1 600 000 31 December 2010 1680 000 31 December 2010 1 680 000 31 December 2020 1 720 000 On 31 December 2020, was determined that the remaining sell We of the building remained unchanged whilst the residual value of the building increased to R750 000 Property B On 1 January 2019. ABC-Orice Lid purchased property which will be used for its own administrative purposes at a cost of R1 920 000 land: RT70 000, building Rt 150 000) The administration building was available for use as intended by management as well as brought into on acquisition date on acquisition date a residual value of Rnt and a useful We of 30 years, which both remained unchanged throughout the period wwe socited to the administration building During the current financial year the management of ABC-Office Lad decided to relocate thes administration department to Property A Property B was subsequently sold on 30 September 2020 for R2 250 000 On 31 December 2019. The fair value of the land, as determined by an independent swom appraiser amounted to R$20 000 The balance of the accumulated depreciation of the administration building on the respective dates which you can me to be corred, was as follows R Accumulated depreciation on 31 December 2019 38 333 Accumulated depreciation on 30 September 2020 67083 Property On 1 May 2019. ABC-Office Lid acquired property Cat a cost of R2 900 000 (and Rt 300 000, building R1 600 000), with the intention to eam rental income from it on 1 July 2019, ABC Office Lad entered nto a five (5) year late contract with a lessee who will use the property for commercial purposes. The building was brought to use on 1 Juy 2018 1 >> SIGNMENT 01 (rat semester (continued FAC3702 Property (continued The far values of the property, on the respective dates, as determined by an independent wor 31 December 2013 31 December 2020 Land 1 350 000 Bulding 1 840 000 Vehicles R 1 370 000 1 605 000 III O 14:13 ASSIGNMENT 81 (First semester (continued Property continued) The far values of the property, on the respective de determined by an independent om were as follow 31 December 2019 31 December 2020 R Land 1 350 000 Building 1370 000 1840 000 1 695 000 Vehicles years 1800 On March 2018, ABC-Office Lid purchased a company motor vehicle at a cost of R190 000. The motor vehicle was available for use an intended by management as well as brought into use on acquisition del On 1 Apel 2020. ABC-te exchanged this motor vehicle for a delivery vehicle. The delivery vehicle was available for use, as nended by management, m well as brought into use on 1 April 2020 The following information, which you can assume to be conect, is applicable to the motor vehicle and delivery vehicle Motor vehicle Delivery vehicle Estimated te in ometers 150 000 195 000 Total kilometers travelled Guring the 2016 and 2019 financial 34000 Not applicable Tot ameters traveled during the 2020 nacelea 26000 Residual value Re000 VO Carrying amount on 31 December 2010 R158 267 Not applicable Carrying amount on 31 March 2020 R156774 Not applicable Fair value on 1 April 2020-rably determined due to the existence of an active market for both the motor vehicle and the delivery vehicle R16 000 R170 000 Accounting policies The following is an extract from the accounting policies of ABC Orice Lad Owner- coupied land is accounted for using the evaluation model is the policy of the company to raise any revaluation surplus upon dispose of the underlying asset it is company policy that de window Owner-occupied buldngt and vehides to accounted for using the cost model The carrying out of the for according to the hedheted Depreciation on vehicles are provided for according to the units of production method. FAC3702 ASSIGNMENT 01 (first semester continued xation e South African normal tax rate is 28%. The capital gains tax indlusion rate is 80% The SA Revenue Service allows a 5 annual building allowance on all the buildings, according to section 1301) and 13quin of the Income Tax Act respectively, on the straightene methodno portioned for part of the year Deferred tax is provided for an altemporary differences in accordance with the statement of financial position approach. There are no other to causing comporary or exempt terences except those mentioned the question. The company will have suficient tacable profits and capital gains in future against which any unused taxes can be used Assumptions Land and buildings are regarded as separate classes of assets. Alamounts are material o 14:14 AO Revations will be made wins intreguany lo ensure we carrying amours do not offer materially from which would be determined using fair values at the end of the reporting period Owner-occupied buildings and vehicles are accounted for using the cost model Investment property is accounted for using their value model. The carrying amount of the investment property