Answered step by step

Verified Expert Solution

Question

1 Approved Answer

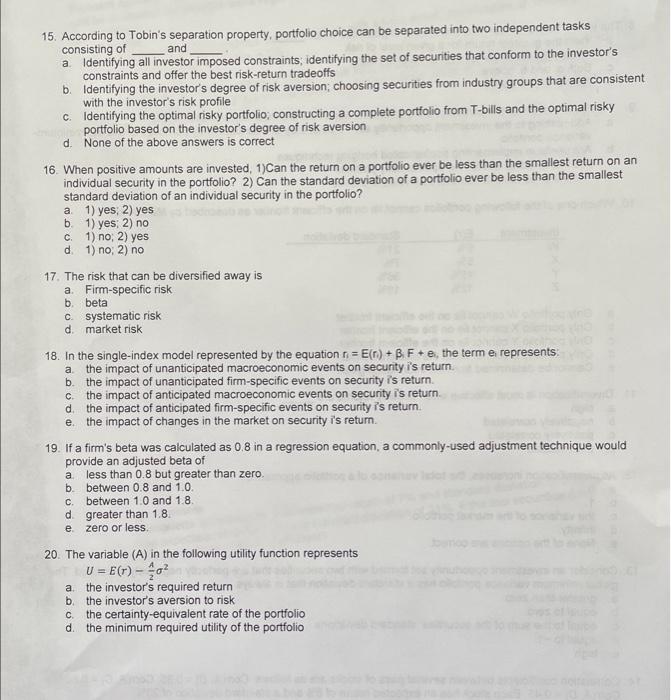

15. According to Tobin's separation property, portfolio choice can be separated into two independent tasks consisting of and a. Identifying all investor imposed constraints; identifying

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Million Air Exclusive Strategies For Pilots To Build Significant Wealth

Authors: Andy Garrison

1st Edition

1541383095, 978-1541383098