Answered step by step

Verified Expert Solution

Question

1 Approved Answer

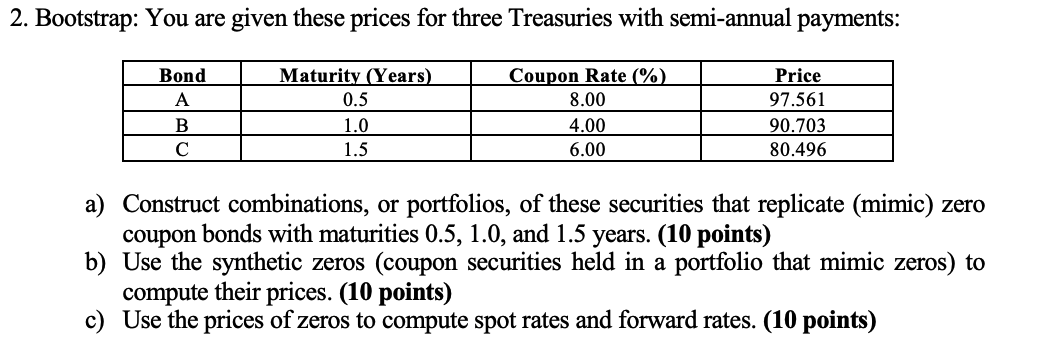

2. Bootstrap: You are given these prices for three Treasuries with semi-annual payments: Bond A B C Maturity (Years) 0.5 1.0 1.5 Coupon Rate

2. Bootstrap: You are given these prices for three Treasuries with semi-annual payments: Bond A B C Maturity (Years) 0.5 1.0 1.5 Coupon Rate (%) 8.00 4.00 6.00 Price 97.561 90.703 80.496 a) Construct combinations, or portfolios, of these securities that replicate (mimic) zero coupon bonds with maturities 0.5, 1.0, and 1.5 years. (10 points) b) Use the synthetic zeros (coupon securities held in a portfolio that mimic zeros) to compute their prices. (10 points) c) Use the prices of zeros to compute spot rates and forward rates. (10 points)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding financial statements

Authors: Lyn M. Fraser, Aileen Ormiston

9th Edition

136086241, 978-0136086246