will be recovered through the sale of the property Depreciation on buildings are provided for according to the straighine metod over the estimated Useful lives of the late Depreciation on vehicles are provided for according to the units of production method FAC3702 ASSIGNMENT 01 (first semester) continued Taxation The South African normal tax rate is 28%. The capital gains tax inclusion rates 80% The SA Revenue Service aliowa 5% a building aliowance on the buildings, according to section 131 and 13quin of the Income Tax Act respectively on the straight line method, not apportioned for part of the year Deferred tax is provided for on all temporary terences in accordance win the statement of financial position approach. There we no other items causing tempowy or exempt diferences except those mentioned in the question. The company will have sufficient taxable profits and capital gains in future against which any used taxes can be used Assumptions Land and buildings are regarded as separate cases of assets Al amounts are material ignore the implications of Value Added Tax (VAT) REQUIRED Marks a) Prepare the relevant general journal entry in the accounting records of ABC Office 5 Lad to correctly account for the exchange of the motor vehicle on 1 April 2020. Prepare the following notes to the annual financial statements of ABC Office Lid for 35 the year ended 31 December 2000 Property, plant and equipment A total column is not required) Investment property Deferred tax (Only relating to the properties) Please note: Your answer must comply with the requirements of international Financial Reporting Standards (IFRS) Journal narrations are not required No abbreviations for general ledger account names may be used Accounting policy notes are not required Ignore comparative information Show al callations Round al amounts to the nearest Rand 1401 >> 30 = III o 2017, ABC-Office Ltd purchased property A, a manufacturing property, at a cost of 600 000; building: R3 800 000). On acquisition date it was determined that the ated useful life of 25 years and a residual value of R600 000 was allocated to it. lable for use, as intended by management, as well as brought into use on 1 Augus alues of the land, on the respective dates, as determined by an independent swor ollows: mber 2017 mber 2018 mber 2019 mber 2020 ecember 2020, it was determined that the remaining useful life of the buildin ed, whilst the residual value of the building increased to R750 000. -B uary 2019, ABC-Office Ltd purchased property B which will be used for its own ad at a cost of R1 920 000 (land: R770 000; building: R1 150 000). The administrat lable for use, as intended by management, as well as brought into use, on acquisiti n date, a residual value of Rnil and a useful life of 30 years, which both remained ut the period, were allocated to the administration building. he current financial year the management of ABC-Office Ltd decided to re ation department to Property A. Property B was subsequently sold on 30 Septem 00. ecember 2019, the fair value of the land, as determined by an independent swor d to R920 000. nce of the accumulated depreciation of the administration building on the respe u can assume to be correct, was as follows: ated depreciation on 31 December 2019. ated depreciation on 30 September 2020. 2019, ABC-Office Ltd acquired property C at a cost of R2 900 000 (land: R1 300 0 00), with the intention to earn rental income from it. On 1 July 2019, ABC-Office e (5) year lease contract with a lessee who will use the property for commercial pu was brought into use on 1 July 2019. MENT 01 (first semester) (continued) -C (continued) ENT 01 (first semester) (continued) -African normal tax rate is 28%. The capital gains tax inclusion rate is 80%. evenue Service allows a 5% annual building allowance on all the buildi. -(1) and 13quin of the Income Tax Act respectively, on the straight- d for part of the year. ex is provided for on all temporary differences in accordance with the state pproach. There are no other items causing temporary or exempt differen in the question. The company will have sufficient taxable profits and capi ich any unused tax losses can be utilised. ons and buildings are regarded as separate classes of assets. mounts are material. e the implications of Value-Added Tax (VAT) D: Dare the relevant general journal entry in the accounting records of ABC-C to correctly account for the exchange of the motor vehicle on 1 April 2020. Dare the following notes to the annual financial statements of ABC-Office Lt year ended 31 December 2020: Property, plant and equipment (A total column is not required) vestment property Deferred tax (Only relating to the properties) te: wer must comply with the requirements of International Financial Repa 5 (IFRS). arrations are not required. viations for