Question

1.Which statement is incorrect? a. When shares are issued for services received, the measure is equal to fair value of such services or the fair

1.Which statement is incorrect?

a. When shares are issued for services received, the measure is equal to fair value of such services or the fair value of shares issued, whichever is more clearly determinable.

b. Shares issued for noncash asset shall be measured first at fair market value of noncash asset received

c. In the absence of any evidence to the contrary, subscriptions receivable is to be presented as current asset.

d. Contributed capital includes the entire amount related to issuance and subscription of shares regardless of whether the shares are par value or no par value.

e. none of the above

2.Which statement is correct?

a. When preference shares and ordinary shares are issued at a single price and both shares have fair value, both shares shall receive allocation equal to their respective fair values.

b. Preference shares which are redeemable 2 years from the financial statements date shall be presented under noncurrent liability rather than shareholders' equity.

c. When Preference shares are converted into bonds, the issuing company shall charge retained earnings for the excess of issue price of preference shares over the face value of the bonds.

d. Preference shares is a better investment than ordinary shares since they offer priority in terms of income and asset distribution and yields greater returns when the corporation is performing very well.

e. all of the above

3.Which statement is incorrect?

a. On repurchase of treasury shares, no gain or loss is recognized. The purchase price would become the cost of treasury shares.

b. On reissuance of treasury shares, the difference between the cost and reissue price of treasury shares is debited or credited to share premium rather than to profit or loss.

c. If treasury shares are retired above par, the difference between the cost and the par value is automatically charged to retained earnings.

d. Treasury shares can be subjected to share split and can be re-issued as share dividends.

e. none of the above

4.Which statement is incorrect?

a. When ABC Co. Issued share warrants, without receiving any consideration, to its shareholders, for them to acquire ABC Co. unissued shares within a specified time at a specified price, there is no need for ABC Co. to make a journal entry.

b. ABC Co. issued at a single price, preference shares with detachable warrants to purchase ordinary shares. If only the preference shares have a fair value at that date, ABC Co. must not credit any amount to the share warrants.

c. Expiration of share warrants previously issued with bonds or preference shares at a lump sum price, will not affect the total shareholders' equity.

d. Share warrants outstanding account shall be reported as share premium to be included under shareholders' equity.

e. none of the above

5.Which statement is incorrect?

a. Dividends out of retained earnings is limited to the balance of unappropriated retained earnings, except for share dividends.

b. Cash dividends are paid on the basis of the number of shares issued less the number of treasury shares.

c. Property dividends payable shall be measured based on fair value of the property on the date of declaration, reporting and distribution.

d. All kinds of dividends not yet paid shall be presented under the liability section of the statement of financial position.

e. none of the above

6.Which statement is incorrect?

a. When a dividend is declared and paid in shares of stock, total shareholders' equity does not change.

b. Retained earnings is capitalized in a share dividend.

c. When treasury shares are reissued as dividends, accumulated profits is charged an amount equal to the cost of treasury shares.

d. In closely held entities, if share dividends are declared, accumulated profits shall be capitalized at par or stated value of the shares.

e. none of the above

7.How many of the transactions below does not affect the balance of accumulated profits? I. share split II. appropriation for plant expansion III. conversion of preference shares to ordinary shares where the original issue price of preference shares is greater than the aggregate par value of ordinary shares. IV. Retirement of treasury shares below par value

a. 0

b. 1

c. 2

d. 3

e. 4

8.What does appropriation of retained earnings (R/E) and declaration of cash dividend have in common?

a. both increase the amount of appropriated R/E

b. both have the same consequences for shareholders

c. both result in a decrease in unappropriated R/E

d. both permanently reduce future ability to pay dividends

e. none of the above

9.Which statement is correct?

a. The primary purpose of quasi reorganization is to give an entity the opportunity to eliminate a deficit in accumulated profits.

b. Quasi reorganization thru revaluation does not change the share capital of the organization and the deficit is eliminated thru the use of revaluation surplus.

c. Quasi reorganization thru recapitalization changes the share capital structure of the organization and the deficit is eliminated thru the use of share premium.

d. all of the above

e. none of the above

10.Which statement is incorrect?

a. Share options are equity settled share based payment transaction and should be reported as expense using the fair value method on the date of grant.

b. Compensation expense is immediately recognized under PFRS 2 in circumstances when options are granted for prior service, and the options are immediately exercisable

c. In share-based compensation, the entry to record the compensation expense is a debit to salaries expense and a credit to Share Options Outstanding.

d. none of the above

11.In share-based compensation, who shall be included in determining total compensation expense?

a. Employees who left the company during the period

b. Employees who will leave the company for the succeeding years

c. Employees who already retired during the period of computation

d. Employees who are hired during the period of computation

e. answer not given

12.Which statement is correct?

a. Defined contribution plan is a benefit plan in which an entity pays a fixed contribution into a separate fund and will have no legal or constructive obligation to pay further contribution if the fund becomes insufficient to pay employee benefits.

