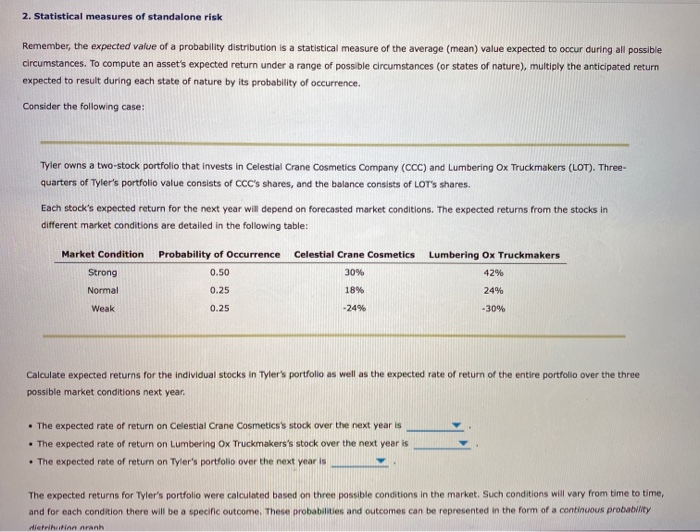

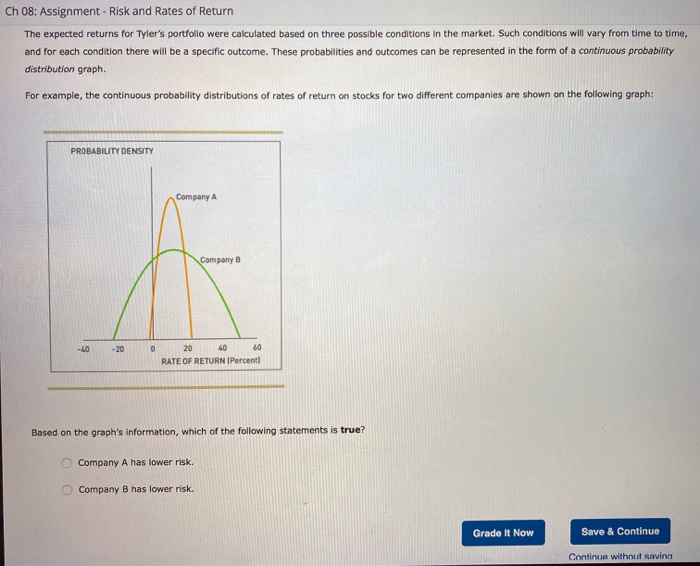

2. Statistical measures of standalone risk Remember, the expected value of a probability distribution is a statistical measure of the average (mean) value expected to occur during all possible circumstances. To compute an asset's expected return under a range of possible circumstances (or states of nature), multiply the anticipated return expected to result during each state of nature by its probability of occurrence. Consider the following case: Tyler owns a two-stock portfolio that invests in Celestial Crane Cosmetics Company (CCC) and Lumbering Ox Truckmakers (LOT). Three- quarters of Tyler's portfolio value consists of CCC's shares, and the balance consists of LOT's shares Each stock's expected return for the next year will depend on forecasted market conditions. The expected returns from the stocks in different market conditions are detailed in the following table: Market Condition Strong Normal Probability of Occurrence 0.50 Celestial Crane Cosmetics 30% Lumbering Ox Truckmakers 42% 0.25 18% 24% Weak 0.25 -24% -30% Calculate expected returns for the individual stocks in Tyler's portfolio as well as the expected rate of return of the entire portfolio over the three possible market conditions next year. The expected rate of return on Celestial Crane Cosmetics's stock over the next year is The expected rate of return on Lumbering Ox Truckmakers's stock over the next year is . The expected rate of return on Tyler's portfolio over the next year is . The expected returns for Tyler's portfolio were calculated based on three possible conditions in the market. Such conditions will vary from time to time, and for each condition there will be a specific outcome. These probabilities and outcomes can be represented in the form of a continuous probability distribution aranh Ch 08: Assignment - Risk and Rates of Return The expected returns for Tyler's portfolio were calculated based on three possible conditions in the market. Such conditions will vary from time to time, and for each condition there will be a specific outcome. These probabilities and outcomes can be represented in the form of a continuous probability distribution graph For example, the continuous probability distributions of rates of return on stocks for two different companies are shown on the following graph: PROBABILITY DENSITY Company A Company B -20 20 40 60 RATE OF RETURN (Percent) Based on the graph's information, which of the following statements is true? Company A has lower risk. Company B has lower risk. Grade It Now Save & Continue Continue without savinn