Answered step by step

Verified Expert Solution

Question

1 Approved Answer

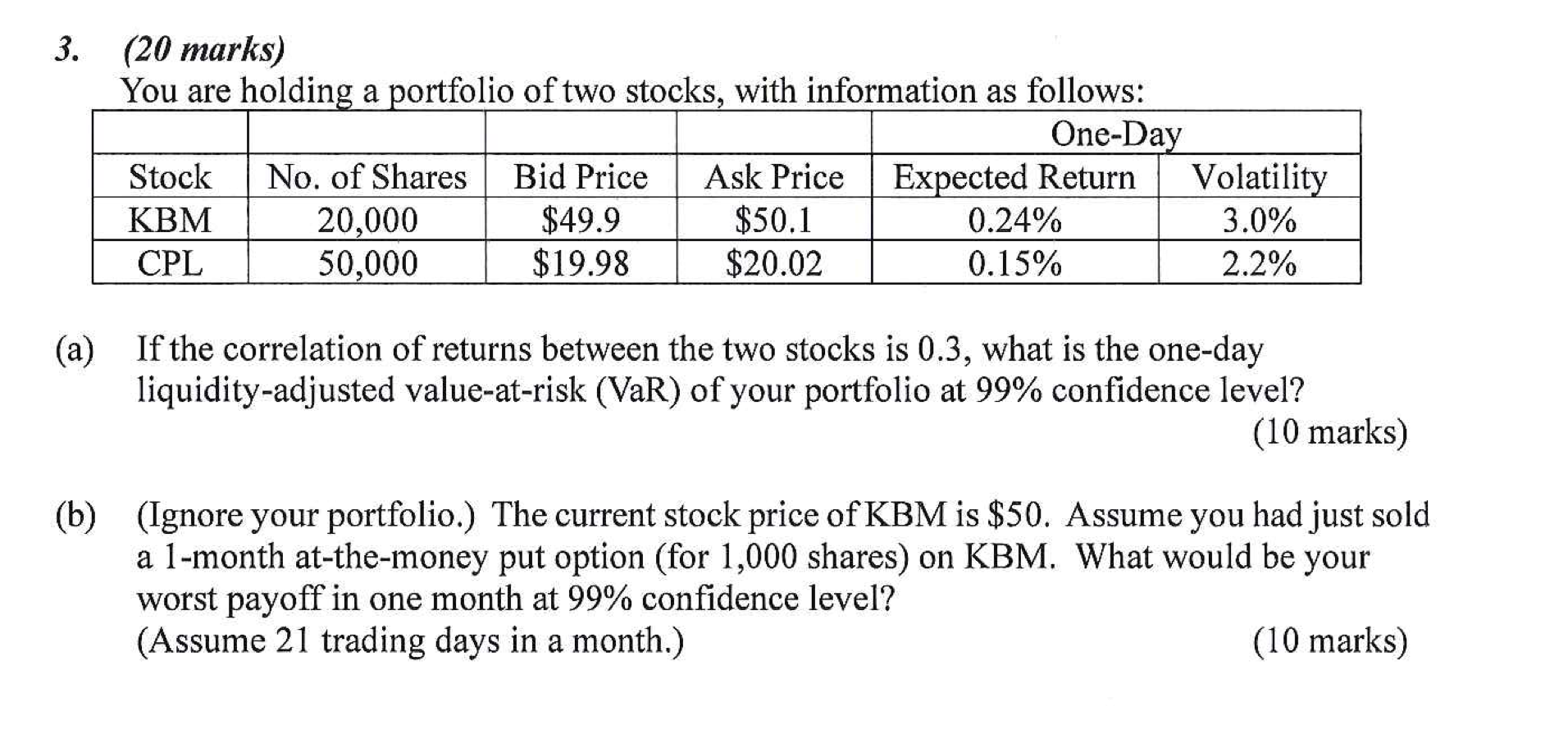

( 2 0 marks ) You are holding a portfolio of two stocks, with information as follows: ( a ) If the correlation of returns

marks

You are holding a portfolio of two stocks, with information as follows:

a If the correlation of returns between the two stocks is what is the oneday

liquidityadjusted valueatrisk VaR of your portfolio at confidence level?

marks

bIgnore your portfolio. The current stock price of KBM is $ Assume you had just sold

a month atthemoney put option for shares on KBM What would be your

worst payoff in one month at confidence level?

Assume trading days in a month.

marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Supply Chain Finance Solutions

Authors: Erik Hofmann, Oliver Belin

1st Edition

3642175651, 978-3642175657