Answered step by step

Verified Expert Solution

Question

1 Approved Answer

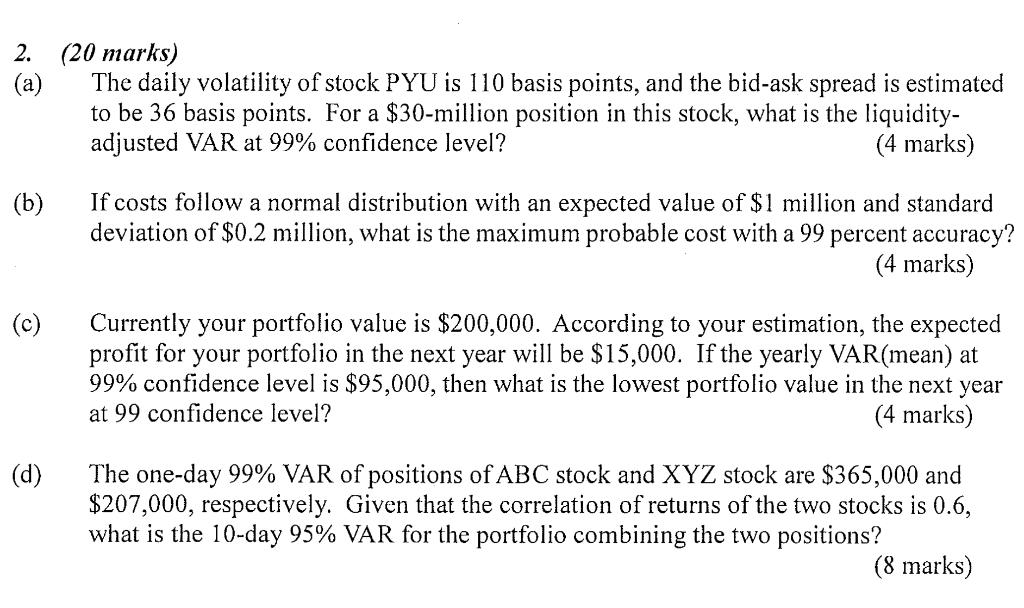

2. (20 marks) (a) (b) If costs follow a normal distribution with an expected value of $1 million and standard deviation of $0.2 million,

2. (20 marks) (a) (b) If costs follow a normal distribution with an expected value of $1 million and standard deviation of $0.2 million, what is the maximum probable cost with a 99 percent accuracy? (4 marks) (c) The daily volatility of stock PYU is 110 basis points, and the bid-ask spread is estimated to be 36 basis points. For a $30-million position in this stock, what is the liquidity- adjusted VAR at 99% confidence level? (4 marks) (d) Currently your portfolio value is $200,000. According to your estimation, the expected profit for your portfolio in the next year will be $15,000. If the yearly VAR(mean) at 99% confidence level is $95,000, then what is the lowest portfolio value in the next year at 99 confidence level? (4 marks) The one-day 99% VAR of positions of ABC stock and XYZ stock are $365,000 and $207,000, respectively. Given that the correlation of returns of the two stocks is 0.6, what is the 10-day 95% VAR for the portfolio combining the two positions? (8 marks)

Step by Step Solution

★★★★★

3.34 Rating (163 Votes )

There are 3 Steps involved in it

Step: 1

a The liquidityadjusted VAR at 99 confidence level is calculated using the formula VAR daily volatil...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Contemporary Financial Management

Authors: James R Mcguigan, R Charles Moyer, William J Kretlow

10th Edition

978-0324289114, 0324289111