general ledger account names may be used. ng policy notes are not required. mparative information. calculations. amounts to the nearest Rand. FAC3702 R ASSIGNMENT 01 (first semester) (40 marks) (72 minutes) ABC-Office Ltd is a manufacturer and retailer of office furniture in South Africa. The company has a 31 December year end Property A On 1 July 2017, ABC-Office Ltd purchased property A, a manufacturing property, at a cost of R5 400 000 (land: R1 600 000, building. R3 800 000). On acquisition date it was determined that the building had an estimated useful life of 25 years and a residual value of R600 000 was allocated to it. The building was available for use, as intended by management, as well as brought into use on 1 August 2017 The fair values of the land, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2017 1 600 000 31 December 2018 1 680 000 31 December 2019. 1 680 000 31 December 2020 1 720 000 On 31 December 2020, it was determined that the remaining useful life of the building remained unchanged, whilst the residual value of the building increased to R750 000. Property B On 1 January 2019, ABC-Office Ltd purchased property B which will be used for its own administrative purposes at a cost of R1 920 000 (and: R770 000; building: R1 150 000). The administration building was available for use, as intended by management, as well as brought into use, on acquisition date. On acquisition date, a residual value of Rnil and a useful life of 30 years, which both remained unchanged throughout the period, were allocated to the administration building, During the current financial year the management of ABC-Office Ltd decided to relocate their administration department to Property A. Property B was subsequently sold on 30 September 2020 for R2 250 000 On 31 December 2019, the fair value of the land, as determined by an independent sworn appraiser, amounted to R920 000 The balance of the accumulated depreciation of the administration building on the respective dates, which you can assume to be correct, was as follows: Accumulated depreciation on 31 December 2019. 38 333 Accumulated depreciation on 30 September 2020. 67 083 Property C On 1 May 2019, ABC-Office Ltd acquired property Cat a cost of R2 900 000 (land: R1 300 000, building: R1 600 000), with the intention to earn rental income from it. On 1 July 2019, ABC-Office Ltd entered into a five (5) year lease contract with a lessee who will use the property for commercial purposes. The building was brought into use on 1 July 2019. R FAC3702 ASSIGNMENT 01 (first semester) (continued) Property (continued) The fair values of the property, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2019 31 December 2020 R R Land. 1 350 000 1 370 000 Building 1 640 000 1 695 000 Vehicles On 1 March 2018, ABC-Office Ltd purchased a company motor vehicle at a cost of R190 000. The motor vehicle was available for use, as intended by management, as well as brought into use on acquisition date. On 1 April 2020, ABC-Office exchanged this motor vehicle for a delivery vehicle. The delivery vehicle was available for use, as intended by management, as well as brought into use on 1 April 2020. The following information, which you can assume to be correct, is applicable to the motor vehicle and delivery vehicle: Motor vehicle Delivery vehicle Estimated useful life in kilometers 150 000 195 000 Total kilometers travelled during the 2018 and 2019 financial years 34 000 Not applicable Total kilometers travelled during the 2020 financial year 1 600 26 000 Residual value R50 000 R80 000 Carrying amount on 31 December 2019 R158 267 Not applicable Carrying amount on 31 March 2020 R156 774 Not applicable Fair value on 1 April 2020 - reliably determined due to the existence of an active market for both the motor vehicle and the delivery vehicle R167 000 R170 000 Accounting policies The following is an extract from the accounting policies of ABC-Office Ltd: Owner-occupied land is accounted for using the revaluation model. It is the policy of the company to realise any revaluation surplus upon disposal of the underlying asset. It is company policy that revaluations will be made with sufficient regularity to ensure that carrying amounts do not differ materially from which would be determined using fair values at the end of the reporting period. Owner-occupied buildings and vehicles are accounted for using the cost model. Investment property is accounted for using the fair value model. The carrying amount of the investment property will be recovered through the sale of the property. Depreciation on buildings are provided for according to the straight-line method over the estimated useful lives of the assets. Depreciation on vehicles are provided for according to the units of production method. FAC3702 R ASSIGNMENT 01 (first semester) (40 marks) (72 minutes) ABC-Office Ltd is a manufacturer and retailer of office furniture in South Africa. The company has a 31 December year end Property A On 1 July 2017, ABC-Office Ltd purchased property A, a manufacturing property, at a cost of R5 400 000 (land: R1 600 000, building. R3 800 000). On acquisition date it was determined that the building had an estimated useful life of 25 years and a residual value of R600 000 was allocated to it. The building was available for use, as intended by management, as well as brought into use on 1 August 2017 The fair values of the land, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2017 1 600 000 31 December 2018 1 680 000 31 December 2019. 