Answered step by step

Verified Expert Solution

Question

1 Approved Answer

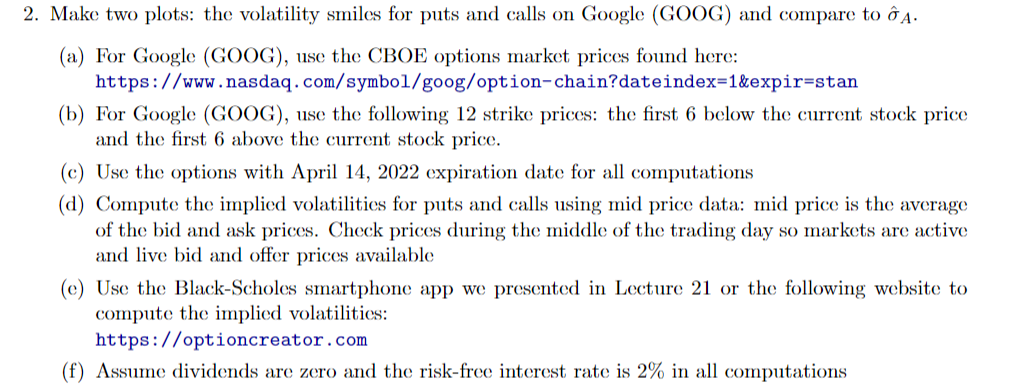

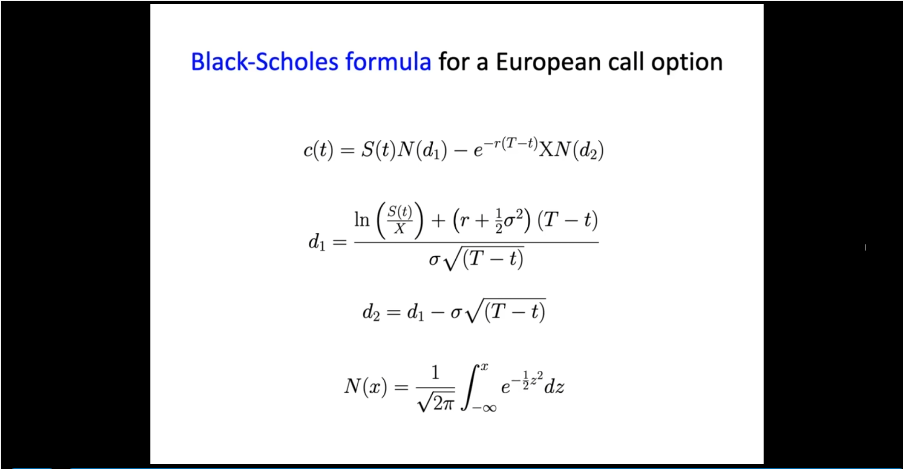

2. Make two plots: the volatility smiles for puts and calls on Google (GOOG) and compare to 64. (a) For Google (GOOG), use the CBOE

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Abstract Algebra A First Course

Authors: Dan Saracino

2nd Edition

1478618221, 9781478618225