Answered step by step

Verified Expert Solution

Question

1 Approved Answer

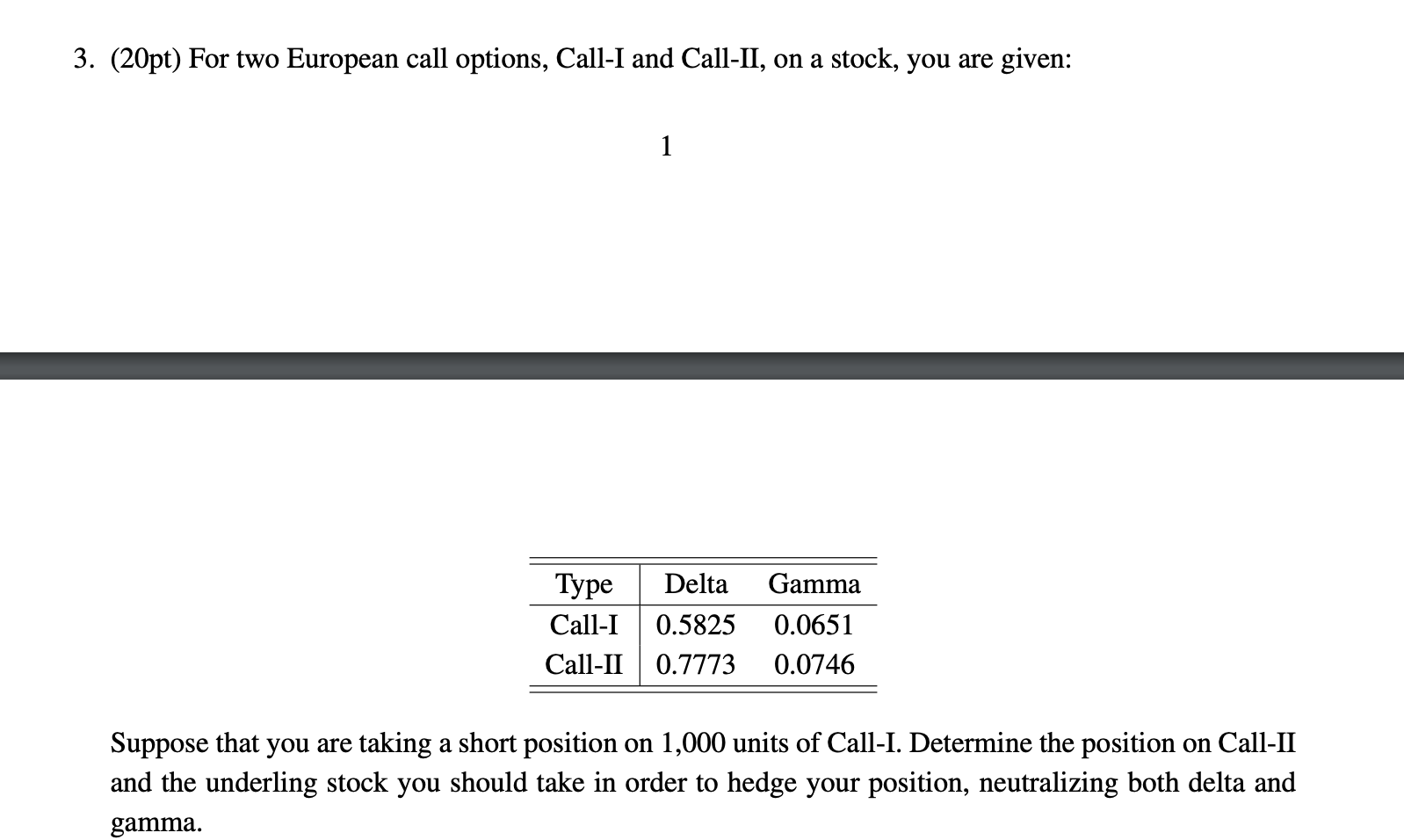

( 2 0 pt ) For two European call options, Call - I and Call - II , on a stock, you are given: 1

pt For two European call options, CallI and CallII on a stock, you are given:

Suppose that you are taking a short position on units of CallI. Determine the position on CallII

and the underling stock you should take in order to hedge your position, neutralizing both delta and

gamma.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Estate Finance And Investments

Authors: William Brueggeman, Jeffrey Fisher

13th Edition

0073524719, 9780073524719