1 680 000 31 December 2020 1 720 000 On 31 December 2020, it was determined that the remaining useful life of the building remained unchanged, whilst the residual value of the building increased to R750 000. Property B On 1 January 2019, ABC-Office Ltd purchased property B which will be used for its own administrative purposes at a cost of R1 920 000 (and: R770 000; building: R1 150 000). The administration building was available for use, as intended by management, as well as brought into use, on acquisition date. On acquisition date, a residual value of Rnil and a useful life of 30 years, which both remained unchanged throughout the period, were allocated to the administration building, During the current financial year the management of ABC-Office Ltd decided to relocate their administration department to Property A. Property B was subsequently sold on 30 September 2020 for R2 250 000 On 31 December 2019, the fair value of the land, as determined by an independent sworn appraiser, amounted to R920 000 The balance of the accumulated depreciation of the administration building on the respective dates, which you can assume to be correct, was as follows: Accumulated depreciation on 31 December 2019. 38 333 Accumulated depreciation on 30 September 2020. 67 083 Property C On 1 May 2019, ABC-Office Ltd acquired property Cat a cost of R2 900 000 (land: R1 300 000, building: R1 600 000), with the intention to earn rental income from it. On 1 July 2019, ABC-Office Ltd entered into a five (5) year lease contract with a lessee who will use the property for commercial purposes. The building was brought into use on 1 July 2019. R FAC3702 ASSIGNMENT 01 (first semester) (continued) Property (continued) The fair values of the property, on the respective dates, as determined by an independent sworn appraiser, were as follows: 31 December 2019 31 December 2020 R R Land. 1 350 000 1 370 000 Building 1 640 000 1 695 000 Vehicles On 1 March 2018, ABC-Office Ltd purchased a company motor vehicle at a cost of R190 000. The motor vehicle was available for use, as intended by management, as well as brought into use on acquisition date. On 1 April 2020, ABC-Office exchanged this motor vehicle for a delivery vehicle. The delivery vehicle was available for use, as intended by management, as well as brought into use on 1 April 2020. The following information, which you can assume to be correct, is applicable to the motor vehicle and delivery vehicle: Motor vehicle Delivery vehicle Estimated useful life in kilometers 150 000 195 000 Total kilometers travelled during the 2018 and 2019 financial years 34 000 Not applicable Total kilometers travelled during the 2020 financial year 1 600 26 000 Residual value R50 000 R80 000 Carrying amount on 31 December 2019 R158 267 Not applicable Carrying amount on 31 March 2020 R156 774 Not applicable Fair value on 1 April 2020 - reliably determined due to the existence of an active market for both the motor vehicle and the delivery vehicle R167 000 R170 000 Accounting policies The following is an extract from the accounting policies of ABC-Office Ltd: Owner-occupied land is accounted for using the revaluation model. It is the policy of the company to realise any revaluation surplus upon disposal of the underlying asset. It is company policy that revaluations will be made with sufficient regularity to ensure that carrying amounts do not differ materially from which would be determined using fair values at the end of the reporting period. Owner-occupied buildings and vehicles are accounted for using the cost model. Investment property is accounted for using the fair value model. The carrying amount of the investment property will be recovered through the sale of the property. Depreciation on buildings are provided for according to the straight-line method over the estimated useful lives of the assets. Depreciation on vehicles are provided for according to the units of production method

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting An Introduction To Concepts Methods And Uses

Authors: Sidney Davidson, Roman L. Weil, Clyde P. Stickney

2nd Edition

0030452961, 978-0030452963