Question

1.Beta is a measure of systematic risk. A beta of 1 implies that a stock is as risky as the overall market, a beta higher

1.Beta is a measure of systematic risk. A beta of 1 implies that a stock is as risky as the overall market, a beta higher than one is that the stock is riskier than the market, while beta less than one implies it is less riskier than the market. Use information outside the case to understand more about beta. Can you explain which would have a higher beta -- full service or limited service restaurants? Why?

2.At what point do you think the bankruptcy costs will outweigh the interest tax shield? Why?

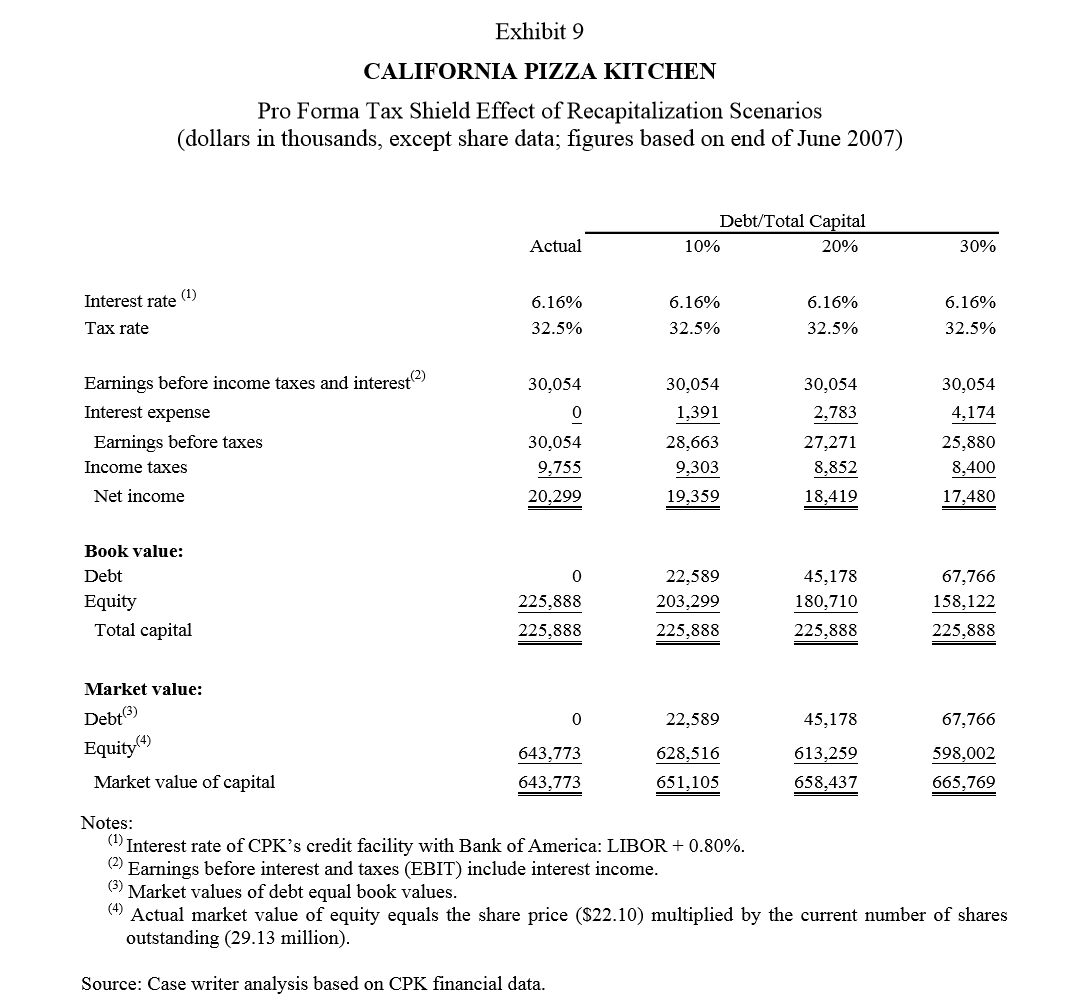

3.Why is it assumed that CPK will receive interest on loan at LIBOR+0.80% (exhibit 9)?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Selected Works Of George J. Benston Banking And Financial Services Volume 1

Authors: James D. Rosenfeld

1st Edition

0195389018, 0199745471, 9780199745470