Answered step by step

Verified Expert Solution

Question

1 Approved Answer

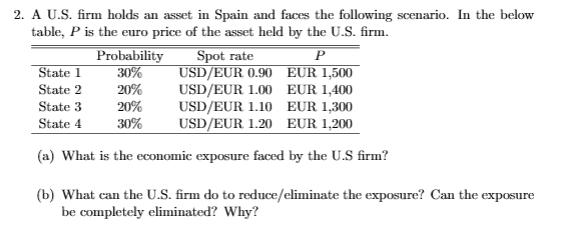

2. A U.S. firm holds an asset in Spain and faces the following scenario. In the below table, P is the euro price of

2. A U.S. firm holds an asset in Spain and faces the following scenario. In the below table, P is the euro price of the asset held by the U.S. firm. Spot rate P USD/EUR 0.90 EUR 1,500 Probability State 1 30% State 2 20% State 3 State 4 20% USD/EUR 1.00 EUR 1,400 USD/EUR 1.10 EUR 1,300 30% USD/EUR 1.20 EUR 1,200 (a) What is the economic exposure faced by the U.S firm? (b) What can the U.S. firm do to reduce/eliminate the exposure? Can the exposure be completely eliminated? Why?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Financial Management

Authors: Cheol S. Eun, Bruce G.Resnick

6th Edition

71316973, 978-0071316972, 78034655, 978-0078034657