Answered step by step

Verified Expert Solution

Question

1 Approved Answer

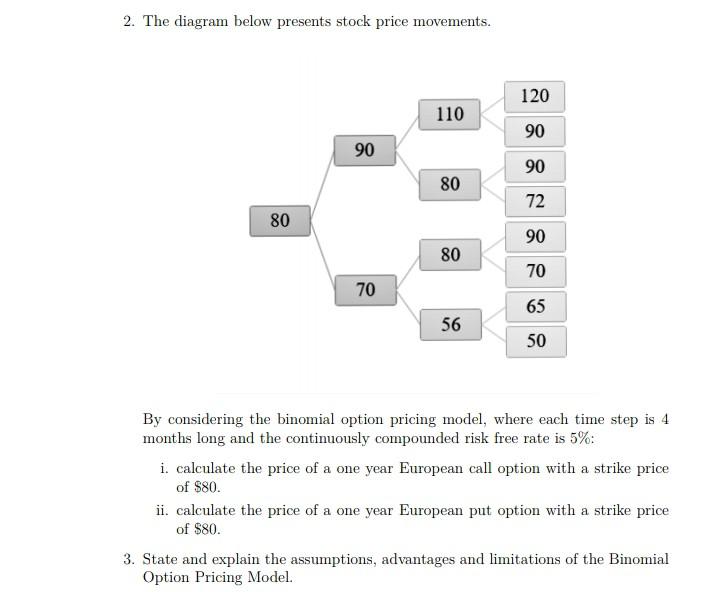

2. The diagram below presents stock price movements. By considering the binomial option pricing model, where each time step is 4 months long and the

2. The diagram below presents stock price movements. By considering the binomial option pricing model, where each time step is 4 months long and the continuously compounded risk free rate is 5% : i. calculate the price of a one year European call option with a strike price of $80. ii. calculate the price of a one year European put option with a strike price of $80. 3. State and explain the assumptions, advantages and limitations of the Binomial Option Pricing Model. 2. The diagram below presents stock price movements. By considering the binomial option pricing model, where each time step is 4 months long and the continuously compounded risk free rate is 5% : i. calculate the price of a one year European call option with a strike price of $80. ii. calculate the price of a one year European put option with a strike price of $80. 3. State and explain the assumptions, advantages and limitations of the Binomial Option Pricing Model

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

American Public School Finance

Authors: William A. Owings, Leslie S. Kaplan

1st Edition

0495807834, 9780495807834