Answered step by step

Verified Expert Solution

Question

1 Approved Answer

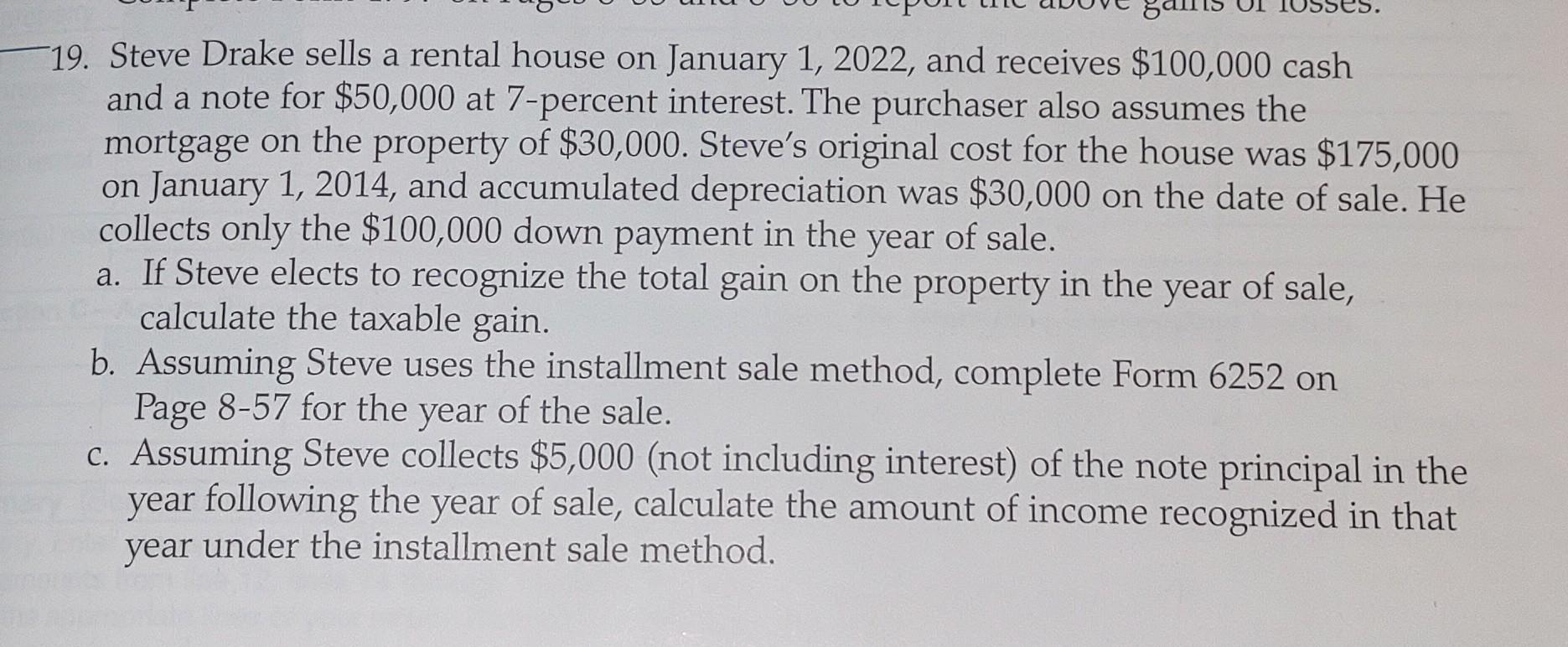

19. Steve Drake sells a rental house on January 1,2022 , and receives $100,000 cash and a note for $50,000 at 7-percent interest. The purchaser

19. Steve Drake sells a rental house on January 1,2022 , and receives $100,000 cash and a note for $50,000 at 7-percent interest. The purchaser also assumes the mortgage on the property of $30,000. Steve's original cost for the house was $175,000 on January 1, 2014, and accumulated depreciation was $30,000 on the date of sale. He collects only the $100,000 down payment in the year of sale. a. If Steve elects to recognize the total gain on the property in the year of sale, calculate the taxable gain. b. Assuming Steve uses the installment sale method, complete Form 6252 on Page 8-57 for the year of the sale. c. Assuming Steve collects $5,000 (not including interest) of the note principal in the year following the year of sale, calculate the amount of income recognized in that year under the installment sale method

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Essentials You Always Wanted To Know Self Learning Management Series

Authors: Vibrant Publishers , Kalpesh Ashar

5th Edition

1636510973, 978-1636510972