Answered step by step

Verified Expert Solution

Question

1 Approved Answer

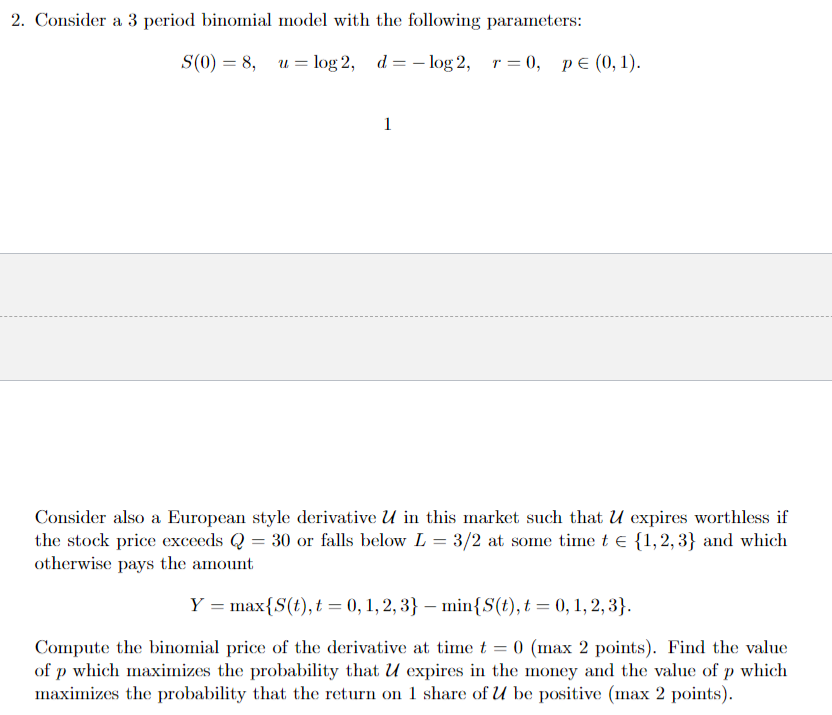

2. Consider a 3 period binomial model with the following parameters: S(0) = 8, u = log2, d= - log 2, r=0, PE (0,1). 1

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing Currency Options In Financial Institutions

Authors: Yat-Fai Lam, Kin-Keung Lai

1st Edition

1138778052, 978-1138778054