Answered step by step

Verified Expert Solution

Question

1 Approved Answer

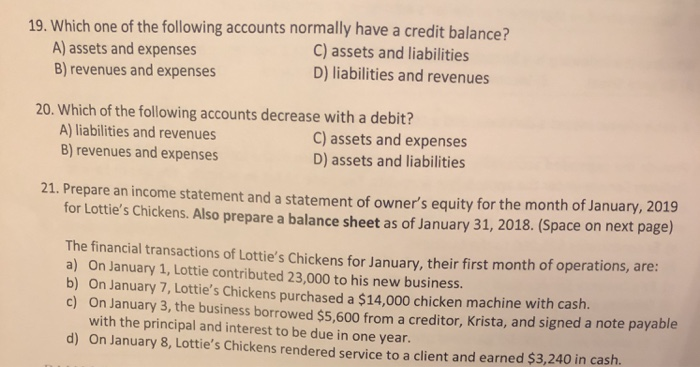

19. Which one of the following accounts normally have a credit balance? A) assets and expenses B) revenues and expenses C) assets and liabilities D)

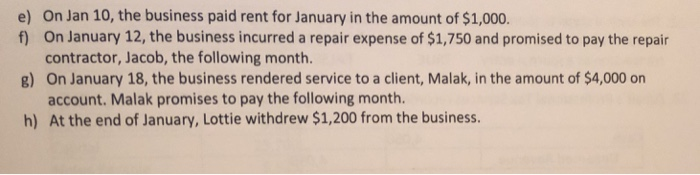

19. Which one of the following accounts normally have a credit balance? A) assets and expenses B) revenues and expenses C) assets and liabilities D) liabilities and revenues 20. Which of the following accounts decrease with a debit? A) liabilities and revenues C) assets and expenses D) assets and liabilities B) revenues and expenses 21. Prepare an income statement and a statement of owner's equity for the month of January, 2019 for Lottie's Chickens. Also prepare a balance sheet as of January 31, 2018. (Space on next page) The financial transactions of Lottie's Chickens for January, their first month of operations, are: a) On January 1, Lottie contributed 23,000 to his new business. b) On January 7, Lottie's Chickens purchased a $14,000 chicken machine with cash. c) On January 3, the business borrowed $5,600 from a creditor, Krista, and signed a note payable with the principal and interest to be due in one year d) On January 8, Lottie's Chickens rendered service to a client and earned $3,240 in cash. e) On Jan 10, the business paid rent for January in the amount of $1,000. f) On January 12, the business incurred a repair expense of $1,750 and promised to pay the repair g) h) contractor, Jacob, the following month. On January 18, the business rendered service to a client, Malak, in the amount of $4,000 on account. Malak promises to pay the following month. At the end of January, Lottie withdrew $1,200 from the business

19. Which one of the following accounts normally have a credit balance? A) assets and expenses B) revenues and expenses C) assets and liabilities D) liabilities and revenues 20. Which of the following accounts decrease with a debit? A) liabilities and revenues C) assets and expenses D) assets and liabilities B) revenues and expenses 21. Prepare an income statement and a statement of owner's equity for the month of January, 2019 for Lottie's Chickens. Also prepare a balance sheet as of January 31, 2018. (Space on next page) The financial transactions of Lottie's Chickens for January, their first month of operations, are: a) On January 1, Lottie contributed 23,000 to his new business. b) On January 7, Lottie's Chickens purchased a $14,000 chicken machine with cash. c) On January 3, the business borrowed $5,600 from a creditor, Krista, and signed a note payable with the principal and interest to be due in one year d) On January 8, Lottie's Chickens rendered service to a client and earned $3,240 in cash. e) On Jan 10, the business paid rent for January in the amount of $1,000. f) On January 12, the business incurred a repair expense of $1,750 and promised to pay the repair g) h) contractor, Jacob, the following month. On January 18, the business rendered service to a client, Malak, in the amount of $4,000 on account. Malak promises to pay the following month. At the end of January, Lottie withdrew $1,200 from the business

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamental Financial Accounting Concepts

Authors: J.K.

7th Edition

B003NPRW7I