Answered step by step

Verified Expert Solution

Question

1 Approved Answer

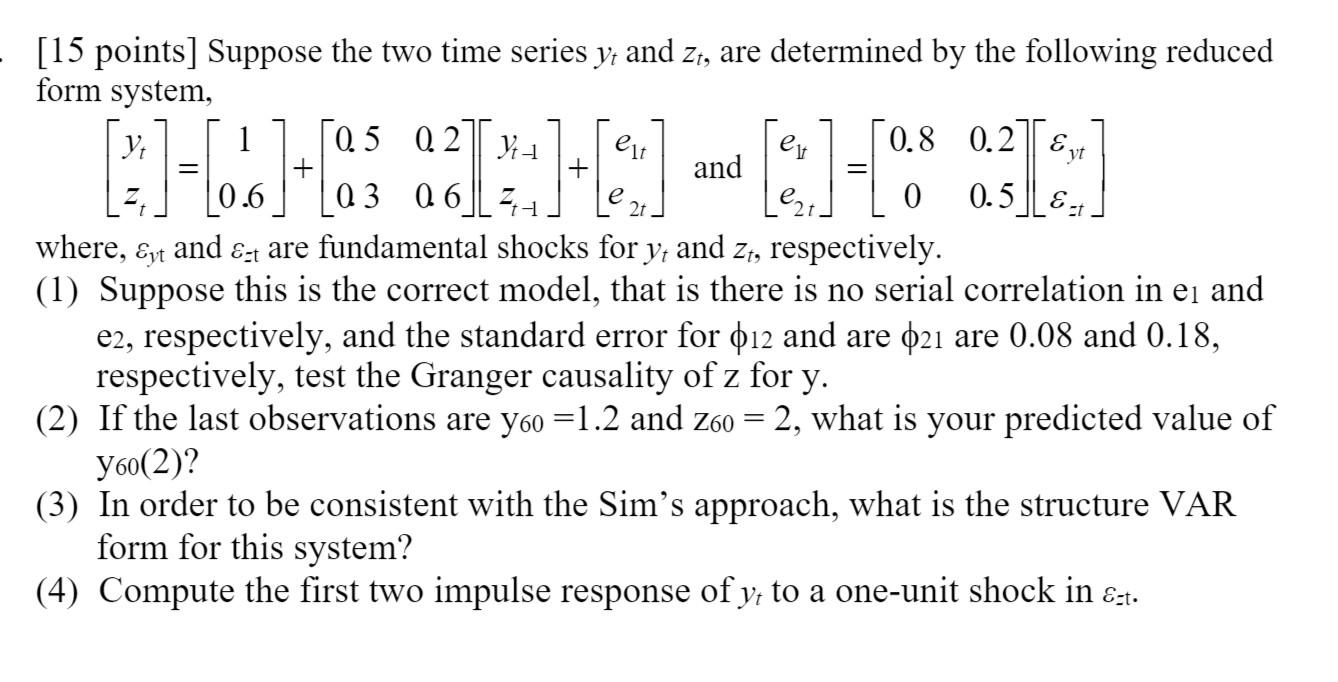

[15 points] Suppose the two time series y, and zt, are determined by the following reduced . form system, -- -) 1 0.5 0.2 1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Report Of The Follow Up International Conference On Financing For Development To Review The Implementation Of The Monterrey Consensus Doha Qatar 29 November 2 December 2008

Authors: United Nations

1st Edition

9211045940,9210558685