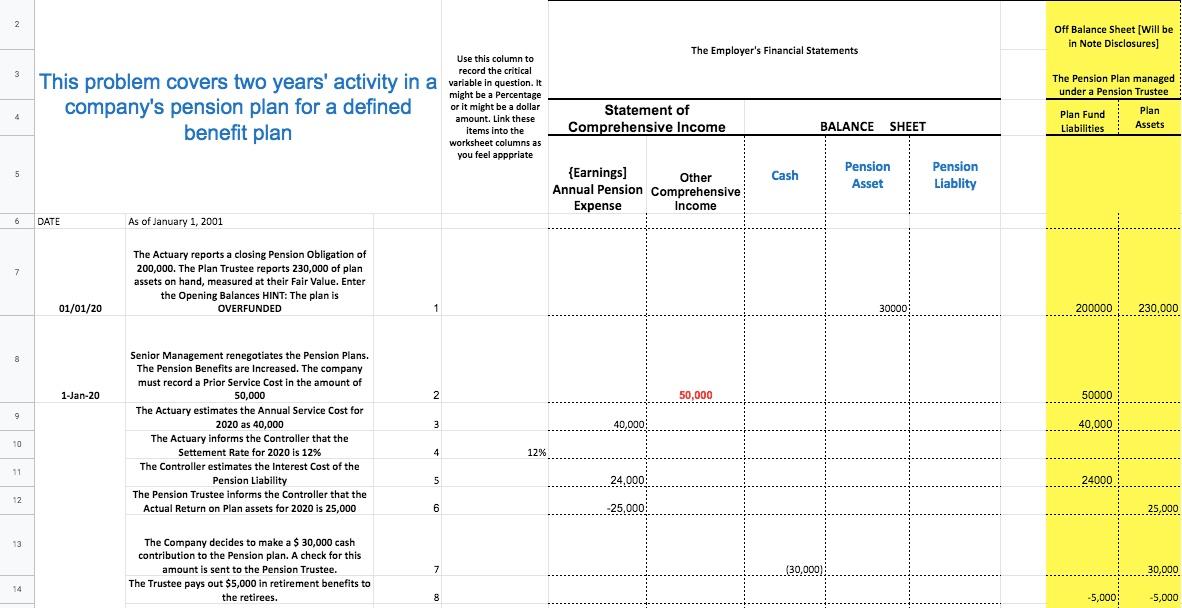

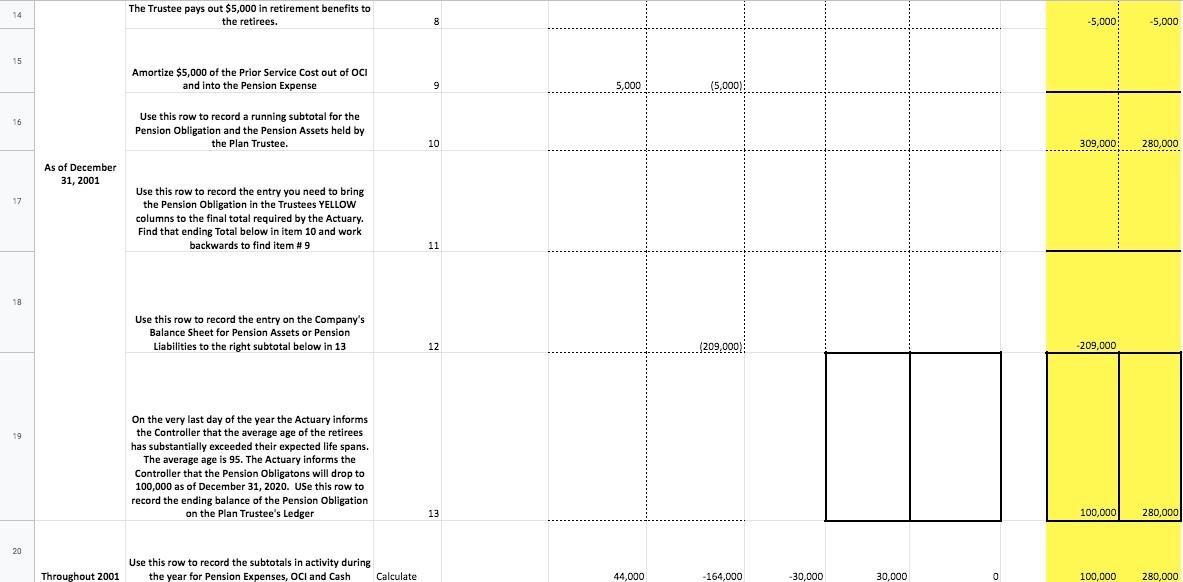

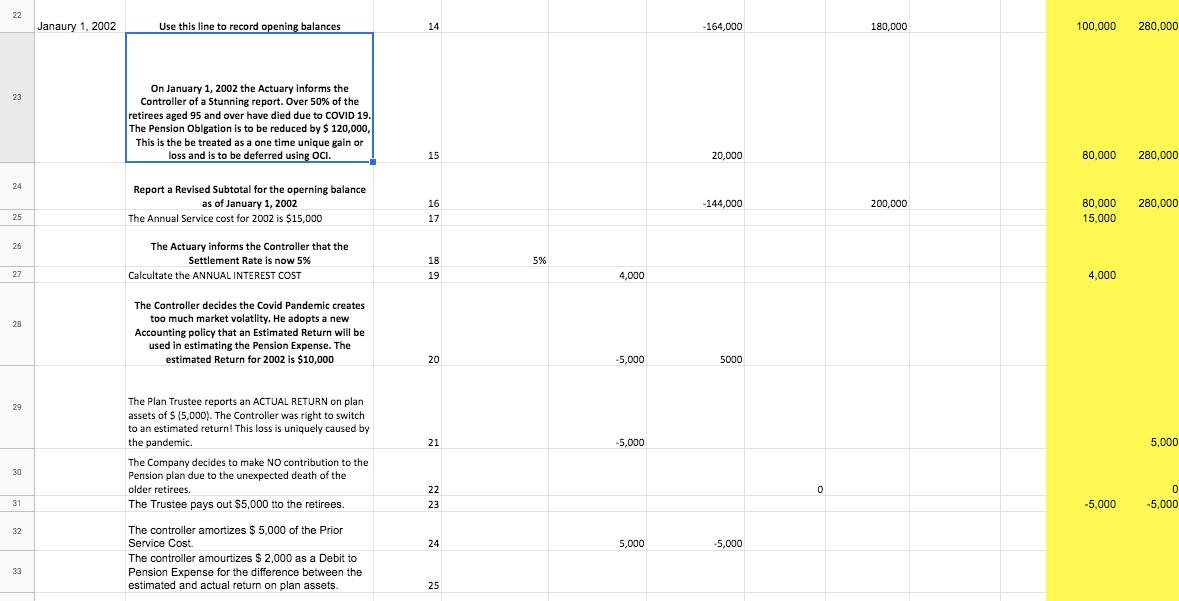

2 Off Balance Sheet (Will be [ in Note Disclosures] The Employer's Financial Statements Use this column to record the critical 3 The Pension Plan managed under a Pension Trustee This problem covers two years' activity in a variable in question. It company's pension plan for a defined benefit plan or it might be a dollar amount. Link these items into the worksheet columns as you feel apppriate Statement of Comprehensive Income BALANCE SHEET Plan Fund Liabilities Plan Assets Pension 5 Cash Pension Asset {Earnings] Other Annual Pension Comprehensive Expense Income Liablity 6 DATE As of January 1, 2001 7 7. The Actuary reports a closing Pension Obligation of a 200,000. The Plan Trustee reports 230,000 of plan assets on hand, measured at their Fair Value. Enter the Opening Balances HINT: The plan is OVERFUNDED 01/01/20 1 30000 200000 230,000 -... & 1-Jan-20 2 50,000 50000 9 3 40,000: Senior Management renegotiates the Pension Plans. The Pension Benefits are increased. The company must record a Prior Service Cost in the amount of 50,000 The Actuary estimates the Annual Service Cost for 2020 as 40,000 The Actuary informs the Controller that the Settement Rate for 2020 is 12% The Controller estimates the Interest Cost of the Pension Liability The Pension Trustee informs the Controller that the Actual Return on Plan assets for 2020 is 25,000 40,000 10 4 12% 11 5 24,000 24000 12 6 25,000 25,000 13 The Company decides to make a $ 30,000 cash contribution to the Pension plan. A check for this amount is sent to the Pension Trustee. The Trustee pays out $5,000 in retirement benefits to the retirees. 7 (30,000) 30,000 14 8 -5,000 -5,000 14 The Trustee pays out $5,000 in retirement benefits to the retirees. 8 -5,000 -5,000 15 Amortize $5,000 of the Prior Service Cost out of OCI and into the Pension Expense 9 5,000 (5,000) 16 Use this row to record a running subtotal for the Pension Obligation and the Pension Assets held by the Plan Trustee. 10 309,000 280.000 As of December 31, 2001 17 Use this row to record the entry you need to bring the Pension Obligation in the Trustees YELLOW columns to the final total required by the Actuary. Find that ending Total below in item 10 and work backwards to find item #9 # 11 18 Use this row to record the entry on the Company's Balance Sheet for Pension Assets or Pension Liabilities to the right subtotal below in 13 12 (209,000): -209,000 19 On the very last day of the year the Actuary informs the Controller that the average age of the retirees has substantially exceeded their expected life spans. The average age is 95. The Actuary informs the Controller that the Pension Obligatons will drop to 100,000 as