Answered step by step

Verified Expert Solution

Question

1 Approved Answer

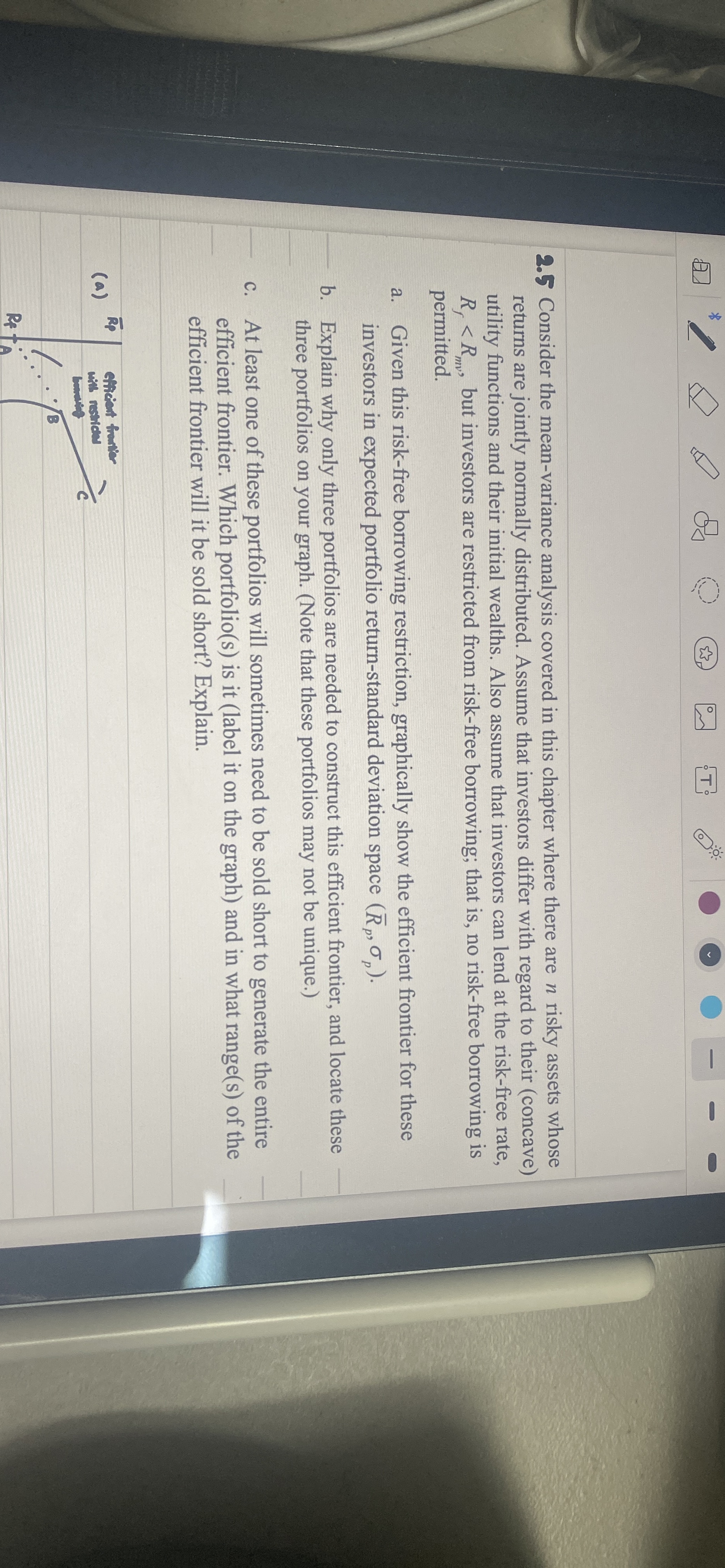

2 . 5 Consider the mean - variance analysis covered in this chapter where there are n risky assets whose returns are jointly normally distributed.

Consider the meanvariance analysis covered in this chapter where there are risky assets whose returns are jointly normally distributed. Assume that investors differ with regard to their concave utility functions and their initial wealths. Also assume that investors can lend at the riskfree rate, but investors are restricted from riskfree borrowing; that riskfree borrowing permitted.

Given this riskfree borrowing restriction, graphically show the efficient frontier for these investors expected portfolio returnstandard deviation space

Explain why only three portfolios are needed construct this efficient frontier, and locate these three portfolios your graph. that these portfolios may not unique.

least one these portfolios will sometimes need sold short generate the entire efficient frontier. Which portfolio the graph and what range the efficient frontier will sold short? Explain.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Private Capital Investing The Handbook Of Private Debt And Private Equity

Authors: Roberto Ippolito

1st Edition

1119526167, 978-1119526162