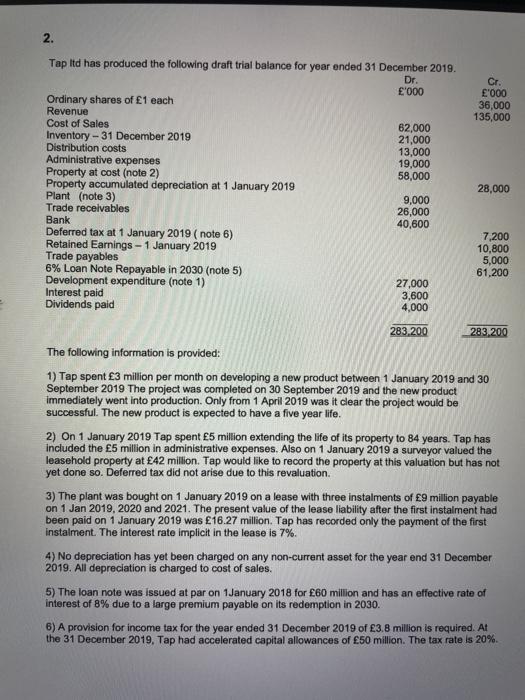

2. Cr. E'000 36,000 135,000 Tap Itd has produced the following draft trial balance for year ended 31 December 2019. Dr. '000 Ordinary shares of 1 each Revenue Cost of Sales 62,000 Inventory - 31 December 2019 21,000 Distribution costs 13,000 Administrative expenses 19,000 Property at cost (note 2) 58,000 Property accumulated depreciation at 1 January 2019 Plant (note 3) 9,000 Trade receivables 26,000 Bank 40,600 Deferred tax at 1 January 2019 (note 6) Retained Earnings - 1 January 2019 Trade payables 6% Loan Note Repayable in 2030 (note 5) Development expenditure (note 1) 27,000 Interest paid 3,600 Dividends paid 4,000 28,000 7,200 10.800 5,000 61,200 283 200 283 200 The following information is provided: 1) Tap spent 3 million per month on developing a new product between 1 January 2019 and 30 September 2019 The project was completed on 30 September 2019 and the new product immediately went into production. Only from 1 April 2019 was it clear the project would be successful. The new product is expected to have a five year life. 2) On 1 January 2019 Tap spent 5 million extending the life of its property to 84 years. Tap has included the 5 million in administrative expenses. Also on 1 January 2019 a surveyor valued the leasehold property at 42 million. Tap would like to record the property at this valuation but has not yet done so. Deferred tax did not arise due to this revaluation. 3) The plant was bought on 1 January 2019 on a lease with three instalments of 9 million payable on 1 Jan 2019, 2020 and 2021. The present value of the lease liability after the first instalment had been paid on 1 January 2019 was 16.27 million. Tap has recorded only the payment of the first instalment. The interest rate implicit in the lease is 7%. 4) No depreciation has yet been charged on any non-current asset for the year end 31 December 2019. All depreciation is charged to cost of sales. 5) The loan note was issued at par on January 2018 for 60 million and has an effective rate of interest of 8% due to a large premium payable on its redemption in 2030. 6) A provision for income tax for the year ended 31 December 2019 of 3.8 million is required. At the 31 December 2019. Tap had accelerated capital allowances of 50 million. The tax rate is 20% Required: In accordance with IAS 1 Presentation of Financial Statements: a) Prepare Tap's statement of profit or loss and other comprehensive income for the year ending 31 December 2019. (11 marks) b) Prepare Tap's statement of changes in equity for the year ending 31 December 2019. (3 marks) c) Prepare Tap's statement of financial position as at 31 December 2019. (11 marks) 2. Cr. E'000 36,000 135,000 Tap Itd has produced the following draft trial balance for year ended 31 December 2019. Dr. '000 Ordinary shares of 1 each Revenue Cost of Sales 62,000 Inventory - 31 December 2019 21,000 Distribution costs 13,000 Administrative expenses 19,000 Property at cost (note 2) 58,000 Property accumulated depreciation at 1 January 2019 Plant (note 3) 9,000 Trade receivables 26,000 Bank 40,600 Deferred tax at 1 January 2019 (note 6) Retained Earnings - 1 January 2019 Trade payables 6% Loan Note Repayable in 2030 (note 5) Development expenditure (note 1) 27,000 Interest paid 3,600 Dividends paid 4,000 28,000 7,200 10.800 5,000 61,200 283 200 283 200 The following information is provided: 1) Tap spent 3 million per month on developing a new product between 1 January 2019 and 30 September 2019 The project was completed on 30 September 2019 and the new product immediately went into production. Only from 1 April 2019 was it clear the project would be successful. The new product is expected to have a five year life. 2) On 1 January 2019 Tap spent 5 million extending the life of its property to 84 years. Tap has included the 5 million in administrative expenses. Also on 1 January 2019 a surveyor valued the leasehold property at 42 million. Tap would like to record the property at this valuation but has not yet done so. Deferred tax did not arise due to this revaluation. 3) The plant was bought on 1 January 2019 on a lease with three instalments of 9 million payable on 1 Jan 2019, 2020 and 2021. The present value of the lease liability after the first instalment had been paid on 1 January 2019 was 16.27 million. Tap has recorded only the payment of the first instalment. The interest rate implicit in the lease is 7%. 4) No depreciation has yet been charged on any non-current asset for the year end 31 December 2019. All depreciation is charged to cost of sales. 5) The loan note was issued at par on January 2018 for 60 million and has an effective rate of interest of 8% due to a large premium payable on its redemption in 2030. 6) A provision for income tax for the year ended 31 December 2019 of 3.8 million is required. At the 31 December 2019. Tap had accelerated capital allowances of 50 million. The tax rate is 20% Required: In accordance with IAS 1 Presentation of Financial Statements: a) Prepare Tap's statement of profit or loss and other comprehensive income for the year ending 31 December 2019. (11 marks) b) Prepare Tap's statement of changes in equity for the year ending 31 December 2019. (3 marks) c) Prepare Tap's statement of financial position as at 31 December 2019. (11 marks)