of December 31, 2020. Use this row to record the ending balance of the Pension Obligation on the Plan Trustee's Ledger 13 100,000 280,000 20 Use this row to record the subtotals in activity during the year for Pension Expenses, OCl and Cash Throughout 2001 Calculate 44,000 -164,000 30,000 30,000 0 0 100,000 280.000 22 Janaury 1, 2002 Use this line to record opening balances 14 -164,000 180,000 100.000 280,000 23 On January 1, 2002 the Actuary informs the Controller of a Stunning report. Over 50% of the retirees aged 95 and over have died due to COVID 19. The Pension Oblgation is to be reduced by $ 120,000, This is the be treated as a one time unique gain or loss and is to be deferred using OCI. 15 20,000 80,000 280,000 24 Report a Revised Subtotal for the operning balance as of January 1, 2002 The Annual Service cost for 2002 is $15,000 -144,000 200.000 280,000 16 17 80,000 15,000 25 26 The Actuary informs the Controller that the Settlement Rate is now 5% Calcultate the ANNUAL INTEREST COST 5% 18 19 27 4,000 4.000 28 The Controller decides the Covid Pandemic creates too much market volatlity. He adopts a new Accounting policy that an Estimated Return will be used in estimating the Pension Expense. The estimated Return for 2002 is $10,000 20 -5,000 5000 29 21 -5,000 5,000 30 The Plan Trustee reports an ACTUAL RETURN on plan assets of S (5,000). The Controller was right to switch to an estimated return! This loss is uniquely caused by the pandemic. The Company decides to make NO contribution to the Pension plan due to the unexpected death of the older retirees. . The Trustee pays out $5,000 tto the retirees. The controller amortizes $5,000 of the Prior Service Cost The controller amourtizes $ 2,000 as a Debit to Pension Expense for the difference between the estimated and actual return on plan assets. 0 22 23 0 -5,000 31 -5,000 32 24 5,000 -5,000 33 25 30 0 0 22 23 31 -5,000 0 -5,000 The Company decides to make NO contribution to the Pension plan due to the unexpected death of the older retirees. The Trustee pays out $5,000 tto the retirees. The controller amortizes $5,000 of the Prior Service Cost The controller amourtizes $ 2,000 as a Debit to Pension Expense for the difference between the estimated and actual return on plan assets. 32 24 5,000 -5,000 33 25 34 The controller amortizes $3,000 into the Pension Expense related to the unexpected GAIN from the death of the retirees due to the Pandemic. 