Answered step by step

Verified Expert Solution

Question

1 Approved Answer

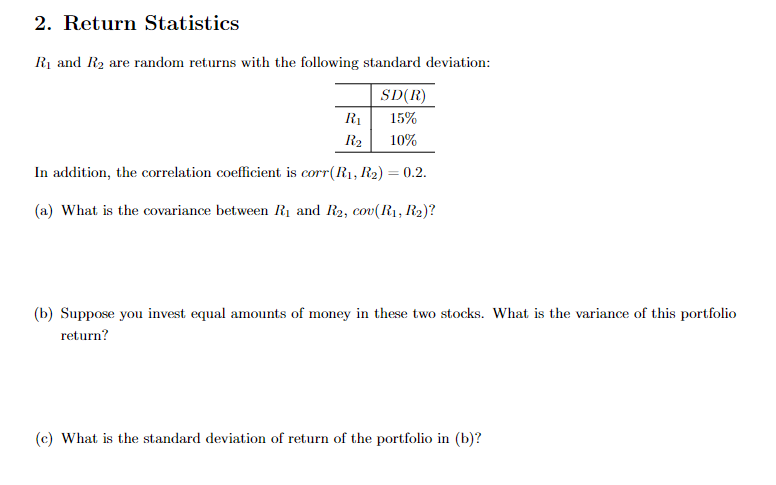

2. Keturn statistics R1 and R2 are random returns with the following standard deviation: In addition, the correlation coefficient is corr(R1,R2)=0.2. (a) What is the

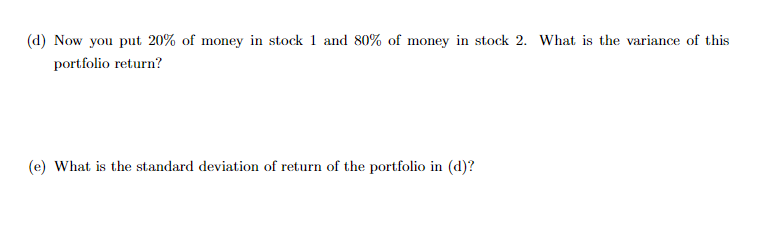

2. Keturn statistics R1 and R2 are random returns with the following standard deviation: In addition, the correlation coefficient is corr(R1,R2)=0.2. (a) What is the covariance between R1 and R2,cov(R1,R2) ? (b) Suppose you invest equal amounts of money in these two stocks. What is the variance of this portfolio return? (c) What is the standard deviation of return of the portfolio in (b)? (d) Now you put 20% of money in stock 1 and 80% of money in stock 2 . What is the variance of this portfolio return? (e) What is the standard deviation of return of the portfolio in (d)

2. Keturn statistics R1 and R2 are random returns with the following standard deviation: In addition, the correlation coefficient is corr(R1,R2)=0.2. (a) What is the covariance between R1 and R2,cov(R1,R2) ? (b) Suppose you invest equal amounts of money in these two stocks. What is the variance of this portfolio return? (c) What is the standard deviation of return of the portfolio in (b)? (d) Now you put 20% of money in stock 1 and 80% of money in stock 2 . What is the variance of this portfolio return? (e) What is the standard deviation of return of the portfolio in (d) Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Housing Finance

Authors: Peter King

2nd Edition

0415432952, 978-0415432955