Answered step by step

Verified Expert Solution

Question

1 Approved Answer

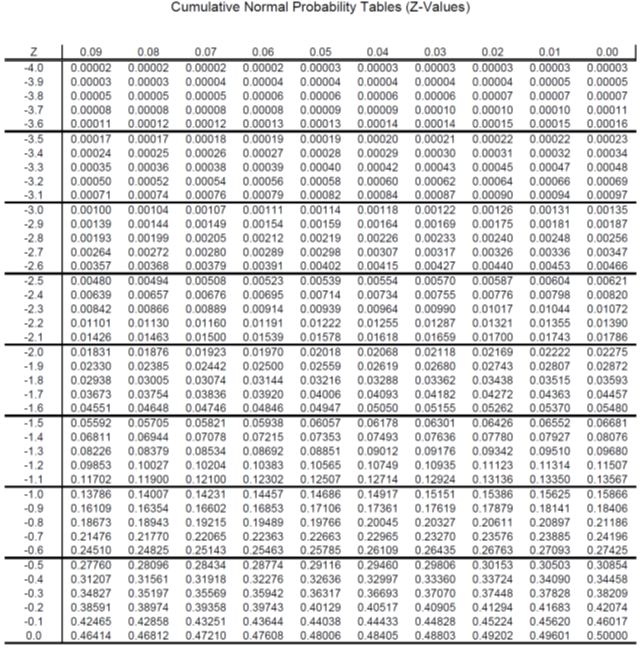

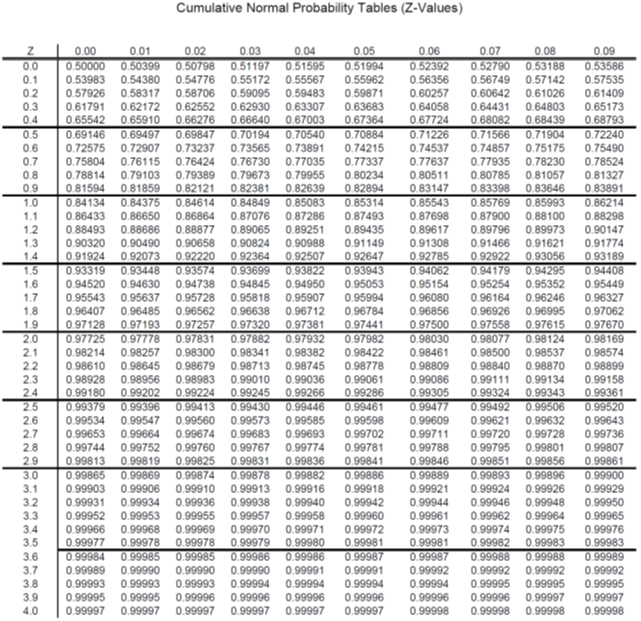

1-The shares of ABC company are currently priced at 4.15. Call options on ABC stocks currently have an exercise price of 4 that expire in

- 1-The shares of ABC company are currently priced at 4.15. Call options on ABC stocks currently have an exercise price of 4 that expire in 3-months time. The prevailing risk free interest rate is 5%, and the volatility of the stock price is 0.22.

- What is the price of a call option on ABC stock under the Black-Scholes-Merton pricing model?

- What is the price of a put option on ABC stock, given a strike price of 4 and expiry date 3-months hence?

- Assuming that you held 50,000 stocks for ABC. How would you construct a delta neutral hedge using ABC calls?

-

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptoassets The Innovative Investors Guide To Bitcoin And Beyond

Authors: Chris Burniske ,Jack Tatar

1st Edition

1260026671, 126002668X, 9781260026672, 9781260026689