Answered step by step

Verified Expert Solution

Question

1 Approved Answer

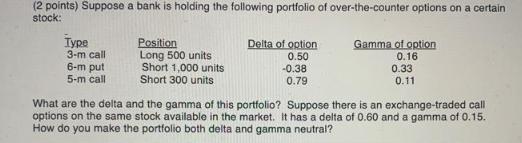

(2 points) Suppose a bank is holding the following portfolio of over-the-counter options on a certain stock: Type 3-m call Position Long 500 units

(2 points) Suppose a bank is holding the following portfolio of over-the-counter options on a certain stock: Type 3-m call Position Long 500 units Delta of option Gamma of option 0.50 0.16 6-m put Short 1,000 units -0.38 0.33 5-m call Short 300 units 0.79 0.11 What are the delta and the gamma of this portfolio? Suppose there is an exchange-traded call options on the same stock available in the market. It has a delta of 0.60 and a gamma of 0.15. How do you make the portfolio both delta and gamma neutral?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To find the delta and gamma of the portfolio you sum up the deltas and gammas of each individual opt...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

663dda2b1254f_961625.pdf

180 KBs PDF File

663dda2b1254f_961625.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Futures and Options Markets

Authors: John C. Hull

8th edition

978-1292155036, 1292155035, 132993341, 978-0132993340