Answered step by step

Verified Expert Solution

Question

1 Approved Answer

1D. 5 points. One year ago, you signed a forward contract in which you agreed to buy 17,255 British pounds today at a price of

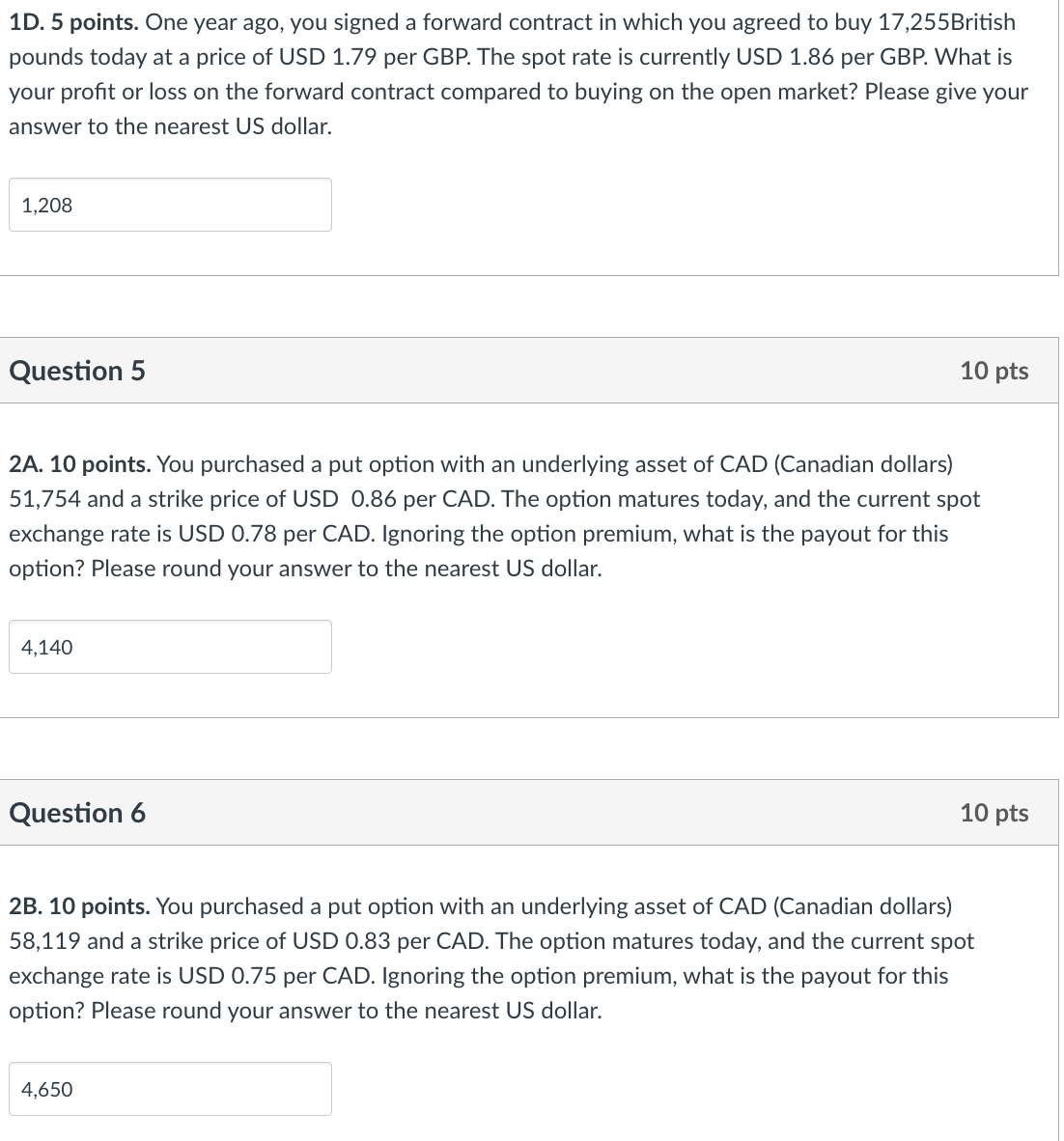

1D. 5 points. One year ago, you signed a forward contract in which you agreed to buy 17,255 British pounds today at a price of USD 1.79 per GBP. The spot rate is currently USD 1.86 per GBP. What is your profit or loss on the forward contract compared to buying on the open market? Please give your answer to the nearest US dollar. Question 5 10 pts 2A. 10 points. You purchased a put option with an underlying asset of CAD (Canadian dollars) 51,754 and a strike price of USD 0.86 per CAD. The option matures today, and the current spot exchange rate is USD 0.78 per CAD. Ignoring the option premium, what is the payout for this option? Please round your answer to the nearest US dollar. Question 6 10 pts 2B. 10 points. You purchased a put option with an underlying asset of CAD (Canadian dollars) 58,119 and a strike price of USD 0.83 per CAD. The option matures today, and the current spot exchange rate is USD 0.75 per CAD. Ignoring the option premium, what is the payout for this option? Please round your answer to the nearest US dollar

1D. 5 points. One year ago, you signed a forward contract in which you agreed to buy 17,255 British pounds today at a price of USD 1.79 per GBP. The spot rate is currently USD 1.86 per GBP. What is your profit or loss on the forward contract compared to buying on the open market? Please give your answer to the nearest US dollar. Question 5 10 pts 2A. 10 points. You purchased a put option with an underlying asset of CAD (Canadian dollars) 51,754 and a strike price of USD 0.86 per CAD. The option matures today, and the current spot exchange rate is USD 0.78 per CAD. Ignoring the option premium, what is the payout for this option? Please round your answer to the nearest US dollar. Question 6 10 pts 2B. 10 points. You purchased a put option with an underlying asset of CAD (Canadian dollars) 58,119 and a strike price of USD 0.83 per CAD. The option matures today, and the current spot exchange rate is USD 0.75 per CAD. Ignoring the option premium, what is the payout for this option? Please round your answer to the nearest US dollar Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Optimization Methods In Finance

Authors: Gerard Cornuejols, Reha Tütüncü

1st Edition

0521861705, 978-0521861700