Question

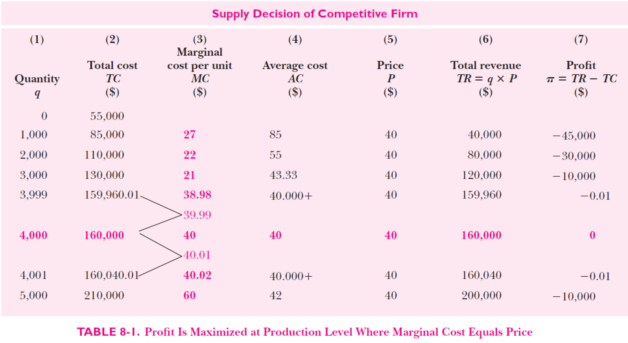

1.Examine the cost data shown in Table 8-1 above . Calculate the supply decision of a profit-maximizing competitive firm when price is $21, $40, and

1.Examine the cost data shown in Table 8-1 above . Calculate the supply decision of a profit-maximizing competitive firm when price is $21, $40, and $60. What would the level of total profit be for each of the three prices?

What would happen to the exit or entry of identical firms in the long run at each of the three prices?

2.Using the cost data shown in Table 8-1 above, calculate the price elasticity of supply between P = 40 and P = 40.02 for the individual firm. Assume that there are 2000 identical firms, and construct a table showing the industry supply schedule. What is the industry price elasticity of supply between P = 40 and P = 40.02?

3.Banana Computer Company has fixed costs of production of $100,000, while each unit costs $600 of labor and $400 of materials and fuel. At a price of $3000, consumers would buy no Banana computers, but for each $10 reduction in price, sales of Banana computers increase by 1000 units. Calculate marginal cost and marginal revenue for Banana Computer, and determine its monopoly price and quantity.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Economics

Authors: Robert H. Frank, Ben Bernanke Professor, Kate Antonovics, Ori Heffetz

6th Edition

0078021855, 9780078021855