Answered step by step

Verified Expert Solution

Question

1 Approved Answer

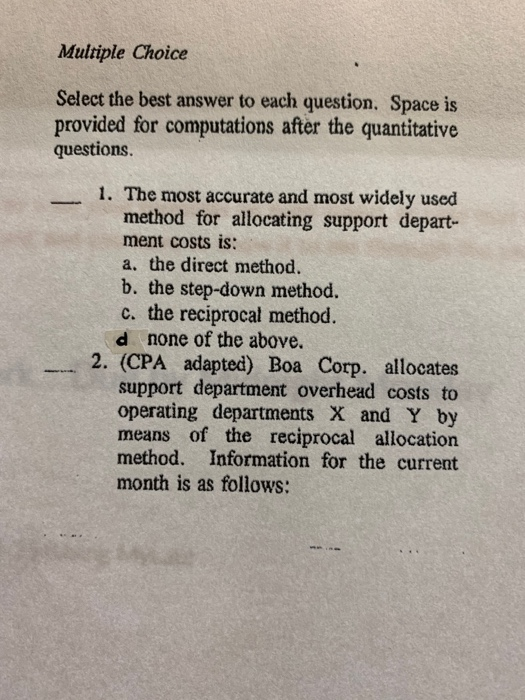

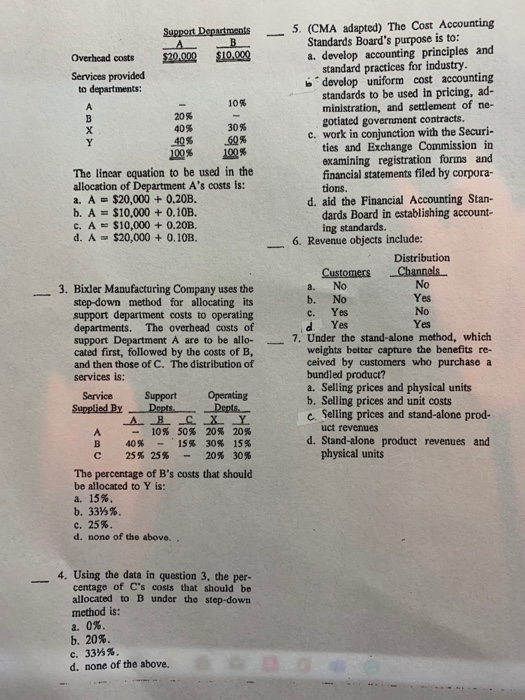

1-7 Multiple Choice Select the best answer to each question. Space is provided for computations after the quantitative questions. 1. The most accurate and most

1-7

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Accounting Volume 1 Financial Accounting

Authors: Mitchell Franklin, Patty Graybeal, Dixon Cooper, OpenStax

1st Edition

1593995946, 978-1593995942