26 35 27 Use this row to prepare the entries to Pension Assets and Pension Liabilities on the Company's Balance Sheet Use this row to find a running subtotal for the Pension Obligation and the Pension Assets. In 2002 unlike 2001 these are the ending balances for these two items. The actuarv is makina no 36 28 37 Use this line to record the net Pension Expense, the OCI changes and the net entry to CASH 29 30 39 40 41 2 Off Balance Sheet (Will be [ in Note Disclosures] The Employer's Financial Statements Use this column to record the critical 3 The Pension Plan managed under a Pension Trustee This problem covers two years' activity in a variable in question. It company's pension plan for a defined benefit plan or it might be a dollar amount. Link these items into the worksheet columns as you feel apppriate Statement of Comprehensive Income BALANCE SHEET Plan Fund Liabilities Plan Assets Pension 5 Cash Pension Asset {Earnings] Other Annual Pension Comprehensive Expense Income Liablity 6 DATE As of January 1, 2001 7 7. The Actuary reports a closing Pension Obligation of a 200,000. The Plan Trustee reports 230,000 of plan assets on hand, measured at their Fair Value. Enter the Opening Balances HINT: The plan is OVERFUNDED 01/01/20 1 30000 200000 230,000 -... & 1-Jan-20 2 50,000 50000 9 3 40,000: Senior Management renegotiates the Pension Plans. The Pension Benefits are increased. The company must record a Prior Service Cost in the amount of 50,000 The Actuary estimates the Annual Service Cost for 2020 as 40,000 The Actuary informs the Controller that the Settement Rate for 2020 is 12% The Controller estimates the Interest Cost of the Pension Liability The Pension Trustee informs the Controller that the Actual Return on Plan assets for 2020 is 25,000 40,000 10 4 12% 11 5 24,000 24000 12 6 25,000 25,000 13 The Company decides to make a $ 30,000 cash contribution to the Pension plan. A check for this amount is sent to the Pension Trustee. The Trustee pays out $5,000 in retirement benefits to the retirees. 7 (30,000) 30,000 14 8 -5,000 -5,000 14 The Trustee pays out $5,000 in retirement benefits to the retirees. 8 -5,000 -5,000 15 Amortize $5,000 of the Prior Service Cost out of OCI and into the Pension Expense 9 5,000 (5,000) 16 Use this row to record a running subtotal for the Pension Obligation and the Pension Assets held by the Plan Trustee. 10 309,000 280.000 As of December 31, 2001 17 Use this row to record the entry you need to bring the Pension Obligation in the Trustees YELLOW columns to the final total required by the Actuary. Find that ending Total below in item 10 and work backwards to find item #9 # 11 18 Use this row to record the entry on the Company's Balance Sheet for Pension Assets or Pension Liabilities to the right subtotal below in 13 12 (209,000): -209,000 19 On the very last day of the year the Actuary informs the Controller that the average age of the retirees has substantially exceeded their expected life spans. The average age is 95. The Actuary informs the Controller that the Pension Obligatons will drop to 100,000 as of December 31, 2020. Use this row to record the ending balance