Answered step by step

Verified Expert Solution

Question

1 Approved Answer

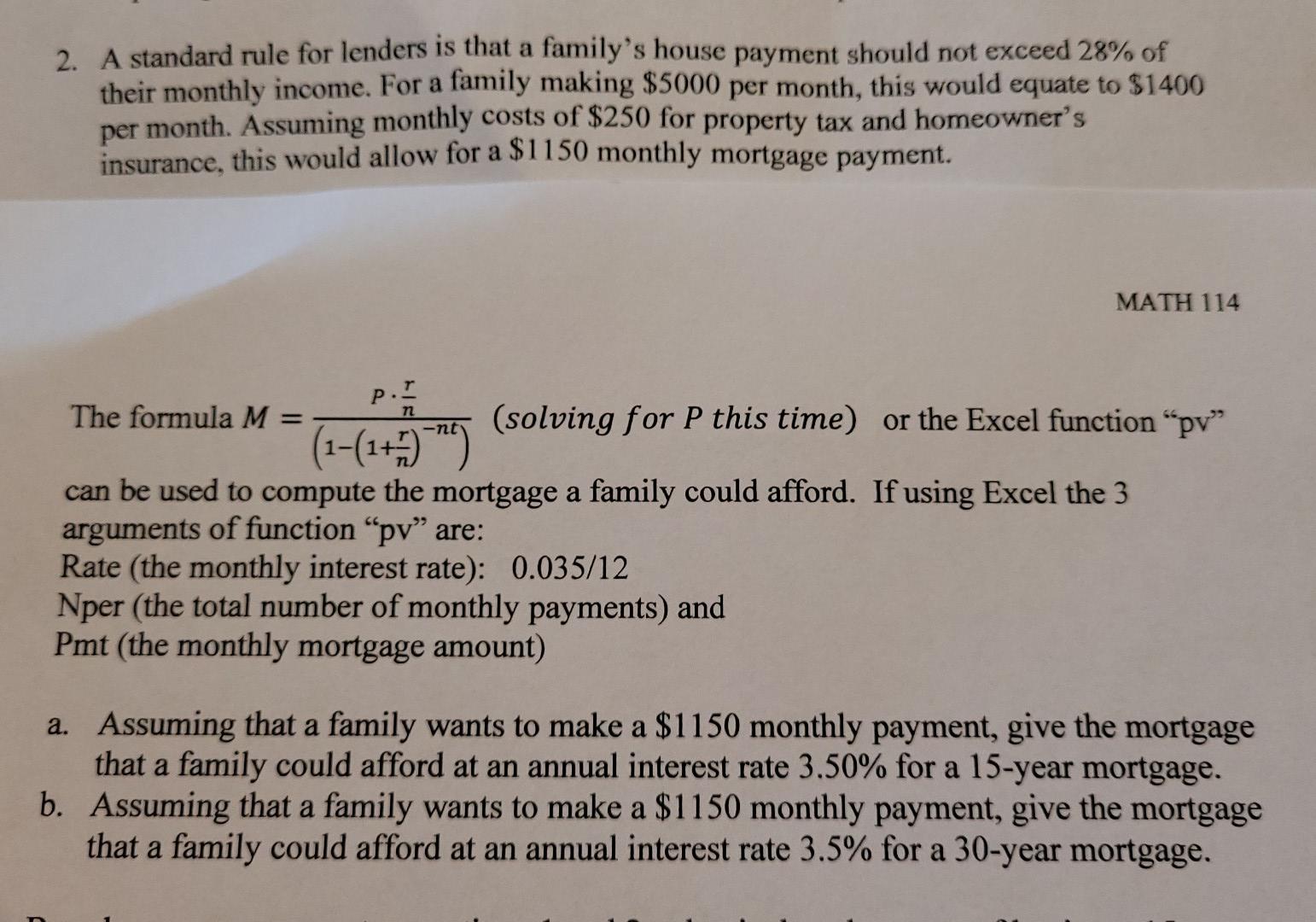

2. A standard rule for lenders is that a family's house payment should not exceed 28% of their monthly income. For a family making $5000

2. A standard rule for lenders is that a family's house payment should not exceed 28% of their monthly income. For a family making $5000 per month, this would equate to $1400 per month. Assuming monthly costs of $250 for property tax and homeowner's insurance, this would allow for a $1150 monthly mortgage payment. MATH 114 n -ni P. The formula M= (solving for P this time) or the Excel function "pv" (1-(1+77) can be used to compute the mortgage a family could afford. If using Excel the 3 arguments of function py" are: Rate (the monthly interest rate): 0.035/12 Nper (the total number of monthly payments) and Pmt (the monthly mortgage amount) a. Assuming that a family wants to make a $1150 monthly payment, give the mortgage that a family could afford at an annual interest rate 3.50% for a 15-year mortgage. b. Assuming that a family wants to make a $1150 monthly payment, give the mortgage that a family could afford at an annual interest rate 3.5% for a 30-year mortgage. a

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance A Contemporary Application of Theory to Policy

Authors: David N Hyman

11th edition

9781305474253, 1285173953, 1305474252, 978-1285173955