Answered step by step

Verified Expert Solution

Question

1 Approved Answer

16.a b. c. d. e. Suppose that your friend has decided to construct a portfolio that will contain stock X, stock Y, and the risk-free

16.a

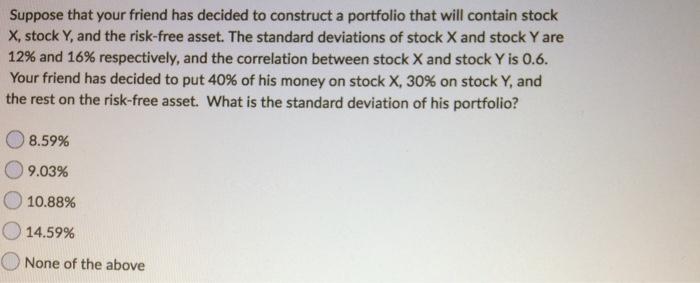

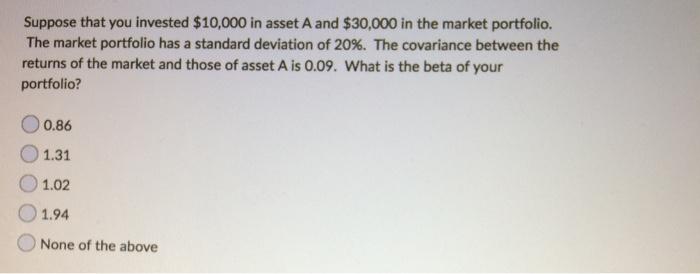

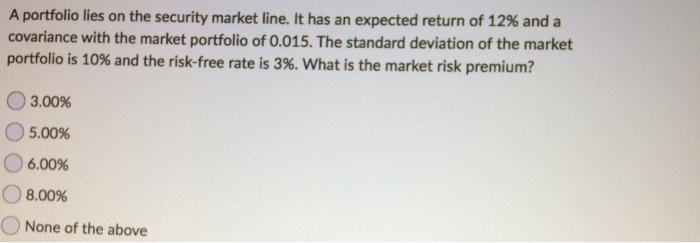

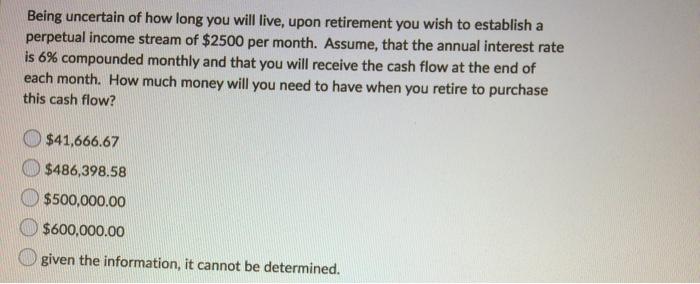

Suppose that your friend has decided to construct a portfolio that will contain stock X, stock Y, and the risk-free asset. The standard deviations of stock X and stock Y are 12% and 16% respectively, and the correlation between stock X and stock Y is 0.6. Your friend has decided to put 40% of his money on stock X, 30% on stock Y, and the rest on the risk-free asset. What is the standard deviation of his portfolio? 8.59% 9.03% 10.88% 14.59% None of the above Suppose that you invested $10,000 in asset A and $30,000 in the market portfolio. The market portfolio has a standard deviation of 20%. The covariance between the returns of the market and those of asset A is 0.09. What is the beta of your portfolio? 0.86 1.31 1.02 1.94 None of the above A portfolio lies on the security market line. It has an expected return of 12% and a covariance with the market portfolio of 0.015. The standard deviation of the market portfolio is 10% and the risk-free rate is 3%. What is the market risk premium? 3.00% 5.00% 6.00% 8.00% None of the above Being uncertain of how long you will live, upon retirement you wish to establish a perpetual income stream of $2500 per month. Assume, that the annual interest rate is 6% compounded monthly and that you will receive the cash flow at the end of each month. How much money will you need to have when you retire to purchase this cash flow? $41,666.67 $486,398.58 $500,000.00 $600,000.00 given the information, it cannot be determined. The Camel Company is considering two mutually exclusive projects with the following cash flows. Project A cash flow: Year 0 $-75; Year 1 $30; Year 2 $35; Year 3 $35. Project B cash flow: Year 0 $-60; Year 1 $25; Year 2 $30; Year 3 $25; What is the crossover rate (incremental IRR)? 13.94% 14.47% 15.44% 15.86% None of the above b.

c.

d.

e.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Belverd E Needles, Marian Powers

10th Edition

0547193289, 9780547193281