Answered step by step

Verified Expert Solution

Question

1 Approved Answer

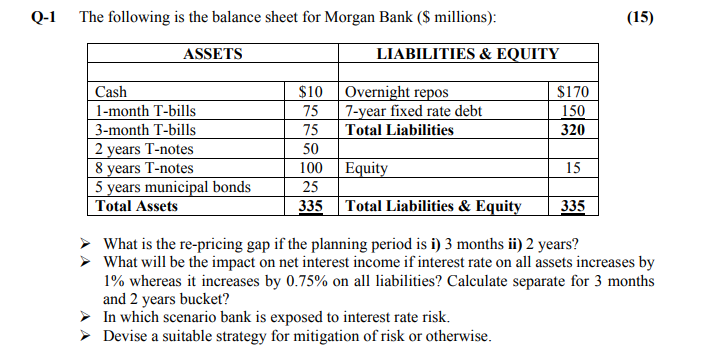

(15) Q-1 The following is the balance sheet for Morgan Bank ($ millions): ASSETS LIABILITIES & EQUITY $170 150 320 Cash 1-month T-bills 3-month T-bills

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

GAO Yellow Book Government Auditing Standar

Authors: Comptroller General United States Government

2011edition

1479245577, 978-1479245574