b. Actuarial assumptions are the entity's best estimates of the variables that will determine the ultimate cost of providing postemployment benefits.

c. In a defined benefit plan, if the fair value of plan assets is more than the projected benefit obligation, the plan is overfunded and there is prepaid benefit cost.

d. A and B

e. A, B and C

13.S1: If the actual return on plan assets is greater than the expected return, there is actuarial gain. S2: A decrease in projected benefit obligation is actuarial gain.

a. both are true

b. both are false

c. S1 is true

d. S2 is true

14.Which statement is incorrect?

a. PFRS mandates the use of projected unit credit method of determining the present value of the defined benefit obligation.

b. The discount rate used in making actuarial assumptions shall be determined by reference to the market yield on high quality bonds at the end of reporting period.

c. Current service cost is the increase in the present value of the defined benefit obligation resulting from employee service in the previous period.

d. In accounting for other long-term employee benefits, Current service cost, past service cost and any gain or loss on settlement are fully recognized through profit or loss.

e. none of the above

15.Which statement is incorrect?

a. The "amortized cost" of bonds payable means Face amount plus premium on bonds payable, minus discount on bonds payable and minus bond issue cost.

b. For a bond issue which sells for less than its face value, the market rate of interest is higher than the rate stated on the bond.

c. Under the effective interest method, interest expense is equal to carrying amount of bonds multiplied by effective interest rate.

d. Amortization of discount on bonds payable would increase the carrying amount of bond and decrease the net income of bond issuer.

e. none of the above

16.Which statement is incorrect?

a. For a liability to exist a past transaction or event must have occurred.

b. Current liabilities are normally recorded at the amount expected to be paid rather than at present value according to the concept of matching principle.

c. A long-term debt maturing currently which is refinanced on a long-term basis after the reporting period but before issuance of the financial statements, shall be classified as current liability.

d. none of the above

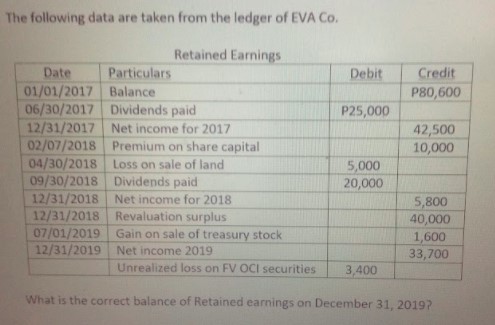

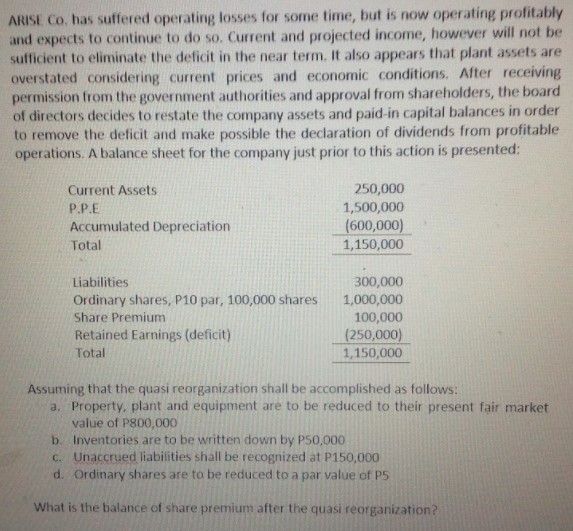

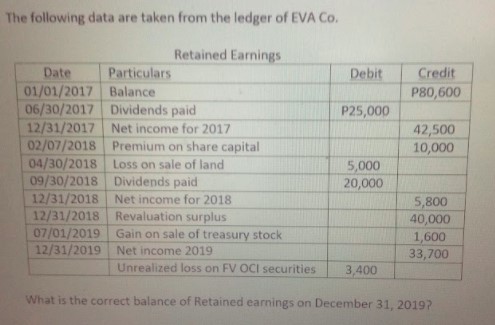

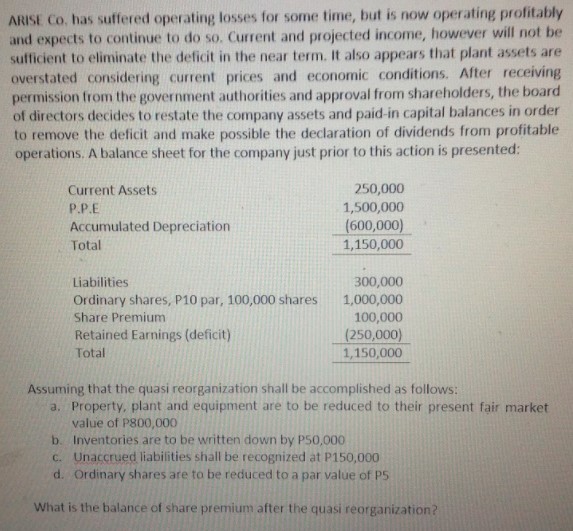

Problems (need solutions)

1.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: LibbyShort

7th Edition

78111021, 978-0078111020