Answered step by step

Verified Expert Solution

Question

1 Approved Answer

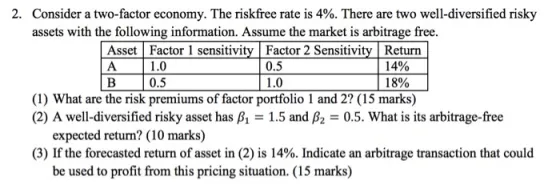

2. Consider a two-factor economy. The riskfree rate is 4%. There are two well-diversified risky assets with the following information. Assume the market is

2. Consider a two-factor economy. The riskfree rate is 4%. There are two well-diversified risky assets with the following information. Assume the market is arbitrage free. Asset Factor 1 sensitivity Factor 2 Sensitivity Return A 1.0 0.5 14% B 0.5 1.0 18% (1) What are the risk premiums of factor portfolio 1 and 2? (15 marks) (2) A well-diversified risky asset has 3 = 1.5 and = 0.5. What is its arbitrage-free expected return? (10 marks) (3) If the forecasted return of asset in (2) is 14%. Indicate an arbitrage transaction that could be used to profit from this pricing situation. (15 marks)

Step by Step Solution

★★★★★

3.32 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

a Let factor portfolio risk premums for factor 1 and 2vbe RP1 and RP2 respectively By using Mult...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Investments

Authors: Gordon J. Alexander, William F. Sharpe, Jeffery V. Bailey

3rd edition

132926172, 978-0132926171