of the Pension Obligation on the Plan Trustee's Ledger 13 100,000 280,000 20 Use this row to record the subtotals in activity during the year for Pension Expenses, OCl and Cash Throughout 2001 Calculate 44,000 -164,000 30,000 30,000 0 0 100,000 280.000 22 Janaury 1, 2002 Use this line to record opening balances 14 -164,000 180,000 100.000 280,000 23 On January 1, 2002 the Actuary informs the Controller of a Stunning report. Over 50% of the retirees aged 95 and over have died due to COVID 19. The Pension Oblgation is to be reduced by $ 120,000, This is the be treated as a one time unique gain or loss and is to be deferred using OCI. 15 20,000 80,000 280,000 24 Report a Revised Subtotal for the operning balance as of January 1, 2002 The Annual Service cost for 2002 is $15,000 -144,000 200.000 280,000 16 17 80,000 15,000 25 26 The Actuary informs the Controller that the Settlement Rate is now 5% Calcultate the ANNUAL INTEREST COST 5% 18 19 27 4,000 4.000 28 The Controller decides the Covid Pandemic creates too much market volatlity. He adopts a new Accounting policy that an Estimated Return will be used in estimating the Pension Expense. The estimated Return for 2002 is $10,000 20 -5,000 5000 29 21 -5,000 5,000 30 The Plan Trustee reports an ACTUAL RETURN on plan assets of S (5,000). The Controller was right to switch to an estimated return! This loss is uniquely caused by the pandemic. The Company decides to make NO contribution to the Pension plan due to the unexpected death of the older retirees. . The Trustee pays out $5,000 tto the retirees. The controller amortizes $5,000 of the Prior Service Cost The controller amourtizes $ 2,000 as a Debit to Pension Expense for the difference between the estimated and actual return on plan assets. 0 22 23 0 -5,000 31 -5,000 32 24 5,000 -5,000 33 25 30 0 0 22 23 31 -5,000 0 -5,000 The Company decides to make NO contribution to the Pension plan due to the unexpected death of the older retirees. The Trustee pays out $5,000 tto the retirees. The controller amortizes $5,000 of the Prior Service Cost The controller amourtizes $ 2,000 as a Debit to Pension Expense for the difference between the estimated and actual return on plan assets. 32 24 5,000 -5,000 33 25 34 The controller amortizes $3,000 into the Pension Expense related to the unexpected GAIN from the death of the retirees due to the Pandemic. 26 35 27 Use this row to prepare the entries to Pension Assets and Pension Liabilities on the Company's Balance Sheet Use this row to find a running subtotal for the Pension Obligation and the Pension Assets. In 2002 unlike 2001 these are the ending balances for these two items. The actuarv is makina no 36 28 37 Use this line to record the net Pension Expense, the OCI changes and the net entry to CASH 29 30 39 40 41